PW Consulting Forecast: IR Spectroscopy Equipment Market to Grow at 5.8% CAGR, Rising from USD 1,242.1 Million in 2025 to USD 1,835.3 Million by 2032

IR Spectroscopy Equipment Market: Strategic Imperatives for Capital Allocation in 2026

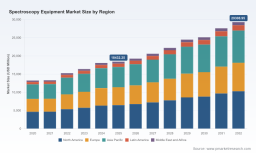

As of 2026, the global IR spectroscopy equipment market sits at an inflection point that demands executive attention. Our latest PW Consulting market study — anchored on a 2025 base year and projecting through 2032 — finds the market expanding at a compound annual growth rate (CAGR) of 5.8%. The market value advances from USD 1,242.1 Million in 2025 toward an estimated USD 1,835.3 Million by 2032, driven by accelerating demand across regulated laboratories, on-site process control, and integrated hyphenated systems. This briefing summarizes the strategic value of the full report for 2026 decision-making while intentionally withholding detailed segment-level allocations to encourage access to the underlying intelligence.

IR Spectroscopy Equipment Market

Market Snapshot: What the High-Level Numbers Mean for 2026

High-level trends are clear: growth is steady but non-linear, with episodic rebounds reflecting cyclical lab upgrades and pockets of rapid adoption for portable and hyphenated IR solutions. Market concentration remains moderate — the top three firms account for 38.2% of revenue and the top five for 48.5% — signaling room for differentiated challengers while highlighting the importance of scale in manufacturing, service, and global distribution.

- Growth driver profile: regulatory tightening in environmental and pharmaceutical testing, coupled with industry adoption of inline process analytics, is reshaping capex plans.

- Cost and supply-side pressures: optics and specialty gas supply volatility are compressing margins for both OEMs and OEM buyers.

- Technology adoption: the migration from standalone benchtop instruments to portable and hyphenated IR configurations is creating new lifecycle and service revenue streams.

Why 2026 Is a Strategic Inflection Point

2026 is the year boards and CIOs must translate high-level optimism into concrete capital allocation decisions. Three contemporaneous forces create urgency:

- Regulatory momentum: updates to test methods and accreditation requirements (for example, recent revisions impacting environmental and semivolatile analysis workflows) are accelerating instrument refresh cycles and compliance-driven purchases.

- Supply-chain shocks: persistent pressure on fused silica optics and specialty cryogens in prior years has increased procurement lead times and handed bargaining leverage to a small group of upstream suppliers.

- Technology convergence: greater integration of IR modules with chromatography and mass spectrometry, plus AI-enhanced spectral libraries, is shifting value from hardware features alone to platform-level design wins.

These dynamics mean that timing, vendor selection, and procurement strategy for spectroscopy equipment in 2026 will materially influence TCO and regulatory risk profiles for the next decade.

Practical Tools Included in the Full Report (How They Address 2026 Pain Points)

The full PW Consulting offering is deliberately operational. The tools are built for procurement teams, R&D and QA leaders, and private-equity investors who need executable inputs — not abstract forecasts. Representative content includes:

- Supply-chain topology maps that trace critical upstream nodes (optics, detector wafers, specialty gases) and identify single points of failure; useful for scenario planning and dual-sourcing strategies.

- Bill-of-Materials (BOM) disassembly logic that links component cost drivers to end-product price sensitivity, enabling targeted cost-reduction programs and supplier negotiation levers without disclosing proprietary BOM figures.

- Yield-adjustment and manufacturing ramp models showing how throughput, test yield, and service part availability affect margins during scale-up or product refresh cycles.

- Technology roadmaps mapping incremental and disruptive trajectories for benchtop, portable, and hyphenated IR systems — organized to highlight feature sets that tend to win design-ins for regulated customers.

- Regulatory and trade risk matrices (including dual-use export-control overlays) that translate policy shifts into procurement and localization decisions for both OEMs and end users.

Each tool is accompanied by scenario playbooks focused on cost control, compliance assurance, and supplier risk mitigation — these playbooks show decision logic and execution sequences rather than disclosing raw segment-level numbers.

Competitive Landscape: The Dimensions That Matter in 2026

Our competitive analysis does not predict individual 2026 strategies in full; instead, it dissects the competitive dimensions that determine winners and losers in the IR equipment arena. Across legacy instrument makers and newer entrants, four capability clusters consistently determine outcomes:

- Integrated solutions and platform lock-in: firms that combine hardware with proprietary software, spectral libraries, and lifecycle services convert one-off sales into recurring revenue and higher design-win stickiness.

- Service and global field coverage: rapid uptime restoration, preventive maintenance networks, and certified consumable supply chains are decisive for regulated end users.

- IP and technology depth: patent families and modular optics architectures reduce time-to-market for next-generation sensors and enable vertical integration with chromatography and mass spectrometry.

- Channel and application specialization: targeted end-use expertise (pharma, environmental, industrial QC) combined with validated method packages creates a compelling buying proposition for regulated labs.

Leading players in the broader spectroscopy ecosystem — from established multinational instrument groups to specialized optical providers — exhibit combinations of these capabilities. For procurement teams, assessing prospective suppliers against these dimensions is more predictive of long-term success than focusing on point-feature comparisons. For a deeper company-by-company competitive matrix that maps these capability clusters to observable indicators, consult the full report.

Access the full competitive matrix and company capability maps here .

Strategic Implications and 2026 Recommendations

Based on our layered analysis, executives should prioritize three concurrent actions in 2026:

- Rebalance procurement toward platform and service economics: negotiate contracts that tie pricing to uptime SLAs, certified consumables, and accelerated field-service response — reducing total cost of ownership even where unit prices are higher.

- Harden supply chains for critical optics and gases: invest in multi-sourced supply agreements, strategic inventory cushions, and design-for-substitutability in instrument models to mitigate supplier-specific shocks.

- Accelerate method validation and digital adoption: integrate AI-assisted spectral interpretation and centralized method validation to shorten lab onboarding cycles and secure regulatory acceptance windows.

These steps convert market growth into durable advantage while protecting operations from regulatory and raw-material volatility that is already evident in 2024–2025 industry data.

Methodology: How We Build Confidential, Actionable Intelligence

PW Consulting’s conclusions are the product of a layered triangulation methodology that blends public records with primary fieldwork and proprietary analytics. Key elements include patent-citation network analysis, customs and shipment flow analysis, reverse engineering of BOMs from fielded units, and structured interviews across OEMs, distributors, procurement officers, and accredited labs. We also synthesize regulatory filings, standards updates, and raw-material pricing data to contextualize demand shocks.

Our approach deliberately emphasizes reproducibility and source diversity. Where public disclosure is limited, we corroborate supplier-level inferences using at least three independent evidence streams (e.g., supplier quotations, customs manifest anomalies, and technician audit logs) before incorporating them into the model. This is how we create estimates of near-term supplier vulnerability and likely impact to instrument lead times without exposing individual suppliers’ confidential pricing.

Risks and Policy Considerations for 2026

Decision-makers must weigh several non-market risks as they craft 2026 capital plans:

- Export control regimes: continued classification of higher-field NMR and certain high-resolution spectrometers as dual-use may constrain cross-border procurement and require local assembly or licensing strategies.

- Commodity and component inflation: optics and specialty gas price fluctuations can materially change vendor margins and shift competitiveness between vertically integrated OEMs and contract assemblers.

- Standards and accreditation dynamics: evolving lab accreditation requirements will alter equipment qualification timelines and increase demand for validated method bundles from suppliers.

These risks underline the imperative to treat spectroscopy equipment purchases not as one-off capital purchases but as strategic investments with regulatory, operational, and supplier dimensions.

Get the Full Playbook

This briefing is deliberately selective — intended to demonstrate the depth and practical orientation of our analysis while preserving the detailed segmentation, regional distribution maps, and company-level scenario outputs for subscribers. For procurement teams, private-equity investors, and OEM strategists preparing 2026 budgets, the full report delivers actionable models, downloadable supplier risk maps, and executable playbooks.

Access the full IR Spectroscopy Equipment Market report and strategic playbooks here .

For detailed analysis of this topic, please visit the official page: IR Spectroscopy Equipment Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.