PW Consulting: Automotive Clutch Market to Rise from USD 13.5 Billion in 2025 to USD 19.1 Billion by 2032 at a 4.8% CAGR

Automotive Clutch Market — Strategic Briefing for 2026 Decisions

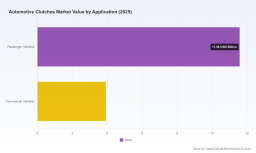

PW Consulting releases a targeted industry briefing derived from our full Automotive Clutch Market study to support executive capital-allocation and product-strategy decisions in 2026. The global clutch market demonstrates steady expansion: total industry value rises from USD 10.3 Billion in 2020 to USD 13.5 Billion in 2025, and our model forecasts growth to USD 19.1 Billion by 2032 at a 4.8% CAGR. Market concentration is meaningful (CR3 65.0%; CR5 75.0%), which shapes supplier negotiating power and OEM sourcing strategies.

Automotive Clutch Market

Why this briefing matters now

Companies planning investments, M&A, or procurement pivots in 2026 face an environment where regulatory pressure, material-cost volatility, and technology bifurcation create asymmetric risks and opportunities. The report translates macro momentum into operational priorities for the coming 12–24 months and explains where time-sensitive moves deliver the highest ROI.

-

Regulatory urgency — Emissions and fuel-efficiency standards are materially increasing the addressable demand for advanced clutch systems in hybrid powertrains.

-

Cost pressure — Raw-material dynamics (notably rising steel and aluminum costs and tariff-induced price shocks) escalate supplier input-cost volatility across manufacturing footprints.

-

Consolidation dynamics — A concentrated supplier base amplifies the impact of a single supplier’s capacity or technology decisions on OEM production continuity.

-

Technology divergence — Parallel adoption paths (conventional friction systems, dual-clutch modules, and electro-mechanical e-clutches) require distinct go-to-market plans and BOM strategies.

Actionable components inside the full report

Where many market studies stop at high-level sizing, our deliverable is constructed as a practical playbook for 2026 execution. Key decision-support assets include:

-

Supply-chain maps that trace tiered suppliers, strategic sole-source nodes, and embedded risk concentrations — designed for rapid scenario-testing under supply disruption assumptions.

-

BOM decomposition logic that links material, process and assembly cost drivers to margin levers; the framework is usable to run sensitivity analyses without exposing proprietary cost cells publicly.

-

Yield-adjustment and throughput models calibrated to real-world shop-floor yield distributions and defect-type frequencies to inform CAPEX vs. process-improvement choices.

-

Technology roadmaps aligning component-level innovation (e.g., wet vs. dry systems, hybrid clutch modules, friction material R&D) with OEM electrification timetables.

-

Compliance and sourcing playbooks for global trade scenarios — intended to operationalize tariff mitigation, localized sourcing, and compliance checks for Tier-1/Tier-2 suppliers.

How these tools address 2026 pain points

Executives tell us the two most urgent 2026 problems are (1) protecting margins under rising input costs and (2) retaining design-wins as OEMs push electrification. Our toolset converts observed market signals into executable choices:

-

Cost control: BOM logic combined with yield models highlights near-term levers (material substitution, process yield gains, localized sourcing) and quantifies trade-offs between CAPEX and recurring savings.

-

Design-win defense: The technology roadmap and competitive-dimension analysis reveal where integration with transmission systems, performance validation artifacts, and reliability demonstration become non-negotiable for OEM platforms.

-

Compliance readiness: Scenario playbooks map how regulatory tightening translates into component-spec changes and supplier qualification timelines so procurement teams can pre-empt schedule exposure.

Competitive dimensions — what differentiates winners in 2026

Our analysis of incumbent players focuses on strategic dimensions rather than publishing proprietary forecasts. Across the industry, successful suppliers exhibit distinct moats and reproducible design-win playbooks:

-

Integration advantage — Firms with tight vertical integration into transmission assemblies or proven e-clutch modules lower OEM integration costs and shorten qualification cycles.

-

Material and IP moats — Advanced friction formulations and patented dual-clutch architectures create migration barriers that matter when OEMs consolidate suppliers.

-

Scale and local footprint — Manufacturing scale plus regional capacity close to key OEM clusters reduces lead times and mitigates tariff and logistics risks.

-

Service and aftermarket channels — Complementary aftermarket reach extends lifecycle revenue and creates data feedback loops for product improvement.

-

Design-win mechanics — Winning new OEM programs in 2026 increasingly depends on rapid prototype cycles, demonstrable NVH (noise-vibration-harshness) performance, and co-engineered integration into hybrid architectures.

Selected industry movements in 2024–2025 that reshape these dimensions include product launches and commercial agreements that expand regional portfolios, and merger activity that recomposes capabilities and IP pools. For example, recent public developments include Eaton’s mid-2025 truck clutch launch in Asia and South America, BorgWarner’s mid-2025 DCT contract expansions, and Schaeffler’s merger activity affecting e-clutch portfolios in late 2024. These events are signals of how scale, geography and product breadth are being deployed as competitive levers in 2026.

For readers ready to evaluate competitor positioning in actionable detail, consult the company-by-company capability matrices and our recommended response options in the full report (Download the full Automotive Clutch Market report: https://pmarketresearch.com/auto/automotive-clutches-market ).

Technology pathways and where to place your bets

Multiple viable technology tracks coexist in 2026. Choosing the right pathway is a function of customer mix, production scale, and regulatory timelines. Key considerations we model include:

-

Electrified propulsion compatibility — e-clutches and hybrid modules require different validation scopes, software integration, and thermal-management strategies than legacy friction parts.

-

Wet vs. dry architectures — Trade-offs between efficiency, cooling, and packaging determine suitability across vehicle segments and regional vehicle cycles.

-

Materials innovation — Advances in friction materials and lightweight substrates can drive lifecycle cost improvements, but they change supplier qualification timelines and material risk profiles.

-

Manufacturing digitization — AI-driven process control and inline quality analytics materially shorten ramp times and reduce recall risk for high-mix lines.

These pathways require bespoke investment timing. The full report contains decision trees that map OEM platform timing to supplier investment triggers and break-even horizons.

Supply-chain stressors and mitigation levers

Recent commodity signals are already affecting supplier margins and sourcing choices. Notable industry inputs in 2025–2026 include upward HRC steel price trends observed from mid-2025 into early 2026 and tariff-driven aluminum and steel cost pressure. Such shifts force suppliers to reassess supplier contracts, hedging strategies, and footprint rationalization. Our analysis shows that procurement teams benefit from rapid scenario modeling that pairs material-hedging options with near-term capacity actions.

Methodology — why our findings are investable

PW Consulting’s conclusions are derived from a layered-triangulation methodology combining patent-citation mapping, controlled component teardowns, confidential OEM procurement interviews, and proprietary shipment and aftermarket telemetry. We calibrate our market model to observed contract flows and validated production data to minimize distributional assumptions. Where public disclosure is limited, we use anonymized supplier-level telemetry and cross-validate against patent filings and qualification timelines to produce defensible forward curves.

Practically, this means our non-public inputs come from firm-level interviews, third-party teardown labs, and anonymized production monitoring rather than speculative desk estimates. We preserve client confidentiality while surfacing the actionable signals that substantiate risk-adjusted recommendations.

Implications for 2026 capital and procurement choices

Executives should treat 2026 as a decision window where delaying small, targeted actions amplifies downstream cost and qualification risk. Recommended directional moves include accelerating design-win support for electrified platforms, stress-testing BOMs against commodity scenarios, and prioritizing capacity investments in regions that reduce tariff exposure. The full report maps specific trigger points for these actions tied to OEM program timelines.

To access PW Consulting’s granular playbooks, supplier matrices, and scenario toolkits — and to benchmark your organization’s exposure to the forces outlined above — download the full Automotive Clutch Market report here: https://pmarketresearch.com/auto/automotive-clutches-market .

For detailed analysis of this topic, please visit the official page: Automotive Clutch Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.