PW Consulting Forecasts Fiber Reinforced Concrete Market to Reach USD 2915.0 Million by 2032, New Report Reveals

Fibre Reinforced Concrete Market 2026: Strategic Imperative for Capital Allocation

The global Fibre Reinforced Concrete (FRC) market is at an inflection point in 2026. After expanding from USD 1,350.3 Million in 2020 to USD 1,820.0 Million in 2025, the market is now projecting continued expansion at a 7.1% compound annual growth rate (CAGR) across the 2026–2032 forecast window, approaching an estimated USD 2,915.0 Million by 2032. This growth trajectory is driven by code acceptance, materials innovation and a shifting project mix—factors that make 2026 a critical year for capital allocation decisions, procurement redesigns and compliance investments.

Fiber Reinforced Concrete (FRC) Market

Macro Dynamics Shaping 2026 Decisions

Several macro forces converge in 2026 to create both opportunity and risk for FRC market participants:

- Standards and design codes: Mainstream structural codes increasingly recognize fibre-based reinforcement. Examples include ACI provisions that permit FRC as an alternative to rebar in specific slabs and the fib Model Code alignment—both of which accelerate institutional demand for certified FRC solutions.

- Raw-material pressure: Global production of key inputs—cement and crude steel—continues to influence cost baselines. The scale of cement production and steel output that underpins fibre costs transmits through supplier pricing and warrant strategic hedging.

- Trade and compliance: Trade measures such as steel tariffs and localized content rules reshape supply-chain design. Import duties remain an active variable in procurement strategies for 2026 projects, particularly in regions with high infrastructure spend.

- Certification and performance validation: Recent product certifications under new ASTM standards and similar regimes are shortening buyer approval cycles, tilting procurement toward suppliers with recognized test footprints.

Where growth momentum is located (high-level)

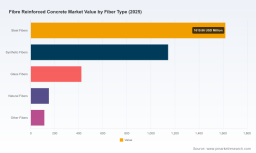

Demand growth is concentrated where public infrastructure funding, precast adoption and industrial flooring modernization intersect with regulatory acceptance. The report maps these growth centers and overlays project pipelines to signal where near-term volume and margin opportunities concentrate — the full geographic and application distribution charts are available in the full report.

Technology and Materials Evolution

Technology advances are broadening the FRC value proposition beyond crack control:

- Fiber chemistry and hybridization: Developments in macro- and micro-fiber blends enable replacement of conventional reinforcement in select designs while improving constructability and reducing labor.

- Coating and alkali resistance: New surface treatments and glass formulations are improving durability in aggressive environments, with certain suppliers obtaining certifications that accelerate adoption for bridges and hydraulic works.

- Digital quality control: AI-driven vision systems and predictive yield models are reducing variability in fiber dispersion and dosage control on batching lines.

- Manufacturing upgrades: Automated dosing, inline monitoring and powder handling upgrades reduce waste and lower per-unit cost when combined with process reengineering.

Practical Tools in Our Report — Built for Action in 2026

PW Consulting’s FRC Market report is designed as a decision-support toolkit rather than a static narrative. Key practical deliverables included:

- Supply-chain topology and risk heatmaps that identify single points of failure and tariff exposure across sourcing corridors.

- Bill-of-Materials (BOM) disassembly logic that translates product specs into actionable procurement line-items, enabling procurement teams to model substitution scenarios without compromising design intent.

- Yield adjustment and margin model templates that quantify the economics of dosage, waste, and labor across common mixing and finishing methods.

- Technology roadmaps that link short-term certification milestones to medium-term manufacturing investments and product R&D priorities.

- Supplier scorecards and design-win playbooks for project-level commercialization, focused on technical pitch points, testing timelines and spec approvals.

Each tool is accompanied by scenario-based worksheets so teams can stress-test cost-control measures, compliance pathways and CAPEX trade-offs under realistic 2026 constraints.

Competitive Landscape: Strategic Dimensions, Not Predictions

The FRC supplier field combines global platform players with specialist innovators. Market concentration is moderate: the combined share of the top three suppliers is roughly 28.5%, and the top five account for about 35.2%, indicating room for regional leaders and niche specialists to capture design wins.

Our competitor analysis evaluates firms across several defensible dimensions without prescribing exact 2026 moves:

- Scale and integrated manufacturing: Suppliers with upstream steel or polymer integration reduce exposure to commodity cycles and can price aggressively on volume projects.

- Certification and standards moat: Companies that secure ASTM and national approvals shorten time-to-spec and increase procurement stickiness for institutional buyers.

- Material and product breadth: Firms offering multi-material platforms (steel, synthetic, glass) win on technical flexibility when projects require hybrid solutions.

- Design-win capabilities and technical support: Suppliers that embed application engineering into bidding teams capture early-stage specs and long-tail maintenance agreements.

- Regional footprint and service logistics: Localized production reduces landed costs and mitigates tariff impacts for large infrastructure pipelines.

These dimensions are visible in the public footprint and recent activity of leading firms. Examples of illustrative developments include a prominent steel-fiber exhibitor demonstrating sustainable tunnelling solutions at a major concrete show, a multi-material provider refreshing its product catalog for precast applications, and a global chemistry group obtaining bridge-related certification under current ASTM regimes—signals that product innovation and compliance are active competitive levers.

For a side-by-side capability map and supplier scorecards that explain how these dimensions convert into commercial outcomes, see the full dataset and interactive matrices: Access the full report .

Methodology — Why our conclusions are action-ready

PW Consulting’s methodology is built on layered triangulation and traceable verification. We combine patent and standards citation analysis, multi-year procurement and customs shipment data, third-party testing records and confidential interviews with OEMs, contractors and procurement heads to reconstruct both installed capacity and demand pull. Our approach includes:

- Patent and technical literature mapping to identify where material innovation converges with manufacturable designs.

- Proprietary BOM reverse engineering and lab validation to translate supplier claims into field-relevant performance metrics.

- Field-level verification through plant tours, sample testing and contract-disclosure cross-checks to calibrate our cost and yield models.

We emphasize how we obtain non-public inputs: controlled disclosure interviews under NDA, licensed customs and shipment feeds, and controlled access to supplier test results. These inputs are synthesized with public filings and standards updates to produce the reproducible models included in the report.

Strategic Guidance for 2026 — Where to Act Now

As firms set budgets for 2026, the following high-level moves deserve priority attention:

- Re-orient procurement to mitigate tariff exposure: model landed-costs under alternative sourcing scenarios and prioritize localized production for high-volume segments.

- Invest in certification and application testing where code acceptance accelerates adoption; certification is a multiplier for volume capture in institutional projects.

- Embed AI and inline QC to improve fibre dispersion yields and reduce rework; invest the savings into customer-facing service bundles that support design wins.

- Target design-win investments early: allocate engineering resources to project spec committees and precast partners where design substitution windows exist.

- Operationalize ESG levers: recycled content and embodied-carbon reporting are increasingly required by large owners; product claims must be verifiable and traceable.

Conclusion and Next Step

2026 is a make-or-break year where standards alignment, material innovation and supply-chain design conspire to reshape competitive advantage in FRC. PW Consulting’s report equips executives with the tools to convert market signals into executable procurement, manufacturing and commercial strategies. For complete regional and application distributions, supplier scorecards, and downloadable financial templates, consult the full deliverable: Access the full report .

For detailed analysis of this topic, please visit the official page: Fiber Reinforced Concrete (FRC) Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.