PW Consulting Forecasts AC Power Source Market to Expand at a 4.3% CAGR in 2026–2032, Underscoring Resilient Demand

AC Power Source Market 2026: Strategic Imperatives for Capital Allocation

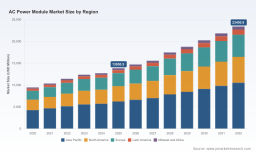

In 2026, the AC power source market is not just growing — it is reconfiguring. PW Consulting’s latest AC Power Source Market research frames that reconfiguration with quantified scale and a practical playbook for executives who must allocate capital, manage compliance risk, and secure design wins under rising input-cost pressure. Our core finding: the market advances from USD 125.2 Million in 2025 toward an expected USD 168.3 Million by 2032, driven by a 4.3% compound annual growth rate across the 2026–2032 forecast window. These headline metrics establish the perimeter of opportunity; the report behind this release provides the distributional maps and segment-level detail necessary to convert intent into advantage.

AC Power Source Market

Why 2026 is a Decision Point

Several concurrent forces make 2026 a critical year for strategic action rather than passive monitoring:

-

Input-cost inflation: Copper and laminate cost spikes, together with semiconductor price uplifts (MOSFETs and related power devices up 10–20% in early 2026), are compressing BOM margins across the value chain and accelerating cost-optimization programs in OEMs and contract manufacturers.

-

Regulatory tightening: New building and energy-efficiency mandates — such as California’s 2025 Title 24 measures now in effect — are reshaping product specifications for building systems and heat-pump electrification, with ripple effects for product certification and type-testing timelines.

-

Standards horizon: Emerging efficiency and motor standards (e.g., expanded electric motor requirements announced by the U.S. Department of Energy) are creating medium-term compliance cliffs that influence platform selection and qualification roadmaps.

-

Fragmented supplier landscape: Market concentration remains low (CR3: 18.5%, CR5: 23.7%), so suppliers compete on differentiated engineering, reliability, and channel penetration rather than on price alone — a structural reality that changes how procurement should evaluate strategic partnerships.

Market Trajectory and What It Means for Capital Allocation

The macro trajectory — from roughly USD 103.9 Million in 2020 to USD 125.2 Million in 2025, and the forecast horizon toward USD 168.3 Million by 2032 — is steady but non-linear. That steadiness masks important inflection points: mid-range power modules are benefitting from electrification of buildings and telecom edge infrastructure, while high-density modular front-ends are growing in demand for data-center and industrial applications.

For CFOs and corporate strategists, the implication is two-fold:

-

Near-term capital should prioritize resilience: dual-sourcing for key passive and semiconductor inputs, targeted investments in yield-improvement tooling, and contractual clauses that hedge commodity pass-throughs.

-

Medium-term capital must prioritize platform optionality: investments in modular front-end architectures and configurable power bricks that reduce qualification cycles across adjacent end-markets will compound return on qualification spend.

Practical Intelligence: What PW Consulting’s Toolbox Delivers

Our report is built to be operational. It goes beyond market sizing and SWOT to deliver instruments that procurement, product, and operations leaders can actually use in 2026:

-

Supply-chain maps that identify single points of failure across Tier-1 to Tier-3 suppliers, annotated with lead-time elasticity and substitute-material readiness.

-

BOM decomposition logic that isolates high-sensitivity line items (by cost, lead time, and regulatory exposure) and quantifies the impact of supplier price moves on finished-goods margins under multiple sourcing scenarios.

-

Yield-adjustment and sensitivity models that translate process improvement initiatives into NOI impact under realistic ramp assumptions — enabling capital prioritization between CAPEX (automation, test) and OPEX (material hedging, buffer stock).

-

Technology roadmaps that link component-level innovation (GaN adoption, high-frequency magnetics, advanced PFC topologies) to system-level trade-offs in thermal footprint, EMC, and serviceability.

Each tool is accompanied by an implementation playbook. The report intentionally avoids handing out prescriptive parameter sets in this public summary — instead, we show how to apply the models to your own BOM and validate outcomes using layered triangulation techniques described below.

Competitive Dynamics: Where Design Wins Really Come From

The supplier list in this market includes global modular specialists, established OEMs with vertical integration, and regional manufacturers optimizing cost structures. From Cincon and MEAN WELL to XP Power, TDK-Lambda, Vicor, COSEL and Phoenix Contact, competition is multifaceted. PW Consulting’s analysis highlights the dimensions that determine 2026 design wins and supplier survival:

-

Technical moat: Proprietary thermal designs, in-house magnetics/ferrites, or packaging IP that shortens certification risk or reduces BOM complexity.

-

Integration capability: Ability to deliver configurable front-ends and seamless mechanical/electrical interfaces that shorten OEM validation cycles.

-

Channel and service: Global spares networks and local engineering support, especially for regulated sectors (medical, aerospace), that contribute to repeat business and aftermarket revenue.

-

Cost and scale agility: Manufacturing footprint choices (near-shore vs. low-cost regions) and contract design that absorb or pass through commodity shocks without losing competitiveness.

These dimensions are what underpin the competitive moats we evaluate — not simplistic revenue comparisons. Executives reading the full report will find our confidential scoring matrices and supplier-specific risk markers that indicate where partnerships are worth doubling down on and where requalification should be accelerated.

Technology Pathways and Strategic Priorities

Technology choices in 2026 are less about chasing the latest component and more about aligning system-level trade-offs with compliance, serviceability, and cost. Our mapping shows three convergent pathways:

-

Efficiency-first modules targeting aggressive regulatory scopes; suitable where operating-costs and regulatory penalties dominate lifecycle TCO.

-

Modular, high-density front-ends for space-constrained industrial and data-center applications where configurability reduces qualification duplication.

-

Low-cost, high-volume solutions optimized for consumer and certain automotive segments where BOM resilience and supplier diversification are the paramount concerns.

Choosing among these pathways requires answering operational questions about qualification cadence, service-level agreements, and capital intensity — the report contains scenario-driven decision trees to assist that selection process. To review the full technology mapping and supplier matchup matrices, access the full study here: https://pmarketresearch.com/worldwide-ac-power-module-market-research .

Methodology: Why Our Findings Are Actionable

PW Consulting’s conclusions are grounded in multi-source, proprietary intelligence designed to minimize blind spots:

-

Layered Triangulation: We reconcile primary interviews (OEMs, EMS providers, component suppliers), teardown BOMs from confidential samples, and customs/production datasets to cross-validate unit economics and supply constraints.

-

Patent and standards mapping: We analyze patent families, component approvals, and certification timelines to estimate time-to-market and the persistence of technical differentiation.

Where public data ends, our team supplements with controlled-access supplier disclosures and lab-verified component measurements under non-disclosure agreements. This allows us to construct validated BOM sensitivity scenarios and supplier risk profiles without exposing client or supplier confidentials in the public report.

Actionable Recommendations for 2026

Executives should treat 2026 as a period for decisive repositioning across three fronts:

-

Supply resilience: Recast supplier scorecards to include raw-material exposure and delivery elasticity; negotiate trigger-based pricing clauses tied to copper and semiconductor indices.

-

Qualification leverage: Invest selectively in modular platforms that amortize qualification across multiple product families to reduce per-product certification cost and calendar risk.

-

Strategic sourcing: Identify a small set of dual-sourced components where near-term hedging or vendor-financed tooling can materially reduce program risk.

Each recommendation is mapped in the full report to specific P&L and balance-sheet impacts using the yield and BOM models described earlier.

Closing: Where to Go From Here

The AC power source market in 2026 presents stable headline growth but critical tactical and strategic forks beneath the surface. Commodity volatility, regulatory timelines, and the fragmented supplier landscape create both risk and arbitrage for disciplined firms. PW Consulting’s report synthesizes the market trajectory, provides the operational models required to make confident capital decisions, and scores suppliers on the competitive dimensions that determine who will capture long-term share.

For procurement leaders, R&D heads, and corporate strategists ready to translate insight into action, the full report — including complete segment distributions, supplier scorecards, and downloadable models — is available here: https://pmarketresearch.com/worldwide-ac-power-module-market-research .

For detailed analysis of this topic, please visit the official page: AC Power Source Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.