PW Consulting: Climate Test Chamber Market Poised for 9.2% CAGR, Accelerating Demand in Automotive and Electronics Testing

Climate Test Chamber Market — Strategic Briefing for 2026 Decision-Makers

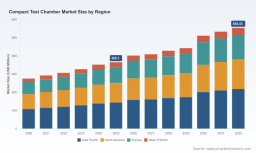

PW Consulting publishes a focused industry briefing derived from our new Climate Test Chamber Market research, designed to equip procurement, R&D and corporate development teams with the situational awareness they need in 2026. The compact environmental chamber market is at an inflection point: after sustained recovery through 2020–2025, the industry is entering a higher-growth phase underpinned by regulatory change, supply-chain stress, and technology-driven demand from electrification and electronics miniaturization. Our analysis shows the global compact test chamber market reached USD 612.4 Million in 2025 and is projected to grow to USD 1,132.3 Million by 2032, reflecting a 9.2% CAGR in the 2026–2032 forecast window. This briefing explains why that trajectory matters for capital allocation, procurement strategy and product roadmaps in 2026 — and what tools in the report accelerate better decisions.

Climate Test Chamber Market

Market Snapshot (2026 lens)

The market in 2026 is simultaneously larger and more dynamic than many OEMs appreciate. Key qualities that define the current window are:

- Acceleration in demand from high-reliability sectors (electronics, automotive electrification, aerospace) coexisting with rising demand for laboratory-grade solutions driven by regulated industries (pharma, materials testing).

- Regulatory and ESG drivers: low-GWP refrigerant rules and energy-efficiency mandates are forcing design and procurement trade-offs that directly affect total cost of ownership.

- Supply-chain volatility: raw-material and component price pressure is persistent, and the refrigeration supply chain (compressors, heat exchangers, refrigerants) is a particular pinch-point.

For companies allocating capital in 2026, these forces mean that budget timing, supplier selection and technical specifications cannot be decoupled from regulatory and materials risk assumptions. The report provides the modelling layers executives need to stress-test those assumptions — without exposing the proprietary micro-segmentation here.

Why This Report Matters for 2026 Decisions

Executives are making three types of decisions in 2026 where better market intelligence delivers immediate value: procurement and supplier risk mitigation; product and R&D roadmap prioritization; and aftermarket and service-business design. Our research translates market momentum and constraints into decision-ready inputs across these three domains.

Immediate strategic implications

- Cost control: rising steel and commodity volatility is changing BOM composition and procurement cadence. The report’s supplier cost-mapping helps teams set hedging thresholds and negotiate indexed contracts.

- Compliance-first product design: new refrigerant constraints and energy-efficiency requirements make “spec-to-reg” alignment a gating factor for design wins in regulated markets.

- Service economics: as clients demand lower lifecycle costs, aftermarket and calibration services become a primary defensibility lever for manufacturers and value capture for distributors.

Practical Tools Inside the Report

The PW Consulting report is structured to move leaders from awareness to action. Key operational tools included are:

- Supply-Chain Topology Map — a visual and analytic map of critical upstream nodes (compressors, refrigerant sources, sheet metal fabrication, electronics controllers) and their failure modes under 2026 market stress.

- BOM Decomposition Logic — a repeatable teardown methodology that isolates cost drivers at component and subassembly levels, enabling rapid scenario-based TCO comparisons without exposing confidential line-item pricing in this briefing.

- Yield Adjustment & Pricing Models — calibrated yield curves and margin levers that show how factory yield improvements or sourcing shifts affect unit economics across common product architectures.

- Technology Roadmap & Compliance Matrix — an indexed view of low-GWP refrigerant adoption paths, energy-efficiency design options, and certification dependencies that impact time-to-market for new models.

Each tool is operationalized with templates and checklists so procurement, engineering and finance teams can run 12–24 month “what-if” scenarios relevant to 2026 capital cycles. For readers seeking implementation-ready assets, download the full toolkit in the comprehensive report: Download the full report .

Competitive Dynamics — What Buyers and Investors Need to Know

The compact test chamber market in 2026 is moderately consolidated, with a small number of global vendors maintaining a majority share while a tier of regional and specialist players competes on price, customization and local service. Our concentration analysis indicates that market concentration is meaningful, enabling incumbents to leverage scale in components and after-sales networks.

Dimensions that determine winners in 2026

- Product engineering and thermal-control IP — vendors with proven low-emission refrigeration cycles and modular architectures secure faster acceptance in regulated markets.

- Service and calibration networks — durability of field support and rapid calibration capability are decisive in buyer selection, especially for high-reliability customers.

- Design-win capture through co-development — early technical collaboration with OEMs (battery packs, avionics, semiconductor test labs) accelerates specification lock-in.

- Cost-to-serve and localized manufacturing — regional manufacturing and component sourcing reduce lead-times and exposure to shipping and tariff risk.

How leading vendors position along these dimensions

Our sector workbench considered the competitive profiles of established OEMs and emerging suppliers. Examples of the competitive dimensions we observe:

- Thermotron Industries — established credibility in high-performance environmental simulation and multi-physics systems; competitive moat built on engineering depth and end-market trust for complex vibration + thermal integrations.

- Cincinnati Sub-Zero (CSZ) and ESPEC — reputation for compact, reliable chambers used in manufacturing and R&D workflows; they compete on precision and service reliability.

- Weiss Technik and Memmert — strong emphasis on precision and sustainability, with early adoption of low-GWP solutions and compliance-oriented product lines that appeal to regulated industrial buyers.

- AES and Angelantoni — niche differentiation through patented battery testing solutions and aerospace-grade systems respectively, enabling premium pricing in specialized segments.

- China-based suppliers (LIB Industry, Sanwood) and mid-tier vendors (Russells) — compete on cost and lead times, and are increasingly relevant for large volume lab procurement where total cost is prioritized over bespoke engineering.

This analysis focuses on the competitive vectors (moats, design-win drivers, service footprints) that procurement teams must evaluate in 2026 rather than publishing private strategic forecasts for individual vendors. For buyers weighing RFP responses, our vendor scorecards in the full report convert these qualitative dimensions into quantitative supplier-selection matrices.

Methodology — Why our findings are decision-grade

PW Consulting’s conclusions are derived through a layered triangulation methodology that combines three rigor pillars: structured primary research, empirical teardown analysis, and multi-source market calibration. Our primary research includes confidential interviews with OEM procurement leads, tier‑1 supplier executives and service partners; field visits to production lines and test labs; and signed supplier NDAs that permit validation of cost and lead-time inputs.

Empirical inputs include BOM tear-downs of representative compact chamber models, patent and standards citation analysis to identify technology adoption trajectories, and time-series price tracking for key commodities. We then triangulate these inputs against proprietary shipment and shipment-intent panels, public financial disclosures, and regulatory filing data to produce models that are both robust and scenario-ready for 2026 decision-making.

2026 Playbook — Actions for Executives

Three priority actions for 2026 based on our findings:

- Lock-in component supply with dual-source clauses for compressors and low-GWP refrigerants; where possible, price-index or volume-commitment clauses mitigate short-term commodity swings.

- Refocus product specs on lifecycle energy cost and compliance. Re-specification now avoids costly redesigns when new regional refrigerant restrictions or energy-efficiency standards are enforced.

- Monetize service: redesign commercial offers to bundle calibration and predictive maintenance — service revenue reduces sensitivity to upfront hardware commoditization.

These tactical moves are supported by the report’s executable templates: supplier scorecards, contract negotiation checklists, and TCO comparators calibrated to 2026 market reality. For teams evaluating acquisition or expansion, our M&A checklist maps regulatory and supply risks into valuation adjustments used by strategic and private equity buyers.

Final Note and Next Steps

2026 is a decisive year for firms engaged in environmental testing equipment: regulatory shifts, persistent commodity volatility, and faster adoption cycles for electrification and miniaturized electronics mean that delayed decisions carry measurable cost and market-share consequences. PW Consulting’s Climate Test Chamber Market report gives leaders the analytic scaffolding to make these choices with confidence — while preserving the deeper granular datasets and supplier-level analytics for report subscribers. To access the full dataset, vendor scorecards and operational toolkits, please follow this link: Access the full report and toolkit .

For detailed analysis of this topic, please visit the official page: Climate Test Chamber Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.