PW Consulting: Anti‑Vibration Mounts Market Set to Expand at 3.6% CAGR Through 2032, New Insight Report Reveals

Anti‑Vibration Mounts Market 2026: Strategic Imperatives for Capital Allocation

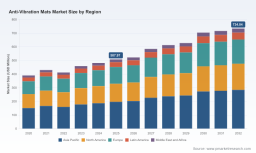

PW Consulting's latest market brief on anti‑vibration mounts (base year 2025) frames the opportunity set for corporate decision‑makers allocating capital in 2026. The global market is at a measured growth inflection: total revenues reach USD 5,595.0 Million in 2025 and, under current trajectories, expand to USD 7,117.0 Million by 2032 at a 3.6% CAGR. These headline figures mask dynamic pockets of disruption driven by raw material swings, tightening safety and sustainability mandates, and the re‑engineering of OEM procurement strategies — each of which has immediate implications for M&A, product investments, and supply‑chain de‑risking programs.

Anti-Vibration Mounts Market

Executive snapshot: Why 2026 matters

For executives, 2026 is not a planning year to defer. Cost volatility in elastomers, new retail and building standards referencing vibration control, and accelerated factory automation converge to make vibration control both an operational risk and a measurable value lever. Investors seeking durable returns will prioritise firms and assets with demonstrable design‑win pipelines, validated qualification processes, and low execution risk on raw materials and compliance. PW Consulting’s report acts as a decision support toolkit — revealing where to place bets while withholding the granular split tables to drive direct engagement with our full study.

Key takeaways

-

Market momentum is steady: the market base in 2025 is substantial and expands at c. 3.6% p.a. through 2032, reflecting steady replacement cycles and growing industrial/rail adoption.

-

Concentration is material: the top three firms capture roughly 65.0% of revenue, and the top five about 70.0%, underscoring the importance of scale in qualification and distribution.

-

Cost and compliance are twin priorities: raw material trends and evolving retail/industrial regulations are shifting procurement and design criteria in 2026.

-

Report value: PW Consulting supplies operational tools (supply‑chain maps, BOM teardowns, yield‑adjustment models, and technology roadmaps) designed to convert the market view into executable programs.

Market dynamics — what is driving growth and where risk is concentrated

Growth in 2026 is shaped by three observable dynamics:

-

Material economics: Elastomer feedstock moves the margin needle. In late 2025 US neoprene rubber prices increased following a 6.1% rise in butadiene feedstock costs, while natural rubber showed a downtrend through 2025 that is expected to firm heading into 2026. Manufacturers with diversified raw‑material sourcing or validated recycled‑rubber strategies face a lower unit‑cost tail risk.

-

Regulatory and procurement shifts: Retail sustainability standards and industrial safety regulations are elevating the specification bar for vibration control components. A notable example — a 2025 update to household‑product guidelines now references anti‑vibration mats for washing machines as part of sustainability and noise‑control criteria — forces retail‑channel suppliers to document performance and lifecycle attributes.

-

Capital deployment patterns: Buyers are prioritising partner credentials that reduce qualification time (test reports, compliance dossiers) and improve supply resilience (dual sourcing, local inventory buffers). This raises the value of suppliers with demonstrable certification portfolios and regional manufacturing footprints.

Practical tools inside the report — how PW Consulting converts insight into action

The report is structured to move executives from diagnosis to execution. Key operational modules include:

-

Supply‑chain maps: visualised tier‑1 through tier‑3 supplier flows, choke‑point heatmaps and alternative sourcing routes to quantify substitution cost and time.

-

BOM teardown logic: component‑level cost build‑ups for representative product families, including material mix sensitivity analysis (SBR, neoprene, recycled rubber) and labor/overhead footprints.

-

Yield‑adjustment and NPI models: templates that convert lab yield changes and qualification delays into P&L and cash‑flow impacts for 12–36 month planning horizons.

-

Technology roadmaps: staging of material innovations, bonding/adhesion advances, and tooling investments with trigger conditions tied to price or regulatory thresholds.

-

Compliance and ESG matrices: requirement matrices aligned to retail and industrial standards to fast‑track design approvals and tender responses.

Each tool is purpose‑built to address 2026 pain points: controlling input cost volatility without sacrificing performance, shortening time‑to‑market under stricter specs, and quantifying the return on sustainability investments. For organisations that require immediate implementation templates, the report provides executable playbooks rather than abstract recommendations.

Competitive landscape — the dimensions that determine winners

Our competitive analysis focuses on structural advantages rather than short‑term tactics. Across incumbent and regional players we observe five repeatable competitive dimensions that define success in 2026:

-

Technical certification moat — companies that hold specialised rail and automotive qualifications (e.g., high‑density SBR/polyurethane systems for rail ballast isolation) shorten OEM qualification time and command premium positioning.

-

Manufacturing precision and quality systems — advanced facility controls and traceability are table stakes for precision industrial applications where vibration tolerances are tight.

-

Material and circularity capability — suppliers with validated recycled‑rubber processes or multi‑feedstock recipes reduce exposure to feedstock price shocks and appeal to ESG‑led procurement teams.

-

Channel and logistics reach — a distributed production footprint and deep distribution partnerships accelerate design wins in geographically diverse installation markets.

-

Service and application engineering — the ability to deliver installation guidance, lifecycle testing, and failure‑mode analytics frequently decides competitive outcomes in retrofit and OEM bids.

Representative firms exemplify these dimensions: specialised rail‑focused manufacturers demonstrate deep product certification and material expertise; German precision suppliers show advantage in tolerance‑sensitive machinery pads; multinational groups leverage scale and product breadth to serve cross‑sector needs; smaller regional players compete on lead‑time and price for local projects. PW Consulting’s proprietary vendor scoring framework quantifies these dimensions to help buyers and investors prioritise targets without disclosing client‑sensitive projections here.

To examine detailed company profiles, capability scorecards and comparative decision matrices, consult the full study at Worldwide Anti‑Vibration Mats Market Research .

Scenario planning — three actionable scenarios for 2026 capital deployment

-

Consolidation play: Target assets with complementary certification stacks or regional footprints to accelerate access to higher‑growth institutional channels. Prioritise targets where integration unlocks rapid qualification cross‑selling.

-

Vertical resilience: Invest in suppliers with validated recycled‑rubber lines or alternative polymer pathways to reduce feedstock exposure. Use our BOM teardown and supplier‑cost curve to stress‑test deal assumptions.

-

Service differentiation: Acquire or partner with firms offering application engineering and lifecycle analytics to convert product sales into recurring service revenue and improve design‑win stickiness.

Methodology — layered triangulation and data provenance

PW Consulting’s 2026 study employs a layered triangulation methodology to ensure outcomes are actionable and auditable. Core elements include:

1) Primary research: structured interviews with more than 40 OEMs, tier‑1 purchasers, and regional distributors; NDA‑protected supplier audits; and factory walkthroughs where we validate bonding, curing, and density controls. 2) Technical verification: laboratory BOM teardowns and accelerated life‑cycle testing under controlled vibration profiles to map failure modes and yield impacts. 3) Secondary validation: aggregated customs and shipment data, patent citation analysis, and machine‑assisted harvesting of regulatory filings to reconcile unit economics and cross‑check supplier claims.

We emphasise provenance: when we present a supplier cost curve or a qualification probability in the full report, each datapoint is trace‑linked to source artifacts — lab reports, interview transcripts, customs records, or supplier technical sheets — allowing clients to replicate and stress‑test assumptions within their own diligence processes.

Implications for procurement, product and investor teams in 2026

Practical next steps for decision‑makers include:

-

Re‑baseline supplier risk models to incorporate elastomer price sensitivities and qualification lead times as first‑order variables.

-

Prioritise design‑win acceleration by investing in pre‑qualification test packages and localised inventory buffers for strategic product lines.

-

Integrate ESG metrics into supplier scorecards, particularly circularity metrics for recycled rubber and documented life‑cycle benefits for retail customers.

Each recommendation is paired in the full report with modelling templates that show the P&L and cash‑flow impacts of alternative sourcing choices and NPI timelines.

Closing and next step

2026 is a year for pragmatic investments — not speculative experimentation. The anti‑vibration mounts market presents steady top‑line expansion but a shifting profit landscape that rewards operational discipline, certification speed, and sustainability credentials. PW Consulting’s report translates this macro picture into tactical programs and valuation filters to guide capital deployment.

For full regional and application splits, detailed competitive scorecards, executable BOM models and the downloadable toolset, access the comprehensive study here: Worldwide Anti‑Vibration Mats Market Research .

For detailed analysis of this topic, please visit the official page: Anti-Vibration Mounts Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.