PW Consulting Predicts Robust 5.9% CAGR for the Marine Composites Market

Marine Composites Market — Strategic Outlook for 2026

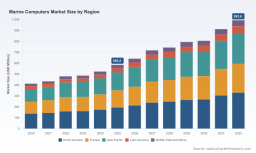

The global marine composites market is at an inflection point in 2026. After a period of steady recovery and capacity realignment from 2020–2025, the market reached approximately USD 5.6 Billion in 2025 and is on a projected growth path to roughly USD 8.3 Billion by 2032, reflecting a compound annual growth rate (CAGR) of 5.9% across the 2026–2032 forecast window. For boards, procurement committees, and corporate strategy teams allocating capital in 2026, these macro dynamics create both near-term execution challenges and multi-year opportunities—especially for firms that can translate technical capability into certified, producible designs and resilient supply chains.

Marine Composites Market

Why 2026 Is a Strategic Decision Year

Several contemporaneous factors converge in 2026 to compress the window for decisive action:

Marine Composites Market

- Regulatory tightening: international and flag-state standards—such as IEC 60945 and updated classification requirements from DNV—are raising the bar on environmental and EMC performance for marine systems. In addition, recent advisory updates (including NVIC-style guidance) are increasing scrutiny on qualified electronic charting and integrated bridge systems.

- Cost-to-compliance pressure: manufacturers face rising scrutiny on lifecycle emissions and traceability as ESG reporting begins to affect tender outcomes for commercial and passenger vessels.

- Technology modularization: demand for lower-weight, higher-performance composite laminates is intersecting with the need to integrate certified electronics and sensor suites into hull structures without sacrificing manufacturability or serviceability.

Consequently, 2026 is a year when capital allocation decisions—whether for plant upgrades, material qualification programs, or strategic supplier partnerships—will materially affect competitive positioning through the remainder of the decade.

Marine Composites Market

Market Structure and Competitive Concentration

The marine composites market exhibits a moderate concentration profile: the top three suppliers account for approximately 32.4% of the market, while the top five capture about 44.8%. This structure creates a dual strategic landscape. On one hand, buyers retain meaningful leverage with a diverse supplier base; on the other, leading vendors can exercise scale economies on prepreg and resin development, certifications, and capital-intensive automated layup cells.

Actionable Frameworks in the Report

PW Consulting’s latest study is explicitly designed to convert macro trends into executable actions for 2026. The report delivers a suite of practical diagnostic and planning tools that are immediately usable by procurement, engineering, and corporate development teams:

- Supply-chain topology maps that identify critical single points of failure across resin, fiber, and specialty additive flows, and that flag regulatory choke points for export control and classification compliance.

- Bill-of-Materials (BOM) decomposition logic that separates cost drivers into raw-material, processing, and certification buckets—enabling scenario-based cost modeling under alternative sourcing strategies.

- Yield-adjustment and throughput models tailored for common layup and infusion processes, allowing teams to quantify the trade-offs between cycle-time reductions and marginal scrap rates without divulging proprietary factory parameters.

- Technology roadmaps that trace material evolution (from glass-dominant systems toward increased carbon and hybrid constructs) and outline the certification milestones firms must achieve to support a tiered product rollout in regulated markets.

Each tool is accompanied by playbooks that focus on 2026 pain points—cost control under volatile resin pricing, certification sequencing under compressed product timelines, and compliance-driven traceability. The outputs are deliberately operational: procurement can run supplier stress tests; engineering can size qualification test matrices; and finance can model staged CAPEX tied to roll-out milestones.

Competitive Dynamics and Ecosystem Players

Understanding competitive dynamics requires evaluating not only composite material specialists but also adjacent ecosystem players whose certified subsystems affect boat integrators’ design choices. Our ecosystem mapping incorporates leading marine electronics vendors whose certification and form-factor trends materially influence composite hull design and systems integration.

Competitor Dimensions — What Really Matters

Across the supplier set we track, competitive advantage is built on a few repeatable dimensions rather than one-size-fits-all metrics. PW Consulting’s analysis highlights these vectors as decisive in 2026:

- Regulatory moat: firms that maintain active DNV/IEC/NMEA certifications reduce integration risk for shipyards and yacht OEMs—this reduces time-to-market for new composite designs and increases likelihood of design wins.

- Integration depth: companies that offer systems (panel PCs, displays, embedded controllers) with documented environmental hardening and cable-routing interfaces simplify the OEM’s packaging problem inside composite structures.

- Service and field-proven reliability: for passenger and commercial applications, demonstrated mean-time-between-failure and rapid field-repair workflows are as persuasive in procurement boards as headline performance specs.

- Supply resilience: suppliers with multi-region manufacturing footprints and tested alternate sourcing for long-lead components provide a tangible mitigation against geopolitical and logistics shocks.

Examples of ecosystem players we track include vendors that specialize in marine-certified electronics (from ruggedized panel PCs to sunlight-readable displays). Their recent product upgrades and industry recognitions reflect the broader trend: tight coupling of component certification and hull-level acceptance criteria. These dynamics create windows of opportunity for composites firms that can co-develop validated integration architectures with certified subsystem vendors.

Technology and Certification Pathways

In practice, the fastest route to procurement success in 2026 is a mapped pathway that aligns compound material selection with certification milestones and supplier readiness. Key elements include:

- Early-stage co-validation protocols with certified subsystem vendors to de-risk penetrating installations and to streamline type-approval timelines.

- Controlled material substitution strategies that maintain homologation status while reducing mass or cost.

- Traceable supply-chain provenance for resins and fibers to satisfy both classification societies and corporate ESG requirements.

These are not theoretical prescriptions. PW Consulting’s deliverables include templates and checklists that enable engineering teams to convert pathway elements into test plans and procurement contracts—helping decision-makers avoid costly rework and certification delays in 2026.

Methodology: How PW Consulting Captures Hard-to-Access Signals

Our methodology is designed to produce predictive, verifiable, and action-ready insights for corporate decision-makers. The study uses Layered Triangulation: we reconcile patent analytics, production-plant audits, and buyer-side interviews against transactional supplier data and classification records. This multi-source approach permits high-confidence inferences about both cost structures and likely certification timelines—without relying on single-source declarations.

Concretely, PW Consulting combines: (a) cross-referenced patent citation mapping to identify emergent layup and resin technologies; (b) proprietary supplier-scan tools that monitor certification filings and equipment upgrades; and (c) structured interviews with Tier-1 buyers and class society technical officers. These layered inputs allow us to surface non-public signals—such as planned capacity shifts and implicit lead-time risks—while preserving supplier confidentiality and limiting exposure of sensitive contract-level data.

Strategic Recommendations for 2026

For corporate leaders allocating capital and shaping product roadmaps in 2026, PW Consulting recommends a three-track approach:

- Protect immediate tender-readiness: prioritize certification sequencing and certified subsystem co-validation agreements to defend near-term revenue streams.

- Build optionality at the material and supplier level: implement BOM scenarios and dual-sourcing pilots that can be switched on under supply stress without incurring recertification penalties.

- Invest selectively in automation that reduces per-unit labor intensity and improves reproducibility of complex laminates—targeted investments deliver measurable yield benefits within 12–24 months.

Each recommendation is anchored to the report’s practical toolset: supply-chain maps, yield-adjustment models, and BOM decomposition logic—so teams can move from strategy to execution in quarter-scale timelines.

What Stakeholders Will Gain

Readers who act on the report will be able to:

- Quantify the impact of certification sequencing on time-to-revenue for new composite products.

- Stress-test supplier portfolios for 2026 regulatory and logistics shocks.

- Calibrate CAPEX on automation and qualification with scenario-based ROI models that account for evolving material mixes and product weight targets.

Next Steps and How to Access the Full Intelligence

PW Consulting’s Marine Composites Market report is deliberately deep on actionable frameworks and diagnostic assets while reserving granular company-level projections and full regional/application splits for subscribers. To review the complete segmentation maps, BOM templates, and supplier-level appendices, access the full report at https://pmarketresearch.com/auto/marine-computers-market.

For boards and strategy teams preparing capital plans or supplier RFPs in 2026, the combination of market-sizing (USD 5.6 Billion in 2025; ~USD 8.3 Billion by 2032 at a 5.9% CAGR), concentration metrics (CR3 32.4%, CR5 44.8%), and the operational playbooks in this study will materially reduce execution risk and accelerate compliant product launches under tightened regulatory scrutiny.

For detailed analysis of this topic, please visit the official page: Marine Composites Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.