PW Consulting: Pediatric Cranial Remolding Orthoses Market Poised to Reach USD 359.8 Million by 2032

Pediatric Cranial Remolding Orthoses Market — Strategic Briefing for 2026 Capital Allocation

PW Consulting presents a forward-looking executive analysis of the Pediatric Cranial Remolding Orthoses market as of 2026. This briefing synthesizes historical performance, near-term forecasts, competitive dynamics and the actionable toolset included in our full market study — designed to inform C-suite and investment decisions during a period of accelerated clinical, regulatory and manufacturing change.

Pediatric Cranial Remolding Orthoses Market

Executive snapshot

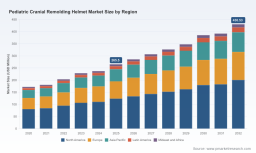

The industry has expanded steadily over the past half-decade, rising from USD 163.1 Million in 2020 to USD 225.1 Million in 2025 (base year). Our model projects continued expansion through the 2026–2032 forecast window, reaching an estimated USD 359.8 Million by 2032 at a compound annual growth rate (CAGR) of 6.98% for the forecast period. These topline dynamics reflect persistent clinical demand, incremental reimbursement normalization, and rapid adoption of digital manufacturing methods — but the pattern of value capture is shifting beneath the surface.

Why 2026 is a pivot year for strategy

Several simultaneous pressures make 2026 a critical decision point for manufacturers, specialty providers and strategic investors:

-

Regulatory tightening and procedural clarity: Devices are regulated as FDA Class II with 510(k) requirements and operational constraints (for example, timelines driven by infant growth that influence fit-and-delivery windows), which amplify the cost of delay and non-compliance.

-

Reimbursement variability: HCPCS billing and payer medical-necessity policies remain uneven across markets and clinical pathways, increasing revenue risk for providers that lack payer engagement capabilities.

-

Operational transformation: The emergence of 3D scanning/printing, bio-based polymers and networked provider models reduce unit costs and raise the bar for design wins — but they also require capital investment and new supplier relationships that must be proven against yield and lead-time targets.

Market dynamics — what is actually driving growth

Growth is not uniform. Instead, it is driven by three reinforcing vectors:

-

Clinical adoption and earlier detection: Increased pediatric screening and earlier referrals lead to a larger addressable treatment window per infant, supporting helmet therapy volumes.

-

Technology-enabled manufacturing: Digital capture (low-error scanning), modular design libraries and additive manufacturing reduce per-unit labor and rework, enabling faster scaling of case throughput where supply chains are integrated.

-

Payer and post-op demand: Expanded recognition of orthoses for post-surgical use in certain craniosynostosis protocols, combined with selective payer coverage, lifts utilization in defined cohorts.

Rather than listing regional or application-level shares in this briefing, the full report maps how these drivers translate into regional shifts, application mix evolution and the movement of market gravity — essential inputs for capital allocation and go-to-market planning. View the complete distribution charts and scenario matrices in the full study.

Competitive landscape — dimensions that determine winners in 2026

Market concentration indicates established incumbency: the three-largest firms account for a dominant portion of market revenue, and the top five hold most of the accessible commercial share. This creates a two-speed market: entrenched clinical networks and specialist manufacturers versus agile entrants leveraging digital fabrication.

Across companies we analyzed, success in 2026 is primarily decided along six competitive dimensions:

-

Regulatory credibility and device clearances — speed to market for updated designs and the ability to document fit windows and biocompatibility.

-

Clinical channel access — direct clinic footprints, referral partnerships and vertically integrated care networks that shorten the patient path from diagnosis to treatment.

-

Design-for-manufacture capability — whether a manufacturer can convert a scan to a low-variance build at scale (key for meeting strict fit timelines and reducing remakes).

-

Material and comfort differentiators — innovations in polymer chemistry and interface materials that improve wear compliance and reduce skin complications.

-

Payer and coding strategy — demonstrated capacity to support HCPCS billing, prior-authorization workflows and post-approval evidence packages.

-

Supply resilience — multi-sourced components and logistics playbooks that mitigate lead-time disruption and preserve clinic throughput.

Prominent market participants illustrate these dimensions rather than defining an immutable pecking order: providers with deep clinic footprints and early FDA clearances sustain a defensive moat through referral density; manufacturers that master 3D printing and bio-based materials capture new value via cost and comfort; large provider networks scale by bundling services and payer relationships. Recent product adoptions and material announcements in 2025–2026 underscore these competitive levers.

Recent developments (directional)

-

National provider networks are integrating 3D-printed orthoses to improve fit precision and patient experience.

-

Material suppliers are commercializing bio-based polymers for cranial devices, creating a sustainable product differentiation path.

-

Payer policy refinement around procedure codes and post-op indications is increasing revenue predictability for compliant providers — but coverage remains contingent on clinical documentation and age windows.

For a company-level view and our assessment of competitive moats and design-win criteria, consult the detailed competitor dossiers in the full report. If you are evaluating specific acquisition targets or JV partners, the report’s situational matrices will materially shorten diligence timelines. Learn more: Full report and company dossiers .

Technology & operations — where margin will be made or lost

Three technology trends converge to reshape unit economics:

-

Scan-to-fit throughput — reducing scanning error and queueing time directly cuts remake rates and improves clinical capacity utilization.

-

Additive manufacturing — selective adoption of 3D printing converts fixed tooling cost into capacity-on-demand, but requires robust quality and yield governance.

-

Material innovation — biocompatible, lower-weight polymers increase wear compliance and reduce follow-up interventions, strengthening payer narratives.

Operationally, the dominant risks are process variance (leading to remakes), inventory of intermediate parts, and compliance failures that trigger corrective actions. Our report provides a structured mapping from design choices to yield implications and regulatory pathways — enabling executives to quantify trade-offs between speed-to-market and cost-to-serve without leaking proprietary modeling assumptions in this briefing.

Practical toolkit inside the full PW Consulting study

The study is purpose-built for executable 2026 plays and includes the following tools and templates that translate analysis into boardroom actions:

-

Supply-chain map and single-page supplier risk heatmap to prioritize dual-sourcing and strategic inventory buffers.

-

BOM disaggregation logic that decomposes a finished orthosis into cost buckets and identifies high-leverage parts for renegotiation or redesign.

-

Yield-adjustment and lead-time sensitivity models to estimate the financial impact of reduced remake rates, faster fits and different manufacturing modalities.

-

Technology roadmap and decision matrix to evaluate when to in-source 3D printing vs. outsource, including compliance checkpoints for 510(k) management.

-

Regulatory-compliance playbook that aligns fit-window constraints, clinical evidence bundles and commercial coding strategy for payer acceptance.

Each tool is accompanied by an implementation checklist and risk mitigations tailored for 2026 realities — for example, how to sequence pilot installations of digital scanners to avoid supply interruptions while preserving clinic throughput.

Methodology — how PW Consulting produces high-confidence insight

Our research applies Layered Triangulation: we combine public registries (FDA 510(k) filings, HCPCS coding guidance), patent and supplier patent-landscape analyses, structured interviews with clinicians and orthotists, and proprietary operational data obtained under NDAs from leading clinics. We perform quantitative cross-checks using practice-level throughput data and supplier quotes to reconcile top-down and bottom-up estimates.

Where direct measurement is unavailable, we derive proxies from correlated signals (clinical appointment cadences, typical wear durations and product lifecycle stages), and we test those proxies via targeted field interviews and blinded validation with device-build partners. This multi-source approach enables us to present actionable scenarios rather than single-point forecasts — and to surface sensitivities that matter to CFOs and operational leaders.

Strategic recommendations for 2026 capital allocation

Based on the analysis, PW Consulting recommends that decision-makers prioritize three investment themes in 2026:

-

Operational resilience: Allocate capital to reduce remake rates and lead times (scans-to-fit and yield governance) before expanding capacity.

-

Regulatory and payer engineering: Invest in documentation and prior-authorization capabilities that convert clinical efficacy into reimbursed volume.

-

Sustainable differentiation: Evaluate selective adoption of bio-based materials and additive manufacturing where they demonstrably improve compliance or reduce total cost of care.

Each recommendation is accompanied in the full report by a five-step implementation roadmap, expected ROI ranges under multiple scenarios, and the key organizational enablers required for execution.

Next steps — how to use this briefing

If you are preparing 2026 budgets, M&A screens or a pilot deployment of digital fabrication, PW Consulting’s market study provides the granular tools and validated assumptions to accelerate decision cycles and reduce execution risk. The full report contains the complete segmentation maps, scenario dashboards and downloadable templates required for rapid due diligence and operational pilots.

Access the comprehensive study and company dossiers here: https://pmarketresearch.com/hc/pediatric-cranial-remolding-helmet-market .

For detailed analysis of this topic, please visit the official page: Pediatric Cranial Remolding Orthoses Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.