PW Consulting: Automotive Airbag Fabric Market to Reach USD 4.4 Billion by 2032

Automotive Airbag Fabric Market 2026: Strategic Imperatives from PW Consulting

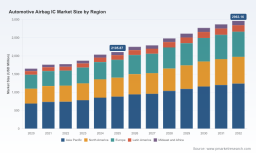

As of 2026, the global automotive airbag fabric market occupies a defined yet evolving niche within vehicle passive safety systems. PW Consulting’s latest market study synthesizes seven years of historical performance (2020–2025) and projects the market through 2032, identifying an overall expansion at a compound annual growth rate (CAGR) of 4.6%. Our base-year assessment (2025) places the market at USD 3.3 Billion and traces a path to approximately USD 4.4 Billion by 2032—figures that frame the investment, sourcing, and product-development questions OEMs, tier-1s, and component suppliers must resolve this year.

Automotive Airbag Fabric Market

Why 2026 Is a Decision Year

Multiple structural pressures converge in 2026 to create a narrow window for decisive capital allocation in airbag fabrics and associated IC ecosystems:

- Regulatory acceleration: New safety mandates and NCAP protocols demand broader airbag coverage and higher functional safety assurance.

- Supply-chain fragility: Continued lead-time volatility for mature-node MCUs and analog ICs raises the cost of inventory and program delay risk.

- Technology differentiation: Advances in integrated ICs and system packaging shift design-win criteria from point-products to platform-level interoperability.

These factors are compressing engineering cycles and shifting the center of gravity for value capture—companies that act in 2026 can lock-in scale advantages and compliance readiness; those that delay face higher remediation costs and longer qualification paths.

Market Trajectory—High-Level View (No Fragmented Numbers)

From 2020 through 2025 the sector showed resilience—with incremental recoveries following pandemic-era shocks—and in 2026 the market continues to expand under steady demand for OE retrofit and new-vehicle passive safety upgrades. Growth is driven by a combination of regulatory-driven scope expansion (more side and curtain coverage), more complex IC requirements (higher diagnostic coverage and ASIL-D compliance), and OEM platform refresh cycles that create waves of design activity rather than a single linear increase.

PW Consulting’s forecast to 2032 models the interplay of new-vehicle content growth, replacement cycles, and commodity-price normalization. The headline CAGR of 4.6% masks internal rebalancing: the market’s center of demand is shifting toward integrated system solutions and suppliers that can prove both functional safety and supply reliability. For complete regional and application distribution charts and interactive scenario outputs, refer to the full report.

Operational Playbook in the Report

Our study is built as an operator’s toolkit—designed to be actionable by CTOs, procurement chiefs, and corporate development teams charged with 2026 execution. The report does not only describe trends; it equips practitioners with constructs and models that directly close common gaps between strategy and production.

- Supply-chain map: Visualized node-by-node flows from textile mills to Tier‑1 assembly, exposing single-supplier dependencies and logistical bottlenecks that extend lead times.

- BOM decomposition logic: A repeatable framework to disaggregate system cost by materials, processing, IC content, and testing—enabling scenario-based cost-to-serve analyses without exposing proprietary supplier prices.

- Yield-adjustment models: Sensitivity modules that translate processing yield improvements and supplier quality interventions into bottom‑line reductions in unit cost and warranty exposure.

- Technology roadmap: A comparative timeline of material innovations, coating and seam technologies, and IC integration pathways aligned with likely regulatory milestones.

Collectively, these tools enable rapid prioritization of interventions—whether that is targeted qualification of a secondary supplier to reduce lead-time risk, a redesign to enable lower-cost assembly, or an investment case for integrated IC adoption to reduce ECU unit cost and diagnostic burden.

Competitive Landscape: What We See at the System Level

PW Consulting’s competitive analysis focuses on structural competitive dimensions rather than prescriptive forecasting of each vendor’s 2026 moves. Our assessment identifies the primary levers that drive design wins and defend market positions among semiconductor and systems players active in the airbag domain.

- Integrated platform depth: Companies offering multi-function ICs (squib drivers, power management, sensor interfaces, safety MCUs) compete on portfolio breadth and system-level interoperability. Bundling reduces integration cost and shortens validation cycles—key for OEMs managing program timing.

- Safety assurance and certification: Demonstrable ASIL-D processes and AEC‑Q100 Grade 1 qualification materially shorten OEM acceptance timelines. Certification investments act as a moat by raising the bar for new entrants and accelerating supplier lock-in.

- Manufacturing and supply reliability: Proven capacity for high-reliability production and the ability to meet long lead‑time contracts (including qualified second-source strategies) are increasingly decisive, given ongoing semiconductor lead‑time volatility.

- Systems and service ecosystem: Partnerships with Tier-1 integrators and the availability of engineering support for ECU BOM optimization are decisive in winning platform-level allocations.

For example, firms emphasizing integrated, safety‑certified IC platforms increase the odds of design wins where OEMs prize reduced validation cycles; conversely, suppliers with in‑house vertical manufacturing and mobility‑grade certification can convert certification investments into preferential sourcing agreements. PW Consulting’s profiles of leading participants map these dimensions and show where each firm’s competitive advantages are most likely to influence OEM procurement decisions.

Recent industry developments underscore these dynamics: in mid‑2025 an established MCU and power-IC supplier announced expanded automotive-grade modules targeted at entry through high-end airbag systems, while a major Tier‑1 gained enterprise‑level ASIL‑D certification for their entire semiconductor R&D process. These moves reduce friction in OEM qualification and raise the bar for newer entrants. For a deeper look at the competitive positioning and the design‑win criteria we track, access the full analysis here: Explore the full Automotive Airbag IC Market report .

Regulatory and Supply Dynamics—Implications for 2026 Capital Allocation

Three regulatory and supply-side realities shape rational capital allocation in 2026:

- Functional safety requirements (ISO 26262 ASIL‑D) and concurrent automotive electronics qualifications (AEC‑Q100 Grade 1) create multi-year certification lead-times that must be factored into platform roadmaps.

- Public safety standards and evolving NCAP criteria expand expected airbag coverage, increasing per-vehicle IC and textile content.

- Persistent supplier lead-time volatility for mature-node semiconductors raises the value of diversified qualification strategies and strategic buffer inventories.

Investment decisions made in 2026 therefore need to balance near-term program delivery against the longer horizon of compliance and platform consolidation. Firms that integrate certification timelines into their supply‑chain and product plans avoid last‑minute rework costs and maintain program cadence.

Practical Strategic Questions for 2026

- Where on my BOM should I prioritize qualification of a second source to minimize program delay risk?

- Does investing in integrated IC solutions reduce total cost of ownership when accounting for validation and software overhead?

- How do certification timelines for ASIL‑D and AEC‑Q100 alter our release schedules and capital expenditure plans?

- What is the appropriate inventory policy given supplier lead-time distributions and planned program launch dates?

Methodology—How PW Consulting Builds Confidence in This Analysis

Our conclusions are derived from a layered triangulation methodology combining primary and secondary sources to reduce estimation error and expose latent risks:

- Patent and standards citation analysis to trace technology diffusion and identify leading innovators.

- Structured interviews with OEM program managers, Tier‑1 technical leads, and semiconductor suppliers to validate timelines and qualification pain points.

- Physical teardown and laboratory testing of airbag modules to derive BOM structure and verify materials/processing claims.

- Proprietary BOM cost models and yield-adjustment modules calibrated against third‑party manufacturing data and supplier quotes to simulate margin sensitivity.

Where supplier confidentiality limits public disclosure, we use anonymized, aggregated datapoints and cross-validate findings against multiple independent sources—firm order books, certification registries, and in‑country testing facilities—to ensure that our scenario outputs reflect implementable realities rather than theoretical assumptions.

What PW Consulting Recommends in 2026

For executives and investors, the operational priority is twofold: secure compliance pathways and insulate program schedules from supplier volatility. Tactical moves include targeted dual‑sourcing for high‑risk ICs, accelerated certification roadmaps for platform ICs, and focused investments in integration capabilities that reduce ECU part count and software overhead. Our report provides the decision-support models to quantify these trade-offs for specific programs.

Next Steps

PW Consulting’s full Automotive Airbag Fabric Market report includes interactive regional and application distribution, supplier scorecards, and downloadable scenario models to support board-level capital allocation and program execution decisions. To view the complete dataset and executive dashboards, please visit: Download the full report .

For detailed analysis of this topic, please visit the official page: Automotive Airbag Fabric Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.