PW Consulting Forecasts Viscometers Market to Expand at a 6.9% CAGR Through 2032

Viscometers Market 2026: Strategic Imperatives for Allocation, Compliance, and Design Wins

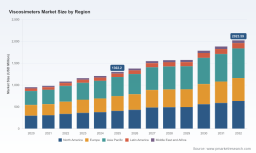

PW Consulting releases a focused industry briefing derived from our comprehensive Viscometers Market study (base year 2025). The global market is in an expansion phase—recovering from supply-chain disruptions and accelerating under increased demand for inline monitoring and biopharma analytics. Our model shows the market expanding from 215.0 Million USD in 2025 to 339.9 Million USD by 2032, at a compound annual growth rate of 6.9%. These macro dynamics create discrete windows for capital deployment and capability building in 2026.

Viscometers Market

Executive snapshot

Key strategic signals that should inform 2026 capital allocation and operational planning:

- Market growth is steady and measurable: PW Consulting projects double-digit adoption in several process and biopharma pockets even as the overall market grows at 6.9% CAGR.

- Fragmented supplier landscape: concentration metrics indicate a fragmented market (CR3 24.6%, CR5 26.2%), creating opportunities for focused players to capture niche design wins.

- Regulatory and standards pressures are rising: ISO 13485, ASTM guidance, and reimbursement classifications are shaping procurement and validation timelines.

- Material and supply-chain friction remains a tactical risk—medical-grade stainless 316L price stabilization is visible but still material to BOM decisions.

Why 2026 is a decisive year

In 2026 the market environment converges on three forces that make near-term strategy both urgent and actionable:

- Operational digitization: Manufacturers implement AI-enabled process control and demand viscometers with digital outputs, deterministic calibration, and secure data pipelines.

- Regulatory tightening and clinical adoption: Devices intended for medical or biopharma use require documented quality management and, increasingly, certifications aligned with ISO 13485 and relevant ASTM methods.

- Shift to continuous and inline processes: Continuous pharmaceutical manufacturing and in-line lubricant monitoring elevate the strategic value of vibrating, inline, and microfluidic viscometry over legacy benchtop-only solutions.

What our report delivers — actionable tools, not just charts

PW Consulting positions this research as a decision-making toolkit for executives allocating budgets in 2026. The report is structured around applied modules that translate market intelligence into executable initiatives:

- Supply-chain map: component-level supplier networks, single-source risk flags, and second-source candidate lists—presented as a navigation layer for procurement and sourcing teams.

- BOM decomposition logic: a reproducible method to reverse-engineer cost drivers in viscometer assemblies so leadership can locate 1–3 cost levers without redesigning the instrument.

- Yield-adjustment and validation models: scenario-based models that quantify time-to-compliance and validation cost under different design and manufacturing choices.

- Technology roadmap: a staged view of sensor fusion, microfluidics, and edge analytics adoption—priced for probabilistic investment planning rather than deterministic mandates.

- Commercial playbooks: design-win frameworks and integration checklists for OEMs and system integrators targeting continuous manufacturing lines.

Each tool is accompanied by caseable use-cases showing how procurement, R&D, and regulatory affairs teams reduce calendar risk and cost-to-market in 2026.

Competitive landscape: dimensions that matter for 2026 design wins

The competitive field is differentiated by discrete defensive and offensive capabilities rather than by sheer scale. Our analysis isolates the competitive dimensions that define which vendors win integrations and which remain instrument sellers:

- Standards and regulatory moat: Companies that embed ASTM/ISO-compliant workflows and hold medical-device certifications secure longer procurement cycles from regulated buyers.

- Systems integration and OEM partnerships: Firms with established API/fieldbus interfaces and proof-of-concept integrations into continuous lines achieve faster design wins.

- Proprietary sensing and consumables: Vendors that couple hardware with unique consumables or cartridges create recurring revenue and stickiness.

- Service footprint and calibration networks: On-site calibration and rapid-response field service remain decisive for process-critical applications in oil & gas and pharma.

- Application-specific know-how: Depth in polymer rheology, blood-plasma analytics, or drilling-fluid testing drives premium positioning and custom validation packages.

Representative competitor archetypes in the field illustrate these dimensions:

- Technology integrators with broad portfolios and automation focus (e.g., firms known for rotational, capillary, and process units) lean on automation and compliance as their primary moat.

- Specialist instrument makers who own unique detection modalities (e.g., dynamic light scattering or microfluidic VROC) monetize precision and small-sample advantages in biopharma R&D.

- Process-focused suppliers that deploy robust inline vibrating sensors and field service support capture continuous-manufacturing and refinery use-cases.

Recent visible moves support these observations: a pharmaceutical-focused automated viscometer launch in late 2025, ISO 13485 certification wins for microfluidic devices, and OEM distribution partnerships announced in 2025—these events validate the strategic vectors we detail in the report.

For granular competitive positioning, product-to-application mapping, and vendor capability matrices, access the full dataset and supplier scorecards here: Download the full Viscometers Market report .

Methodology — how PW Consulting constructs a higher-confidence view

Our study applies layered triangulation to reconcile public filings, proprietary shipment reconciliations, and primary-source interviews. Key elements of our approach include patent citation analysis to identify emerging sensing modalities, customs and shipment reconciliations to approximate installed base movement, and anonymized supplier interviews to validate BOM reconstructions. We supplement this with laboratory visits and instrument teardown exercises to calibrate component-level cost models.

Where data is not public, we rely on non-attributable industry interlocutors, contractual disclosure continuations, and validated secondary sources. All non-public inputs are captured under confidentiality protocols and cross-validated by at least two independent channels before incorporation. This layered approach explains the directional accuracy of the models included in the report while preserving commercial confidentiality.

Implications for 2026 capital allocation and M&A

Based on our scenario analysis, executives should prioritize a balanced portfolio of initiatives to manage risk and capture upside in 2026:

- Invest in integrations and software: allocate near-term budget to retrofit projects that enable viscometers to stream validated data into MES/SCADA and AI analytics.

- Secure critical components: hedge exposure to medical-grade stainless and microfluidic consumables by qualifying alternative suppliers and negotiating long-term contracts.

- Certify for regulated markets: accelerate quality-system upgrades and pursue targeted certifications where clinical or pharmaceutical revenue is expected.

- Pursue tuck-in M&A for analytics and consumables: acquire software or cartridge suppliers that de-risk design wins and add recurring revenue.

- Embed ESG and trade-compliance checks into procurement: traceability of materials and export-control screening prevent validation delays and reputational risk.

Operational playbook—examples of short-cycle moves

Leaders can apply three short-cycle interventions in 2026 that improve margins or defend contracts within 6–12 months:

- Use BOM decomposition to identify 2–4 high-cost components and run a rapid supplier qualification sprint to identify lower-cost equivalents without revalidating field performance.

- Deploy yield-adjustment models during pilot production to quantify incremental validation cost vs. time-to-revenue for certification-heavy customers.

- Stage a product roadmap that sequences microfluidic and inline variants earlier in markets with the fastest regulatory clarity to accelerate commercial uptake.

Next steps and where to read the full intelligence

PW Consulting’s Viscometers Market report is designed to convert market intelligence into executable actions for 2026. The public briefing here highlights the strategic levers—detailed segmentation maps, region- and application-level distributions, supplier scorecards, and reproducible models are available only in the full report. Access the complete report and the downloadable appendices here: Get the complete Viscometers Market report .

For detailed analysis of this topic, please visit the official page: Viscometers Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.