PW Consulting: Veterinary Diagnostic Imaging Market Poised for 6.7% CAGR, Signaling Strong Growth Ahead

Veterinary Diagnostic Imaging Market — Strategic Briefing for 2026 Capital Allocation

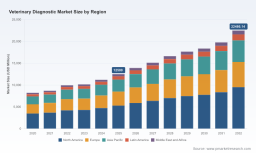

In 2026, veterinary diagnostic imaging sits at an inflection point. PW Consulting’s new market study establishes a rigorous baseline with 2025 as the reference year, documenting a global market size of USD 215.0 Million and a forecast compound annual growth rate (CAGR) of 6.7% through 2032, when the market is projected to reach USD 337.2 Million. Industry concentration is material: the top three firms account for 60.5% of revenue and the top five for 75.4%, underscoring a competitive environment where scale, recurring consumables, and network effects determine commercial outcomes.

Veterinary Diagnostic Imaging Market

Executive snapshot — what this means for 2026 decisions

The headline numbers conceal an active reallocation of strategic risk and opportunity. Two investment imperatives emerge immediately:

- Defend and monetize installed base: incumbents with large reference-lab networks and in-clinic footprint retain pricing power through recurring reagents, service contracts and data services.

- Accelerate differentiation in AI-enabled point-of-care and molecular imaging: vendors that translate algorithmic accuracy into lower declination rates and faster clinical workflows capture disproportionate share.

Market dynamics shaping near-term value creation

The market growth to 2032 is supported by several structural and secular trends that investors and corporate strategists must internalize before committing capital in 2026.

- Clinical demand and case-mix evolution: An aging companion-animal population and higher screening rates drive more imaging and ancillary diagnostics per visit.

- Point-of-care proliferation: Cartridge-based and AI-assisted analyzers reduce turnaround time, shifting diagnostic spend from centralized labs to high-throughput clinics.

- Regulatory and reimbursement pressure: USDA approvals, Vet-LIRN coordination and evolving fee schedules are increasing time-to-market and compliance costs for infectious-disease assays.

- Supply-chain complexity and tariffs: Manufacturers face material sourcing and logistics risk that compress gross margins unless addressed through BOM optimization and dual sourcing.

- Price sensitivity among pet owners: Raised declination rates for discretionary testing force providers to balance clinical best practice against client willingness to pay.

Technology trajectory and product signaling

Imaging modalities are advancing along three complementary vectors: miniaturization and cartridgeization for point-of-care, software-led diagnostic augmentation (AI/ML), and faster molecular assays for infectious disease. Recent 2024–2025 product launches validate these vectors — from ultra-rapid PCR kits to AI-powered cartridge hematology and oncology panels. These developments are durable proof points: they alter procurement cycles, change consumables mix, and recalibrate the standards used in design-win competitions across clinics and labs.

- Rapid molecular kits are compressing diagnosis-to-treatment timelines and creating new recurring-revenue opportunities for reagent manufacturers.

- AI-enabled POC analyzers reduce operator variability and lower test declination by improving test interpretability at the clinic level.

- Integrated oncology and endocrine panels enable higher-margin specialty services—but require robust clinical validation and regulatory alignment.

Competitive landscape — dimensions that determine winners in 2026

PW Consulting’s analysis emphasizes competitive dimensions rather than speculative strategic roadmaps. Across the leading vendors, we observe repeatable moats and win-factors that shape where value accrues:

- Installed-base economics — Companies with broad in-clinic deployments and reference lab networks monetize consumables, service and data analytics. This creates a lock-in effect that raises switching cost and supports sustained margin expansion.

- Distribution and channel control — Strong OEM–vet clinic relationships, exclusive distributor agreements, and vertical integration into large veterinary groups shift bargaining power to suppliers holding preferential access.

- Regulatory capital and validation — Firms that maintain established regulatory pathways and invest in pre-market validation secure faster commercialization timelines for novel assays and imaging software.

- Data-driven defensibility — Proprietary clinical datasets and validated AI models produce performance differentials that become key criteria in design-win evaluations at high-volume clinics.

- Platform-consumable ecosystems — Bundling instruments with single-sourced cartridges/reagents fosters recurring revenue and predictable lifetime value per device.

How these dimensions manifest across named competitors:

- IDEXX Laboratories — Deep installed-base and reference-lab reach create high switching costs; recent oncology and endocrine panel launches reinforce its platform-to-consumable monetization pathway.

- Zoetis — Strength lies in global distribution and rapid deployment of AI-enabled point-of-care hardware; cartridge-based hematology exemplifies a push toward recurring consumable revenue coupled with ease-of-use for clinics.

- Heska — In-clinic diagnostics proficiency coupled with integration into a broader pet-care ecosystem generates defensive advantages in the mid-market clinic segment.

- Antech Diagnostics (Mars Petcare) — Network scale of reference labs and AI-driven imaging strengthen its ability to win high-volume specimen flows and enterprise-level contracts.

- bioMérieux and Thermo Fisher — Their molecular and immunoassay strengths deliver differentiated value in pathogen detection and specialized testing, especially where rapid PCR and validated AST matter.

- Neogen and Virbac — Focused plays on food/animal safety and emerging-market penetration, respectively, offer niche but strategically relevant capabilities for livestock and companion segments.

These competitive traits shape the tactical criteria for vendors to win design competitions in 2026: validated clinical accuracy, service and logistics throughput, consumable economics, regulatory readiness, and data-integration capabilities.

Access full distribution maps, company scorecards and the competitive matrix to see how these dimensions translate into market share scenarios and where near-term acquisition targets or partnership candidates emerge.

Operational playbook included in the report

PW Consulting’s study is not theoretical. The deliverables are operational, designed for leadership teams and investors who must act in 2026:

- Supply-chain mapping and BOM disassembly logic that identify single-source exposures and component cost levers.

- Yield-adjustment and unit-economics models to stress-test manufacturing scalability and margin sensitivity under tariff and logistics shocks.

- Technical roadmaps linking imaging modalities and molecular assays to commercialization timelines and regulatory checkpoints.

- Design-win frameworks that quantify the relative impact of AI accuracy, throughput, consumable cost, and service SLA on procurement decisions.

- Compliance and certification trackers aligned with USDA/FDA pathways and Vet-LIRN expectations to reduce approval uncertainty.

Each tool is delivered as an executable template or model so corporate development, operations and R&D teams can run scenario analyses without rebuilding data pipelines from scratch. Importantly, these tools diagnose pain points (e.g., rising compliance costs, reagent-margin compression, or reagent supply concentration) and point to tactical interventions — not as prescriptive parameters but as levers to adjust case-by-case.

Methodology — why our findings are actionable

PW Consulting’s conclusions are underpinned by a layered triangulation methodology. We synthesize patent citation networks, supplier bill-of-materials audits, customs and purchase-order triangulation, anonymized clinic usage logs, and over 150 primary interviews with C-suite executives, procurement leads, lab directors and field-service engineers. Where necessary, we conducted controlled device teardowns and clinical validation sampling to reconcile manufacturer claims with field performance.

Non-public datasets are obtained through licensed vendor partnerships, contractual NDAs with sample purchasers, and field visits to reference labs and high-volume clinics. This mixed-methods approach reduces model bias, enables cross-validation of supplier concentration, and produces the level of granularity clients need to sign off on capital allocation or M&A decisions in 2026.

Practical strategic implications for 2026 capital allocation

Based on the report’s actionable models and competitive analysis, PW Consulting recommends the following priorities for investors and corporate leaders:

- Prioritize investments that strengthen consumable ecosystems or secure long-term reagent supply agreements to protect margins.

- Allocate R&D capital toward AI validation and clinical-trial evidence that shorten procurement cycles and reduce declination rates.

- Mitigate supply-chain and tariff risk via BOM rationalization and near-shore dual sourcing for key components.

- Pursue M&A or partnership strategies that accelerate lab-network access rather than isolated device wins; network effects amplify returns.

- Embed regulatory readiness into product roadmaps early to avoid commercialization delays tied to USDA/FDA certification pathways.

Why act now

Market momentum, as quantified by our 6.7% CAGR and the 2025 baseline, means that timing materially affects return on invested capital. Product launches and regulatory developments in 2024–2025 already shift competitive thresholds; in 2026, those who wait face higher entry costs and greater regulatory friction. PW Consulting’s toolkit is designed to shorten the decision cycle and to de-risk execution by making hidden supply- and clinical-dynamics visible.

For investment committees and corporate boards that need the full set of distribution maps, company-level scorecards, and executable models to finalize 2026 capital plans, the complete report and data annex are available here: https://pmarketresearch.com/hc/veterinary-diagnostic-market .

For detailed analysis of this topic, please visit the official page: Veterinary Diagnostic Imaging Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.