PW Consulting: Data Loggers Market at USD 621.0 Million in 2025, Poised to Reach USD 1,003.7 Million by 2032 at a 7.1% CAGR

Data Loggers Market 2026: Strategic Preview from PW Consulting

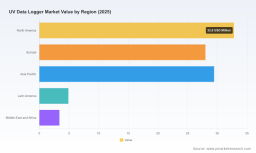

PW Consulting releases a concise strategic briefing drawn from our forthcoming Data Loggers Market report, setting the decision framework for enterprises allocating capital and operational focus in 2026. The global UV and environmental data logger market is in a sustained growth phase — up from USD 440.2 Million in 2020 to USD 621.0 Million in 2025 — and is projected to approach USD 1,003.7 Million by 2032 at a compound annual growth rate (CAGR) of 7.1%. This briefing previews the report’s practical value for procurement, product, and compliance leaders while preserving the detailed segment-level intelligence for subscribers.

Executive Snapshot — Why 2026 Is a Strategic Inflection

Three structural forces make 2026 a decisive year for players and buyers of data logging solutions:

- Regulatory and validation intensity in healthcare and pharma is increasing, elevating demand for traceable UV and environmental measurement.

- Supply-chain pressure and component cost volatility force manufacturers to re-evaluate BOM composition, sourcing geographies, and yield optimization levers.

- Operationalization of cloud-native monitoring and tighter ESG reporting requirements means buyers now prioritize lifecycle cost and data integrity over unit price alone.

These forces are driving market expansion and complexity: from a market base of USD 621.0 Million in 2025 to an expected USD 687.0 Million in 2026, the sector requires targeted capital allocation to win design slots and ensure compliance continuity.

Market Dynamics and Compliance Drivers

Regulatory and standards developments reshape procurement criteria for 2026:

- Traceable calibration is becoming non-negotiable in regulated environments. Certain suppliers already offer PTB-traceable calibration aligned with ISO/CIE workflows, which materially reduces validation friction for customers in medical and disinfection use cases.

- UV data logging is increasingly embedded into environmental validation programs alongside temperature and humidity monitoring, expanding scope for integrated sensor systems in hospitals, pharmaceutical storage, and biotech labs.

- Cloud connectivity and real-time alerting are evolving from convenience features to audit-enabling capabilities — buyers now expect secure, tamper-evident data export paths as part of validation records.

These regulatory realities create first-mover advantages for vendors that combine measurement traceability, robust firmware, and enterprise-grade telemetry.

What the Report Contains — Practical Tools, Not Just Charts

The full report goes beyond topline forecasts to deliver executable intelligence for procurement, engineering, and compliance teams. Key deliverables include:

- Supply-chain maps showing tiered supplier relationships and substitution pathways for critical components.

- BOM teardown logic that isolates high-impact parts by cost, lead-time risk, and compliance sensitivity.

- Yield-adjustment and TCO models that simulate the impact of component yield, calibration cycles, and firmware rework on unit economics.

- Technology roadmaps that position sensing modalities (broadband UV, UVA/UVB/UVC distinctions), power management, and connectivity upgrades against adoption timelines.

- Calibration-compliance matrices linking measurement accuracy, calibration traceability, and audit workflows for regulated end markets.

Each tool is designed to be operational: procurement teams can use the supply-chain map to create dual-source strategies; engineering can use BOM logic to prioritize re-engineering for cost-downs; and quality/compliance can use the calibration matrix to shorten validation cycles. For readers seeking the full distribution maps, interactive dashboards, and scenario inputs, please consult the complete dataset here: Access the full report and dashboards .

Competitive Landscape — Dimensions of Advantage (Not Predictions)

The market exhibits a moderate concentration dynamic (CR3 29.8%, CR5 32.1%), indicating room for specialized incumbents and focused new entrants. Our competitive analysis emphasizes the structural dimensions that determine long-term success rather than one-off forecasts:

- Measurement credibility and traceability — Suppliers that embed PTB-traceable calibration and maintain auditable calibration chains enjoy lower commercial friction in regulated procurement cycles.

- Connectivity and platform stickiness — Cloud-enabled telemetry and alerting, when paired with robust data integrity controls, create switching costs through integration with validation workflows and centralized monitoring platforms.

- Power and operational longevity — Battery life, low-power sensing and firmware over-the-air update strategies materially influence total cost of ownership, especially for distributed deployments such as moving goods or remote facilities.

- Channel and service reach — Companies with direct enterprise service capabilities or certified distribution partners accelerate design wins in healthcare and industrial accounts where on-site validation is required.

Illustratively, vendors in the sample set differentiate along these axes: some emphasize traceable calibration and long-term field autonomy; others emphasize cloud-native monitoring and integrated alerts. These are defensive and offensive levers any strategic buyer should evaluate when committing to multi-year contracts.

Selected Vendor Archetypes (Illustrative Capabilities)

- Precision-calibration specialists that deliver PTB-traceable sensors and long battery life—appeal to sterilization and medical-technology users requiring rigorous validation traces.

- Platform-oriented vendors offering cloud connectivity and integrated alerting—appeal to centralized operations teams and third-party logistics providers.

- Cost-optimized device makers focusing on compact BOMs and USB-centric data capture—appeal to high-volume, low-margin applications where ease-of-use dominates.

For a detailed comparative matrix and decision rubric that maps vendor capabilities to procurement evaluation criteria, see the full analysis at: Access the full report and dashboards .

Methodology — Why Our Conclusions Are Actionable

PW Consulting’s findings rest on a layered-triangulation methodology designed to surface both public and non-public signals with high fidelity. In 2026 we combine patent citation analysis, multi-stage supplier interviews, controlled BOM teardowns, and calibration validation tests to ensure internal consistency across datasets. Key elements include:

- Patent and standards mapping to identify emerging sensing and power-management innovation vectors.

- Vendor and channel interviews across R&D, procurement, and QA functions to capture contract structures, lead-times, and validation pain points.

- Lab-based BOM teardowns and calibration verification to quantify practical trade-offs between component choice and measurement integrity.

Our layered approach reconciles public filings with primary-source observations, enabling confident scenario modeling for capital allocation and product planning without exposing client-sensitive information. This is why the report’s practical tools are directly implementable by procurement and product teams facing 2026 validation and cost pressures.

Strategic Imperatives for 2026

Based on our analysis, executives should prioritize three near-term actions:

- Lock calibration certainty: Require PTB-traceable or equivalent calibration documentation in RFPs for regulated deployments. This reduces audit rework and shortens deployment timelines.

- Stress-test BOMs under supply disruption scenarios: Use yield-adjustment models to understand margin sensitivity and to identify components where dual-sourcing or design substitution has disproportionate impact.

- Assess data governance as part of procurement: Evaluate telemetry platforms for tamper evidence, export control compatibility, and ESG-aligned lifecycle reporting.

These imperatives help convert the market’s growth — a projected rise to USD 687.0 Million in 2026 and onward to USD 1,003.7 Million by 2032 — into disciplined investment and defensible product choices.

Invitation to Deeper Intelligence

Our full report contains the granular maps, interactive models, and supplier-specific matrices required to execute the recommendations above. PW Consulting provides customized briefings and scenario workshops to operationalize the insights for procurement, engineering, and strategy teams. Access the full dataset, vendor matrices, and scenario tools here: Access the full report and dashboards .

Closing Note

2026 is a year of converging pressures — regulatory rigor, supply fragility, and platform-enabled monitoring — that will reconfigure design wins and procurement criteria in the data logger market. PW Consulting’s Data Loggers Market report equips leaders with the analytical tools and evidence base to convert market growth into durable advantage while avoiding common pitfalls that increase compliance and cost exposure.

For detailed analysis of this topic, please visit the official page: Data Loggers Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.