PW Consulting Predicts InGaAs Photodiodes & Arrays Market to Reach USD 351.2 Million by 2032

PW Consulting Strategic Preview: InGaAs Photodiodes and Arrays Market — 2026 Outlook

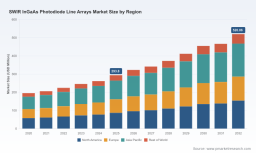

In 2026 the InGaAs photodiodes and arrays sector occupies a strategic crossroads for optics, defense, and industrial sensing investments. Our latest market model uses 2025 as the base year and shows the market expanding from USD 219.0 Million in 2025 to a materially larger footprint by 2032, at a compound annual growth rate (CAGR) of 6.98%. This briefing highlights the decision-useful takeaways senior leaders need today — without disclosing the granular segment tables that we reserve for subscribers.

InGaAs Photodiodes and Arrays Market

Why 2026 Is a Pivotal Year for Capital Allocation

Three structural shifts compress decision timelines for investors, OEMs, and systems integrators in 2026:

- Supply-chain tightness: Strategic raw materials and substrate availability are creating single-point risks that elevate lead-times and input cost volatility.

- Regulatory complexity: The combination of export licensing for SWIR-capable systems and jurisdictional dual-use rules increases transaction friction and compliance expense for cross-border programs.

- Technology-defining design wins: Customers are shifting procurement toward suppliers who can deliver both device performance (uniformity, operability, pixel architecture) and downstream integration (hybridized ROICs, packaging, life-cycle qualification).

Market Trajectory — Macro View

Our market construct shows steady growth driven by a portfolio of application pull and manufacturing maturation. The sector’s baseline in 2025 is USD 219.0 Million, and the forecast path through 2032 reflects a 6.98% CAGR. Growth is being underwritten by expanding adoption in spectroscopy, machine-vision line-scan inspection, and security/hyperspectral systems, while new product introductions are extending measurable performance into adjacent use cases.

Importantly, the headline figures mask heterogeneity across regions and end markets. Rather than reproducing those distributions here, we emphasize the directional dynamics that matter for 2026 capital allocation: rising demand for longer-wavelength SWIR capability, concentration of high-value design activity among specialized suppliers, and a gradual shift of manufacturing emphasis toward integration of epitaxial growth with advanced ROIC hybridization. For a complete breakdown of geographic and application distributions and interactive charts, see the full report.

Operational Playbook Contained in the Report

Buyers and operators repeatedly tell us they need executable assets, not only market sizing. The report therefore includes a suite of tools that translate insight into operational levers for 2026:

- Supply-chain mapping and supplier tiers — visibility into substrate sources, back-end hybridization partners, and logistics chokepoints.

- BOM decomposition logic — a reproducible framework to disaggregate finished-device costs into material, process, test, and overhead buckets.

- Yield-adjustment models — parametric models that quantify how incremental improvements in epitaxial quality, hybridization yield, and pixel operability map to margin expansion.

- Technology roadmap and capability matrix — comparative assessment of pixel pitch, spectral cutoff, and packaging strategies linked to system-level KPIs.

- Compliance and export-readiness checklist — practical matrices that highlight licensing triggers, documentation requirements, and approval timelines in critical jurisdictions.

Each tool is modular and designed to be applied in boardroom scenarios: M&A due diligence, capex prioritization, supplier selection, and price negotiation. The deliverables are intentionally prescriptive about where to act (for example, which supply nodes to de-risk) but do not publish the confidential parametric inputs that underpin those recommendations — readers are directed to the full report for the detailed worksheets.

Competitive Landscape — Dimensions that Decide Design Wins

Market leadership in InGaAs photodiodes and arrays is built across several, often overlapping, competitive dimensions. Our competitive analysis focuses on the strategic levers that determine sustainable advantage rather than speculative annual playbooks.

- Technology moat: Suppliers with vertically integrated epitaxial capabilities and deep hybridization experience create performance differentiation via higher operability and lower pixel defects. This technical configuration shortens qualification cycles for large OEMs.

- Manufacturing scale and yield expertise: High-volume producers that have invested in process control and test automation reduce the unit cost of pixels and increase effective throughput — a decisive factor when customers evaluate total cost of ownership.

- Systems-level integration: Vendors who couple sensors with proven mechanical, thermal, and ROIC subsystems win larger bill-of-materials and gain stickiness through embedded design wins.

- Regulatory and export credentialing: Suppliers with established export licensing workflows and controlled-goods compliance are preferred for multinational programs — a rapidly emergent procurement criterion in 2026.

Selected incumbents illustrate these dimensions: some firms excel in high-uniformity line arrays and long-wavelength coverage; others compete on pixel-density and hybrid ROIC partnerships. Recent public milestones — such as a February 2026 commercial launch of a rectangular-pixel line-scan camera for spectroscopy and OCT, and a 2025 product-line confirmation for 1.7um-optimized arrays — validate supplier efforts to extend product portfolios into higher-value niches. We analyze each major supplier across the above dimensions in the full report and map where their competitive posture is likely to influence your sourcing decisions. Access the full vendor maps and comparative matrices here: Full report and vendor maps .

Supply-side Constraints and Regulatory Headwinds

Two “noise” vectors merit particular attention in 2026 planning:

- Raw-material availability: Tighter export controls and limited suppliers of indium and InP substrates are increasing pressure on upstream costs and constraining capacity expansion timelines.

- Dual-use regulation: SWIR-capable imaging systems attract export control scrutiny in multiple jurisdictions, elevating operating costs for international sales and increasing time-to-revenue for multi-country programs.

For companies investing in new capacity or cross-border programs, hedging strategies are no longer optional. Practical options include forward raw-material agreements, qualification of parallel substrate routes, and embedding export-compliance checks into procurement and R&D gating processes. The report contains scenario workbooks that map the range of outcomes for supply disruption and regulatory delay — designed for board-level stress testing.

Practical Strategic Recommendations for 2026

Our synthesis points to a limited set of high-leverage actions for management teams considering capital deployment in 2026:

- Secure upstream exposure: prioritize contracts or minority partnerships with substrate and indium suppliers to reduce input-price volatility and ensure production continuity.

- Invest in hybridization capability: bring ROIC integration and packaging know-how closer to the sensor stack to accelerate time-to-market for higher-value line-scan and spectroscopy products.

- Target design-win pipelines: align product development with system integrator requirements early (testability, calibration flows, and lifecycle documentation) to shorten procurement cycles.

- Build compliance into product design: incorporate export control and documentation requirements into product release processes to avoid costly program delays.

- Allocate R&D to yield-bottlenecks: prioritize projects that improve epitaxial uniformity and pixel operability, because incremental gains here disproportionately improve margins.

Each recommendation is supported by quantitative trade-off models in the main report; executives can use those models to compare investment scenarios under multiple market and regulatory conditions.

Methodology — Why Our Findings Are Actionable

PW Consulting applies a layered-triangulation methodology to produce both accurate sizing and decision-ready operational tools. Our approach combines:

- Patent-anchored technical mapping to surface R&D trajectories and proprietary process innovations.

- Supplier and integrator interviews, including anonymized program-level disclosures from Tier-1 customers and contract manufacturers.

- Reverse-engineered BOMs and lab-based verification of device-level performance using partner test facilities.

- Custom customs-flow and trade-data analysis to detect upstream movements and hidden supply relationships.

We reconcile these inputs using multi-stage calibration: first, high-confidence datapoints (public disclosures, patents, and audited supplier data) are used to build base parameters; second, anonymous interviews and customs-derived signals are layered in to adjust for non-public production realities; third, scenario simulations stress-tested against macro assumptions produce the final forecast envelope. This process explains how we access and validate information that is not available in public filings, without relying on single-source anecdotes.

Next Steps — Access the Full Intelligence

This preview is intentionally selective to preserve the value of our integrated deliverables. The full report contains detailed segment distributions, regional and application maps, concentration metrics, downloadable models, and supplier scorecards that operational teams can apply immediately. To obtain the complete dataset, interactive models, and supplier benchmarking tools, access the report here: https://pmarketresearch.com/it/swir-ingaas-photodiode-line-arrays-market .

For clients requiring bespoke briefings, scenario workshops, or supplier diligence sprints in 2026, PW Consulting provides tailored engagement tracks that convert this market intelligence into executable procurement and R&D plans. Contact our advisor team to schedule a workshop based on your program priorities.

For detailed analysis of this topic, please visit the official page: InGaAs Photodiodes and Arrays Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.