PW Consulting Predicts Parylene Market to Expand at a Robust 7.8% CAGR

Parylene Market 2026: Strategic Intelligence for Boardroom Capital Allocation

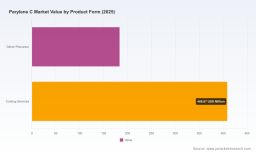

PW Consulting publishes a new market intelligence briefing on the Parylene coatings sector that is specifically engineered to inform 2026 capital-allocation and supplier-strategy decisions. The market is materially larger than it was at the start of the decade — rising from USD 839.4 million in 2020 to USD 1,222.0 million in 2025 — and our base-case projection points to continued expansion at a 7.8% CAGR through the 2026–2032 forecast window, reaching USD 2,067.3 million by 2032. This briefing is structured to give senior executives actionable strategic frameworks while deliberately preserving the detailed segmentation tables and transactional intelligence for report subscribers.

Parylene Market

Why 2026 Is an Inflection Point

Several converging forces make 2026 the year to re-set supplier strategy, capex plans, and compliance roadmaps for organizations that rely on Parylene coatings.

- Regulatory acceleration: Biocompatibility mandates and polymer safety reviews in multiple jurisdictions increase the bar for implantable and high-reliability applications, shifting procurement toward certified coatings with robust compliance documentation.

- Volume breakpoints in electronics and EV subsystems: Inline deposition technologies and faster cycle-times are unlocking new volume tiers that favour vertically integrated providers and OEMs that can absorb higher throughput.

- Supply-chain tightness for key raw inputs: Control of Parylene dimers and qualified CVD capacity is emerging as a critical constraint that affects lead times and total landed cost.

- ESG and end-of-life considerations: Disposal and polymer-management rules are creating upstream requirements for suppliers to certify waste-handling and provide lifecycle evidence.

What PW Consulting’s Report Delivers — Tools for 2026 Execution

The report is organized as a practical playbook rather than a theoretical abstract. Subscribers gain a suite of diagnostic tools designed for immediate operational use:

- Supply-chain map and supplier scorecards — traceability from dimer production to coated assemblies, with supplier risk tiers and qualification checklists that accelerate supplier selection without re-inventing the audit process.

- BOM teardown methodology — a replicable framework for estimating coating content and process steps by device class, enabling procurement to convert technical requirements into cost runways.

- Yield-adjustment models — scenario-driven models to quantify how deposition yield, rework rates, and throughput improvements affect landed unit cost and margin at scale.

- Technology roadmap and equipment economics — side-by-side comparisons of batch vs inline CVD architectures, total cost of ownership drivers, and throughput break-evens that inform capex vs outsourcing choices.

- Compliance matrix — mapping of IPC, ISO, USP and regional medical-device regulations to supplier evidence packages and audit checklists to reduce time-to-market for regulated devices.

Each tool is designed to solve a 2026 pain point — from reducing total cost of ownership in high-volume electronics to shortening supplier qualification cycles for medical devices — without publishing the confidential parameter values that are included in the full report.

Market Dynamics and Macro View

PW Consulting’s historical calibration shows steady expansion across 2020–2025, with market size moving from USD 839.4 million to USD 1,222.0 million. Looking forward from the 2026 vantage the market trajectory continues on an upward path at a 7.8% CAGR to USD 2,067.3 million by 2032. Market concentration is notable: the top three suppliers account for roughly 65.0% of the market, and the top five for about 75.0%, underscoring a market where scale, certifications, and integrated supply capabilities confer structural advantages.

Key demand vectors include electronics miniaturization, medical implant compliance, EV and automotive electronics reliability, and defense/aerospace qualification cycles. On the supply side, dimer manufacture, equipment lead times and certification bottlenecks determine who can scale first when a large design win materializes.

Competitive Dimensions — What Separates Winners from Followers

PW Consulting’s competitive analysis focuses on dimensions that determine durable advantage rather than speculative year-by-year forecasts. The following competitive vectors consistently dictate design wins and margin capture in 2026:

- Vertical integration and raw-material control: Owning or tightly contracted access to Parylene dimer production reduces exposure to input shortages and price spikes.

- Equipment and process IP: Providers that develop proprietary deposition systems or inline solutions are able to compress cycle times and offer differentiated unit economics to high-volume OEMs.

- Certification and quality systems: ISO 10993, USP/IPC compliance, AS9100 and ISO 13485 are gating factors for medical, aerospace and defense segments; possession of these certifications materially shortens customer qualification windows.

- Regional capacity and speed-to-line: Proximity to major electronics hubs and EV supply chains, combined with flexible CVD chamber capacity, shortens time-to-market for new projects.

- Integration with adjacent technologies: Bundles that combine Parylene deposition with plasma treatments, potting or conformal design services reduce assembly complexity for customers.

Examples from the field (non-exhaustive): a global coatings OEM that owns dimer production and sells deposition equipment can convert an equipment sale into recurring dimer and service revenue; a medical-focused coater that holds ISO 13485 capacity expansion is positioned to capture higher-margin implant work; an equipment OEM pursuing CE certification addresses customer hesitancy around medical-class installations. Recent market developments illustrate these vectors in action:

- 2026-03: Penta Nanotechnology pursues CE certification for its vacuum CVD systems, signalling OEM efforts to bridge equipment acceptance in regulated markets.

- 2026-02: VSi Parylene expands ISO 13485-certified deposition capacity to serve medical device manufacturers, demonstrating a capacity-led bid to win device qualifications.

- 2026-02: Specialty Coating Systems launches next-generation inline deposition equipment that reduces batch cycle times for high-volume applications.

- 2025-07: A major Asia-based coater built a new multi-chamber facility targeting consumer and EV electronics, reflecting localization of capacity to meet regional demand.

- 2025-04: A North American coater obtained AS9100 Rev D certification for aerospace work, highlighting certification as a competitive threshold.

To review company profiles, comparative capabilities and our full competitive heat map, see the detailed section in our report. For immediate access, click here: Worldwide Parylene C Market Research .

Strategic Implications for Boardrooms and CROs

Executives who treat 2026 as a year of active repositioning can reduce risk and capture upside by executing a small set of high-impact moves:

- Secure raw-material pathways: Prioritise agreements or secondary sources for dimer supply to de-risk production ramp-ups.

- Validate supplier certification roadmaps: Insist on audit-ready documentation for IPC, ISO and biocompatibility evidence when qualifying new coaters for regulated programmes.

- Model capex vs outsourcing around throughput break-evens: Use technology-roadmap analysis to determine whether inline deposition or external coaters yield lower total cost of ownership at intended volumes.

- Factor ESG and disposal into vendor selection: Require supplier commitments on end-of-life handling and waste-stream certification to avoid regulatory friction.

- Pursue modular contracting and pilot design wins: Structure PO terms to include pilot phases and yield gates that align incentives with supplier performance improvements.

Methodology — Why Our Findings Are Actionable

PW Consulting’s conclusions rest on a Layered Triangulation methodology designed to minimize single-source bias and surface confidential operational signals that matter to executives. Core components include:

- Primary data collection: Over 80 structured interviews with coating-house operations managers, OEM supply-chain leads, and equipment OEM engineers, many conducted under NDA to capture non-public lead-time and yield data.

- BOM teardown and lab verification: Controlled dissections of representative assemblies combined with laboratory deposit thickness measurement to validate coating consumption models.

- Patent and equipment shipment analysis: Cross-referencing patent filings with equipment placement records and import/export customs data to infer adoption rates for new deposition platforms.

- Proprietary modelling: Supply-risk scoring, yield-adjustment Monte Carlo routines and certified compliance-matrix mapping that are back-tested against known design-wins.

This multi-source approach allows PW Consulting to publish robust directional insights and operationally relevant frameworks while preserving the transactional tables, supplier-level metrics and unit-cost outputs that we reserve for report clients.

How to Access the Full Intelligence

Our public note is intended to establish the strategic context for 2026 decisions. The full PW Consulting Parylene Market research package contains the complete regional and application splits, supplier-level scorecards, BOM templates and executable playbooks referenced above. For the full dataset and step-by-step supplier selection tools, visit: Worldwide Parylene C Market Research .

PW Consulting remains available to support board-level scenario workshops, supplier negotiation playbooks and facility-level implementation planning for organizations that require rapid execution in 2026. The underlying market momentum and concentration dynamics create both risk and opportunity — those with the most structurally defensible supply chains and the fastest certification pathways will capture the disproportionate share of growth over the coming planning cycle.

For detailed analysis of this topic, please visit the official page: Parylene Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.