PW Consulting Forecasts Scandium Oxide Market to Grow at 4.3% CAGR Through 2032

Scandium Oxide Market — Strategic Briefing for 2026 Capital Allocators

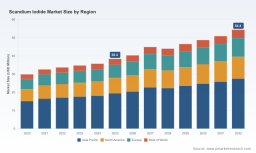

As PW Consulting’s lead industry analyst, I present an executive briefing drawn from our latest Scandium Oxide Market research (base year 2025). This note synthesizes the report’s strategic value for corporate and investor decision-making in 2026, spotlighting actionable frameworks, competitive dimensions, and the urgent timing for capital allocation. The underlying dataset shows the market expanding from USD 45.2 Million in 2020 to USD 55.5 Million in 2025 and continuing on a steady trajectory (CAGR 4.3%) through our forecast window; by 2032 the market reaches approximately USD 73.8 Million under current assumptions. The purpose here is to demonstrate the depth of PW Consulting’s analysis while directing decision-makers to the full report for proprietary breakdowns and region/application distribution maps.

Scandium Oxide Market

Market Snapshot and 2026 Context

In 2026 the scandium oxide ecosystem is characterized by constrained upstream supply, concentrated industry structure, and differentiated demand pockets that reward technical trust and certification. Global primary supply remains tight—industry estimates and USGS references indicate production-levels measured in tens of tons per year, with installed capacity materially above current output but unevenly distributed. Notably, a set of new pilot projects and capacity debottlenecking efforts are altering the supply backdrop; one public example is a 1.5-tonnes-per-year pilot commissioned from red-mud feedstock and timed to come online around the end of 2025.

Scandium Oxide Market

These supply signals interact with persistent price dispersion across purity grades and compound forms. Market concentration is meaningful: the top three producers account for roughly 55% market share (CR3) and the top five roughly 70% (CR5), creating a supplier landscape where design wins and off-take relationships can be as valuable as process IP.

Why 2026 Is a Pivotal Year for Strategic Moves

-

Supply tightness vs. latent capacity: Firms that secure validated off-take and multi-source supply in 2026 will avoid costly production interruptions and inventory-driven price volatility in downstream manufacturing.

-

Regulatory and ESG pressure: Global trade compliance and upstream footprint transparency are now procurement gating factors for OEMs, especially in aerospace, defense, and critical infrastructure segments.

-

Technical validation premium: High-purity scandium products used in alloys, specialty lighting, and energy devices command a trust premium—winning qualification cycles in 2026 shortens lead times to commercial adoption.

-

Capital allocation squeeze: Given the moderate but persistent CAGR and high per-unit value, timing of brownfield vs greenfield investment materially affects IRR models for new entrants and expansions.

Implications for Corporate Strategy

Executives should prioritize three concurrent tracks in 2026: secure validated multi-sourcing, accelerate qualification programs with key OEMs, and embed upstream transparency into procurement contracts to meet compliance and ESG metrics. These are not abstract best practices—our scenario and stress-testing models show they materially change cash-flow risk profiles for manufacturing programs that rely on scandium inputs.

What the PW Consulting Report Includes — Tools Designed for 2026 Problems

Our Scandium Oxide Market report is deliberately operational. Below are the principal analytic modules and how each directly addresses 2026 decision pain points.

-

Supply-chain map and counterparty profiles — Identifies critical raw-material vectors, alternate feedstock routes (including red-mud and matte concentrates), and second-tier processors. Use case: fast-tracking contract counterparties that meet ESG and quality gates.

-

BOM decomposition logic and purity-pathway diagnostics — A repeatable framework for reverse-engineering product bills of materials to quantify scandium content by application class and purity requirement. Use case: cost-to-serve modelling for pricing strategies in alloys and specialty compounds.

-

Yield-adjustment and ramp models — Parametric models that translate raw scandium feedstock quality and processing yields into effective delivered volumes across purity bands. Use case: scenario planning for brownfield capacity expansions versus outsourced toll-processing.

-

Technology roadmap and critical-process scorecards — Comparative assessment of separation, hydrometallurgical, and iodide synthesis routes, including typical bottlenecks, capital intensity, and regulatory implications. Use case: selecting low-risk technology partners for scale-up in 2026.

-

Cost build-up templates and benchmarking panels — Granular cost models (materials, utilities, waste handling, certification) calibrated against PW’s proprietary shipment and pricing panel. Use case: validating supplier quotes and underpinning negotiation anchors.

Competitive Dynamics — How Market Leaders Compete in 2026

Across the supplier universe, competition is less about price-tinkering and more about a set of interlocking capabilities. The following competitive dimensions emerge as decisive in 2026:

-

Purity and quality certification — Being able to reproducibly deliver ultra-high-purity grades with trace-impurity control is a gating factor for aerospace alloys and specialty optics.

-

Supply-chain control and feedstock optionality — Firms that control feedstock sourcing or maintain tolling agreements reduce feedstock price exposure and can offer more stable delivery windows.

-

Regulatory and ESG alignment — Certification, audit-readiness, and minimized environmental externalities become non-negotiable for large OEMs and government contractors.

-

Customer intimacy and qualification pipelines — The ability to move from sample to design win via rigorous test protocols shortens time-to-revenue for higher-volume applications.

-

Scale economics vs niche premium positioning — Some suppliers optimize for low-volume, high-margin laboratory and research channels, while others pursue scale into alloy and energy markets.

PW Consulting’s company canvassing finds these dimensions playing out across the incumbent and specialty suppliers. For example:

-

American Elements: recognized for ready access to high-purity iodide products and deep distribution channels that serve research and industrial labs. Their moat is product breadth and logistics reach into small-batch consumers.

-

Thermo Scientific Chemicals (formerly Alfa Aesar): leverages established laboratory reagent channels and brand trust for ultra-dry compound supply; their key strength is institutional certification and traceability demanded by research customers.

-

AEM REE and Heeger Materials: regional manufacturing footprint and cost-competitive supply positions them well for luminescent and metal-halide feedstock—their competitive edge is process know-how and proximity to feedstock sources.

-

Stanford Advanced Materials and Sigma-Aldrich (Merck): play the high-trust, high-purity laboratory and specialty materials role, where technical datasheets, lot testing, and fast small-batch fulfillment determine design wins.

These vignettes illustrate the report’s granular vendor archetypes and the procurement scorecards we use to map buyers’ needs to supplier profiles. For readers evaluating partnerships or M&A targets in 2026, these profiles are essential because they make the trade-offs between supply security, cost, and compliance explicit.

Methodology: How PW Consulting Sources and Validates Non-Public Insights

Our analysis uses a layered triangulation methodology combining patent-citation mapping, customs-level trade flow analysis by HS code, confidential supplier interviews, on-site facility assessments, and calibration with public filings and academic literature. We then reconcile these independent layers through probabilistic weighting to produce the reported market figures and risk scenarios.

Notably, non-public inputs include: structured interviews with technical leads at processing plants, anonymized shipment records from our proprietary logistics panel, and lab-verified BOM assessments commissioned by PW. We disclose our methodological logic and confidence intervals in the report so decision-makers can understand the provenance and limitations of each inference without exposing raw supplier-level data.

Strategic Recommendations for 2026

-

Lock multi-source off-take with staged qualification clauses: prioritize one validated primary supplier plus a second validated tolling partner within 12 months.

-

Invest in qualification and co-engineering cycles now: suppliers that can support accelerated material testing and qualification into alloys and fuel-cell assemblies secure premium long-term contracts.

-

Embed ESG and trade-compliance clauses into procurement: require upstream disclosure and audit rights to reduce regulatory and reputational risk.

-

De-risk scale via staged CAPEX and offtake-linked financing: use yield-adjustment models in the report to justify phased investments rather than large upfront greenfield commitments.

Where to Find the Full Intelligence

This briefing highlights the strategic contours we see for 2026, but intentionally omits the detailed regional, type and application split tables, supplier-level forecasts, and the full set of sensitivity runs—these are available in the complete PW Consulting report. Access the full market distribution maps, supplier scorecards, and downloadable modeling templates here: Access the full PW Consulting Scandium Oxide Market report .

Final Note — The Investment Clock Is Ticking

With supply-side pilot projects coming online and downstream qualification cycles still in progress, 2026 is a decisive year for firms to solidify their supply architecture and secure cost and compliance advantages. PW Consulting’s toolkit is designed to convert market intelligence into executable procurement and investment choices that materially change risk-adjusted returns. For capital allocators and procurement leaders, the question is not whether to act, but how to act with the right information and contractual levers; our full report supplies those items in operational form.

For detailed analysis of this topic, please visit the official page: Scandium Oxide Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.