PW Consulting: Carbon Brush Market Forecast to Expand at a 4.1% CAGR Through 2032 Amid Rising Motor and Asia‑Pacific DemandPW Consulting: Embroidery Machine Market to Expand at a 3.3% CAGR, Signaling Steady Opportunities for Manufacturers

PW Consulting: Carbon Brush Market — 2026 Strategic Outlook and Decision-Grade Toolkit

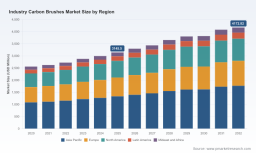

In 2026 the carbon brush market stands at a decisive inflection: the sector is recovering from raw-material volatility while adapting to stricter standards and the slow but persistent displacement risk from brushless architectures. PW Consulting’s latest market study shows the global market reached USD 301.2 Million in 2025 and is forecast to grow at a 4.1% CAGR through 2032, approaching roughly USD 400.0 Million by the end of the forecast window. This briefing summarises the report’s strategic value for executives and investors making allocation decisions in 2026 — showcasing the analytical depth while preserving the report’s proprietary segment detail to drive you to the full dossier.

Carbon Brush Market

Executive snapshot — why 2026 matters

The business case for near-term action is compact and urgent. The market is not collapsing, but it is undergoing structural shifts that change where margin and growth will accrue:

Carbon Brush Market

- Raw-material price instability has transmitted proportionally large cost shocks into producer P&Ls, forcing re‑pricing, supplier consolidation and tighter inventory governance.

- Regulatory tightening and newer test protocols are increasing the compliance bar for rotating electrical contacts, shifting procurement emphasis toward certified suppliers and audited BOMs.

- Electrification in heavy industries (notably wind and industrial drives) creates pockets of above-market demand even as certain end-markets accelerate brushless conversions.

- The competitive landscape remains moderately concentrated (CR3 ~48.0%; CR5 ~55.0%), enabling leading suppliers to extract design‑win premiums where they hold material or systems advantages.

Primary strategic implications for 2026 decision-makers

Executives, procurement chiefs and PE sponsors will find three immediate, actionable implications:

- Cost-to-serve is now a board-level metric. With raw materials representing a large share of manufacturing cost, companies that can demonstrate transparent, hedged supply chains and adaptive BOMs will protect margin.

- Design wins are multi-dimensional. Buyers select suppliers based on a combination of materials science, test certification, aftermarket service and the ability to secure long‑term performance on high‑value rotating assets.

- Regulatory and ESG compliance is a gatekeeper for market access. Proactive testing alignment to contemporary IEC/CENELEC standards reduces rework risk and shortens qualification cycles for OEM platforms.

Report toolset — what makes this study operational for 2026

The report is intentionally built as an execution toolkit rather than a passive desk reference. Key deliverables are designed to bridge analysis and implementation:

- Supply‑chain map with supplier tiering and risk heat‑maps — structured to support near-term hedging, dual-sourcing decisions and inventory optimisation.

- BOM decomposition logic and reverse‑engineering playbook — enabling buyers and manufacturers to derive substitution pathways and cost-down opportunities without compromising performance spec.

- Yield-adjustment and sensitivity model — a parameterised spreadsheet framework for testing the P&L impact of material price swings, yield improvements and tariff changes across multiple production footprints.

- Technology roadmap and materials R&D tracker — aligning grades, coatings and holder-system innovations to anticipated regulatory and reliability requirements through 2032.

Each tool is accompanied by an implementation checklist that maps short-term actions (0–12 months) to medium-term initiatives (12–36 months), allowing teams to prioritise based on cash-flow and contract exposure.

Competitive landscape — dimensions that determine winners in 2026

Rather than offering point forecasts for individual firms, PW Consulting’s competitive analysis dissects the strategic dimensions that govern success in 2026. These dimensions are consistent across the universe of incumbent and challenger suppliers:

- Materials engineering moat — firms with proprietary grade libraries and application-specific formulations convert higher conversion rates for motors and generators that require extreme endurance.

- Standards and qualification capability — suppliers that maintain deep certification pipelines (test labs, traceable material batches) shorten OEM qualification cycles and command a price premium.

- Systems integration and aftermarket services — the ability to supply brush assemblies, spring systems and lifecycle support creates stickiness and recurring revenue.

- Regional production footprint and supply resilience — proximity to OEM clusters and flexible production scales are decisive when lead times and compliance checks tighten.

Selected players illustrate these dimensions:

- Morgan Advanced Materials — deep materials engineering and a broad industrial portfolio produce a materials‑led moat that supports high‑value design wins.

- Mersen — certification breadth and standards alignment create a quality‑assurance advantage in regulated industrial applications.

- Schunk Carbon Technology — systems and customised assemblies position the firm well for transport and engineered applications where integration is rewarded.

- Helwig Carbon — a US‑centric, service‑oriented model that excels in rapid customisation and aftermarket responsiveness.

- Toyo Tanso & AVO Carbon — niche technical strengths (small motor grades; automotive-focused design centres) that support segment-specific adoption.

This dimensional framing explains why certain suppliers capture higher margins without disclosing proprietary forecasts — and it is the analytical logic purchasers and investors need when structuring contracts or sizing positions in 2026.

Raw-materials, cost mechanics and supply risk

Two cost facts anchor the market: graphite and related inputs are volatile, and material costs account for a large share of production expense. Historical dislocations (2022–2024) saw large swings that materially affected producers’ cash flows and prompted tactical hedging and supplier consolidation.

- Price volatility compresses entry-level margins and accelerates supplier rationalisation where firms lack vertical integration or secured long-term off-take.

- Procurement levers that matter in 2026 include strategic inventory sizing, multi-sourcing from geographically diverse mills, and accelerated material substitution trials supported by lab validation.

Regulation and standards — compliance as competitive advantage

Regulatory updates impacting rotating electrical contacts are changing supplier selection criteria. New and updated test protocols are increasing certification costs and elongating qualification windows.

- Compliance readiness — alignment to the latest IEC/CENELEC protocols is now a procurement prerequisite for many OEMs.

- Testing infrastructure and documented traceability shorten time-to-design-win and mitigate retrofit risk on critical rotating equipment.

Methodology — how PW Consulting derives decision‑grade insight

Our conclusions rest on Layered Triangulation, a multi-step validation process that integrates primary and secondary sources to reconstruct supply and demand flows with high confidence. This methodology includes:

- Primary interviews with OEM purchasers, Tier‑1 integrators and select plant managers to capture procurement behaviours, qualification hurdles and spot pricing signals.

- Patent and technical literature citation analysis to map innovation clusters and anticipate material/grade substitution trajectories.

- Reverse BOM analysis and targeted production audits to validate materials shares, yield profiles and assembly labour contributions.

- Customs flow and shipment analytics to detect regional shifts in capacity and to triangulate supplier footprints where public disclosures are limited.

Critically, our approach emphasises how we access non-public information — while respecting confidentiality — through anonymised supplier benchmarking, controlled NDA interviews and laboratory verification protocols. The result is a reproducible, transparent evidence chain that supports commercial decisions without publishing sensitive client-level data in the public domain.

Practical next steps for 2026 allocators

For management teams and investors allocating capital in 2026 the tactical roadmap is straightforward:

- Prioritise suppliers with demonstrable certification pathways and localised production options to reduce time-to-market and compliance exposure.

- Stress-test portfolios against at least two raw‑material stress scenarios and require suppliers to demonstrate hedging or substitution plans as part of commercial contracts.

- Target acquisition or partnership opportunities where technology integration (brush‑holder systems, coatings, aftermarket services) creates immediate cross-sell potential.

Get the full diagnostic and implementation kit

PW Consulting’s full report provides the granular segmentation maps, supplier scorecards, and the Excel-based yield and sensitivity models that enable operational execution in 2026. To review the complete set of maps, charts and the implementation checklist, download the report here: PW Consulting — Worldwide Carbon Brushes Market Research .

Contact our industry team for a short briefing tailored to your portfolio or procurement priorities — we can run a 90-minute, decision-focused workshop that uses the report’s models on your data to produce near-term action plans.

For detailed analysis of this topic, please visit the official page: Carbon Brush Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.