PW Consulting: Gypsum Board Market to Rise from USD 124.2 Million in 2025 to USD 158.6 Million by 2032 at a 3.6% CAGR

Gypsum Board Market 2026: Strategic Imperatives for Capital Allocation

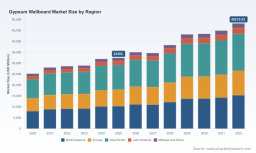

The global gypsum board market is at an inflection point in 2026. After a transient downturn in 2024, the market rebounds to an estimated USD 124.2 Million in 2025 and is projected to grow to roughly USD 132.9 Million in 2026, following a 3.6% compound annual growth rate across the 2026–2032 forecast window. These headline metrics mask diverging dynamics across supply chains, regulatory regimes, and product stacks — dynamics that materially affect capital deployment, M&A timing, and factory modernization choices this year.

Gypsum Board Market

Why 2026 demands proactive capital decisions

Three concurrent forces are compressing the decision window for investors and operators:

-

Cost & input volatility: stable-but-elevated US producer price indices and structural shifts in gypsum sourcing (including significant volumes of synthetic gypsum) are reconfiguring feedstock economics.

-

Regulatory friction: recent trade-policy moves and tax-rebate changes in key exporting markets are reshaping cross-border arbitrage and export competitiveness.

-

Consolidation pressure: a moderately concentrated supplier base is heightening the payoff from scale, proximity to raw gypsum reserves, and aftermarket channels.

Market posture and concentration

As of 2026, the sector exhibits mid-tier concentration: the top-three firms account for roughly 53.4% of industry volume, and the top-five approach 64.8%. This structure rewards incumbents with integrated supply chains and regional manufacturing footprints while leaving tactical opportunities for niche players that can secure design wins or localized feedstock advantages.

Macro and trade context affecting 2026 decisions

-

Raw material balance — The US industrial picture shows producer-price stability (PPI ~362.3 in March 2026) alongside large volumes of both mined and synthetic gypsum used in wallboard manufacture; these inputs create a two-track supply dynamic for cost and sustainability planning.

-

Export regime shifts — Recent policy changes, for example the cancellation of certain export tax rebates by a major exporter effective April 1, 2026, and continued anti-dumping frameworks in export destinations, are narrowing arbitrage windows and elevating near-term logistics risk.

-

Industry capex signals — Greenfield and brownfield investments announced in 2025–2026, including large-scale modernization projects and new plants in resource-rich locations, indicate that firms are prioritizing unit-cost reduction and regional self-sufficiency.

Recent developments shaping 2026 strategy

-

Major capacity investments are underway: a North American producer disclosed a USD 330.0 Million modernization and expansion program (plant restart and ramp toward H2 2027), signaling aggressive cost-reduction focus via local gypsum integration and process upgrades.

-

Pricing moves are active: leading suppliers announced price adjustments in early 2026, a clear market response to cost pass-through needs and capacity repositioning.

-

Regional partnerships are materializing: a European-origin materials group entered a joint venture to establish a new plant in the Middle East with an initial investment in the low tens of millions of euros, highlighting strategic localization to access raw gypsum reserves and shorten supply chains.

What PW Consulting’s report delivers — practical toolset, not theory

Our market report is built around practitioner tools meant to be immediately operationalized by purchasing, operations, and corporate development teams. Key deliverables include:

-

Supply-chain maps that trace ore-to-panel flows, logistics choke points, and single-source dependencies at plant and port level.

-

BOM decomposition logic that converts panel specifications into cost buckets and sensitivity drivers so teams can stress-test margin outcomes against feedstock and energy scenarios.

-

Yield-adjustment models that allow plant managers to simulate how minor changes in calcination or line throughput affect finished-panel tonnage and unit cost.

-

Technology roadmaps that categorize near-term process upgrades (digital sensors, AI process control, dryer optimization) against capital intensity and payback horizons.

These instruments are presented as configurable modules so that a CFO or plant manager in 2026 can translate macro forecasts into cash-flow scenarios, capital prioritization lists, and compliance risk matrices without having to rebuild the analytical backbone.

How these tools solve 2026 pain points

-

Cost control: BOM and yield modules expose which line items deliver the largest margin leverage, enabling targeted retrofit versus full-line replacement decisions.

-

Compliance & trade risk: supply-chain maps combined with customs and tariff overlays let supply managers quantify the impact of export-tax reversals and anti-dumping indices on sourcing strategies.

-

Capacity & timing: plant-level capacity models and scenario simulations help planners reconcile announced expansions with regional demand rebounds, reducing the risk of overbuild or under-utilization.

Competitive landscape — what to watch beyond the logos

Our analysis centers on the competitive dimensions that determine winners in design wins and long-term profitability. Across the leading firms — global industrial groups, regional champions, and resource-integrated producers — we see a set of repeatable advantage types:

-

Integrated feedstock advantage: firms with captive gypsum mines or secure synthetic-gypsum supply contracts achieve a lower and more predictable cost base.

-

Scale & logistics moat: large-scale producers leverage distribution density and national dealer networks to accelerate construction-spec adoption and lock in retrofit projects.

-

Product & specification edge: companies that bundle certification-ready fire and moisture resistant systems with technical design support tend to win institutional and commercial projects.

-

Sustainability positioning: early adopters of low-carbon calcination and recycled-content panels convert ESG credentials into specification wins in green building markets.

-

Local-market agility: nimble regional producers use JV structures and local sourcing to circumvent trade friction and capture fastest-growing segments.

PW Consulting’s proprietary workbench identifies which firms exhibit which combination of moats, and where capability gaps create acquisition or partnership opportunities for buyers. For specific firm-level design-win factors and comparative matrices, access the full dataset here: Access the full market study .

Methodology — how we derive hard-to-find inputs

Our conclusions rest on layered triangulation: we synthesize primary interviews (C-suite, plant managers, major distributors), plant-level audits, customs and import-export reconciliations, satellite imagery for capacity verification, and machine-processed patent and standards filings. We then validate these inputs against manufacturer-reported throughput and public financial statements, applying cross-check filters to flag outliers.

Crucially, our supply-chain and BOM reconstructions incorporate confidential supplier contract summaries and anonymized field measurements obtained under non-disclosure agreements, allowing us to model real operating yields and cost structures rather than relying on high-level averages. This methodology is described in full in the report’s methodology annex so clients can replicate and stress-test our scenarios.

Strategic playbook for 2026

-

Prioritize capex that reduces unit energy and feedstock cost per panel rather than broad capacity expansion, unless capacity addresses a clear regional feedstock mismatch.

-

Assess partner or JV routes in resource-rich countries to mitigate export-tax and tariff risk, using local plant builds as a hedge against cross-border volatility.

-

Target small-to-medium acquisitions that close distribution gaps or secure synthetic-gypsum supply; such deals often unlock faster paybacks than greenfield plants.

-

Invest selectively in AI-enabled process control where yield models show high sensitivity to kiln and dryer variance; these upgrades can materially shorten payback when energy input is a dominant cost.

-

Embed compliance scenarios into all procurement models to ensure pricing decisions account for potential tariff or rebate shifts in the next 12–24 months.

Next steps — how to use our report

For corporate development teams, the report’s transaction-ready modules include valuation overlays, asset comparables, and integration checklists. For operations leaders, the plant-level yield and BOM tools provide retrofit decision matrices and vendor scorecards. For purchasing and sustainability officers, the supply-chain maps and low-carbon scenario paths enable supplier segmentation by risk and ESG scoring.

To receive the complete distribution of regional, type, and application splits — and to unlock the full set of downloadable models and plant-level dashboards — please consult the full PW Consulting study: Access the full market study .

Closing perspective — decisive but disciplined action in 2026

2026 is a year where incremental improvements in yield and supply security can compound into material margin gains. The market’s modest but steady growth (3.6% CAGR over the forecast horizon) rewards firms that combine capital discipline with surgical investments in feedstock security, process intelligence, and regional partnerships. PW Consulting’s deliverables are designed to convert these strategic priorities into executable projects — calibrated to risk tolerances, regulatory realities, and the competitive landscape that will define success this year.

For detailed analysis of this topic, please visit the official page: Gypsum Board Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.