PW Consulting Forecast: Solid Phase Extraction Apparatus Market Set to Hit USD 344.8 Million by 2032

Solid Phase Extraction Apparatus Market — Strategic Briefing for 2026 Capital Allocation

PW Consulting publishes an executive briefing drawn from our new market study on the Solid Phase Extraction (SPE) apparatus market. This note synthesizes the evidence base that underpins our 2026 recommendations and highlights why now is a decisive moment for procurement, R&D prioritization, and M&A readiness. The market is mature but dynamic: historical revenues rose from USD 163.1 Million in 2020 to USD 215.0 Million in 2025, and our forecast projects growth to USD 344.8 Million by 2032 at a 2026–2032 CAGR of 5.4%.

Solid Phase Extraction Apparatus Market

Why 2026 is an inflection year

Several converging forces are compressing decision cycles and escalating the value of forward-looking vendor and product choices:

Solid Phase Extraction Apparatus Market

- Regulatory tightening on trace contaminants (e.g., PFAS) is re‑shaping acceptable material specifications and QC test regimes across environmental and public health labs.

- End users demand lower per‑sample operating cost and higher reproducibility as labs scale biomonitoring and environmental testing workloads.

- Supply chain re‑shoring and ESG-driven procurement introduce new constraints on BOM composition and supplier footprint.

- Automation and data integration trends create premium for systems designed for seamless upstream/downstream interfacing rather than standalone manifolds.

Key takeaways for capital allocation

Buyers and investors should treat 2026 as a window to lock in technology and supply relationships that align with compliance and unit‑economics objectives over the next seven years. The dominant risk is not demand shortfall but supplier misalignment: mismatches between consumable ecosystems, regulatory readiness (QC for low‑residual PFAS, method conformity), and manufacturability at scale. PW Consulting’s report privileges actionable diagnostics over hindsight—identifying where small investments in qualifying partners and BOM redesign can convert into outsized OPEX savings and lower compliance risk.

Report tools that address 2026 pain points

Our study includes a suite of practical tools designed for immediate operational use by procurement, engineering, and corporate development teams. These include:

- Supply‑chain topology maps that surface single‑sourced components, logistics chokepoints, and alternate qualified suppliers for critical parts.

- BOM teardown logic that identifies cost‑takeout opportunities and sensitivity of overall yield to specific subcomponents.

- Yield adjustment and scenario models that quantify the trade‑offs between throughput, recovery rates, and per‑sample cost under different quality targets.

- Technology roadmaps that align incremental design investments (e.g., positive‑pressure vs vacuum manifolds, cartridge compatibility) with expected regulatory milestones and buyer preference trajectories.

- Compliance alignment matrices mapping product attributes to prevailing laboratory methods and regulatory references.

Each tool is accompanied by an executable playbook—procedural checklists, vendor qualification templates, and negotiation levers—that teams can apply without waiting for bespoke consultancy. To preserve the report’s strategic value, detailed parameterizations and cell‑level outputs are intentionally withheld here; the full models and downloadable templates are available in the source report.

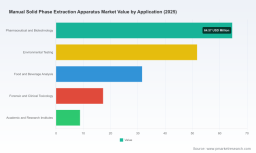

Market sizing and growth drivers

The market’s trajectory reflects steady, diversified demand: routine environmental monitoring, expanded biomonitoring programs, and sustained usage in pharmaceutical and academic laboratories. From a historical base of USD 163.1 Million in 2020 the industry reached USD 215.0 Million in 2025. Our 2026–2032 forecast assumes a 5.4% CAGR and models several demand scenarios tied to regulatory accelerants and automation adoption. Notably, the market remains fragmented—our concentration metrics show that the largest three firms account for roughly 24.6% of global revenue and the top five for about 26.2%—indicating persistent opportunity for mid‑tier suppliers and differentiated new entrants.

Competitive dimensions that determine winners

PW Consulting’s competitive analysis reframes competition as a multi‑axis contest. We evaluate incumbent and emerging suppliers along specific vectors—ecosystem ownership, reproducibility and low‑background footprints, distribution and service networks, and integration readiness for automation. The following general observations summarize where competitive advantage is commonly built:

- Consumables ecosystems: Firms that pair cartridges and manifolds into an integrated consumable/service offering create recurring revenue and higher switching costs.

- Quality and method alignment: Vendors able to demonstrate QC‑tested low residuals (a capability increasingly relevant for PFAS testing) gain early preferential access to regulatory programs and large environmental lab contracts.

- Design compatibility: Design wins hinge on compatibility with common lab workflows—positive‑pressure options for high‑viscosity samples, vacuum manifolds for high‑throughput plate workflows, and cartridge geometries that minimize dead volume.

- Distribution and aftermarket services: Rapid regional service, calibration, and certified consumables shorten qualification cycles and materially affect procurement decisions.

- IP and standards leadership: Patents, validated methods, and close collaboration with standards bodies accelerate acceptance in regulated testing programs.

To illustrate without disclosing proprietary forecasts, our analysis examined public and product‑level traits across market participants including Gilson, Biotage, Chemglass, Labstac, Thermo Fisher, Agilent, Waters, Phenomenex, and Sigma‑Aldrich (Merck). Each brings observable strengths—e.g., established cartridge ecosystems, positive‑pressure designs, or global service footprints—that map directly to the competitive vectors above. The full competitive matrix in the report provides match‑up diagnostics and relative positioning.

Regulatory and method catalysts

Specific regulatory updates are already reshaping product requirements in 2026. For example, cartridge configurations that support PFAS workflows and EPA method compliance are becoming procurement prerequisites; Waters’ development of low‑residual PFAS cartridge options is a case in point. Similarly, persistent reference to manual‑compatible SPE protocols in environmental and biomonitoring lab manuals continues to preserve demand for manual manifolds even as automation grows. PW Consulting models these method‑level shifts into our adoption curves and vendor qualification timelines.

Operational imperatives

Practical actions purchasers and OEMs should prioritize in 2026 include:

- Qualify suppliers on method‑level performance (not just nominal specs), including documented low‑residual testing where applicable.

- Run BOM re‑optimizations to identify where localized sourcing or component redesign can reduce lead times and cost per sample.

- Embed yield‑adjustment scenarios into capital approval processes so that procurement decisions reflect realistic throughput and scrap assumptions.

- Negotiate SLAs that encompass calibration, consumables availability, and regulatory support for labs implementing new methods.

- Prioritize platforms designed for modular automation interfaces to future‑proof capital investments.

Methodology — why our conclusions are actionable

PW Consulting relies on a layered triangulation methodology combining: patent citation analytics to surface innovation clusters; proprietary BOM teardowns and factory audits to assess manufacturability and cost structure; customs and logistics flow analyses to map supply risks; and structured interviews with laboratory procurement, head engineers, and regulatory program managers for on‑the‑record validation. In addition, we use machine‑assisted signal extraction from procurement notices and design‑win disclosures to detect early market shifts. This multi‑source approach allows us to infer commercially significant but non‑public dynamics—such as consumable dependency ratios and tender qualification criteria—without disclosing counterparty‑sensitive detail.

Next steps and how to access the full intelligence set

PW Consulting’s full report contains the executable models, regionally disaggregated demand maps, supplier scorecards, and downloadable negotiation templates referenced above. For procurement directors, R&D leads, and corporate development teams planning 2026 allocations, the report converts strategic options into prioritized, risk‑weighted actions. Access the comprehensive study, interactive dashboards, and model templates here: https://pmarketresearch.com/worldwide-manual-solid-phase-extraction-apparatus-market-research .

For detailed analysis of this topic, please visit the official page: Solid Phase Extraction Apparatus Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.