PW Consulting: Electrolyte Analyzers Market Poised for Steady Growth with a 5.7% CAGR Through 2032

Electrolyte Analyzers Market — Strategic Preview for 2026

Executive snapshot

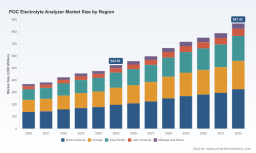

PW Consulting’s latest market briefing positions the worldwide electrolyte analyzers market as a steady-growth medical device segment now entering a phase of selective capital allocation and technology consolidation. The market expands from an estimated USD 163.2 Million in 2020 to USD 215.0 Million in our 2025 base year and is forecast to reach USD 344.8 Million by 2032, reflecting a compound annual growth rate (CAGR) of 5.7% over the forecast window. These headline numbers underscore both the resilience of near-patient testing demand and the mounting pressure on OEMs and buyers to optimize cost, compliance and clinical workflow integration in 2026.

Electrolyte Analyzers Market

Why 2026 is a decision-point year

Now (2026) the market is characterized by three concurrent dynamics that force strategic choices for device manufacturers, hospital procurement teams and investors:

Electrolyte Analyzers Market

-

Operational intensity in acute care: emergency, ICU and high-throughput lab settings continue to drive demand for fast, small-sample electrolyte testing — but value now hinges on total cost of ownership, not just device speed.

-

Regulatory and reimbursement friction: FDA review cycles and CPT-coded reimbursement structures remain material gating factors for US market entry and adoption timing, elevating the premium on regulatory readiness and evidence generation.

-

Technology migration and supplier economics: innovations in micro-sampling, maintenance-free sensor chemistries and integrated analytics are altering consumable lifecycles and BOM structure; concurrently, CapEx and consumable expense profiles continue to restrict broader adoption beyond large hospital centers unless unit economics are rebalanced.

Market trajectory and strategic implications

The market’s steady 5.7% CAGR masks important inflection points that are actionable in 2026. PW Consulting identifies the pivot from unit-sales-driven competition toward a platform-and-consumable economics model as the defining strategic fault line. Companies that establish defensible recurring-revenue streams through consumables, intelligent quality management and integrated clinical decision support capture disproportionate long-run value. For health systems, the strategic question in 2026 is selective concentration of POC assets where throughput and acuity justify the higher marginal costs — and establishing multi-vendor procurement playbooks that prioritize interoperability and lifecycle guarantees.

Report deliverables: Tactical tools for 2026 execution

Our report is designed as an operational toolkit for executives making procurement, R&D and M&A decisions in 2026. Key deliverables include:

-

Supply-chain topology and supplier-risk maps showing second- and third-tier dependencies across critical subcomponents, with scenario triggers for semiconductor and reagent supply shocks.

-

BOM decomposition logic and cost-sensitivity templates that let procurement model alternative sourcing and yield-improvement levers without exposing raw supplier pricing.

-

Yield-adjustment and throughput models that translate manufacturing process improvements into consumable cost curves and service cadence implications for field-install base.

-

Technology roadmaps that align sensor chemistry, microfluidics and embedded analytics to five commercialization pathways and regulatory timing bands.

Each tool is operationalized for 2026 use cases — for example, enabling a hospital chain to quantify break-even thresholds for replacing legacy benchtop analyzers with POC platforms under constrained CapEx plans, or allowing an OEM to prioritize R&D investments that will materially reduce per-test consumable cost.

Competitive landscape: dimensions that matter

The market’s vendor set includes global diagnostic OEMs, specialized POC players and regional low-cost suppliers. Rather than predicting each company’s 2026 playbook, PW Consulting focuses on the competitive dimensions that determine sustainable advantage:

-

Installed-base and service network: companies with dense hospital footprints and rapid field-service capabilities convert trial deployments into sustained design wins because uptime and calibration cadence are critical in acute settings.

-

Consumable lock-in and chemistry IP: firms that couple proprietary sensor chemistries or single-use cassette designs with demonstrable quality-management features convert device procurement into recurring revenue relationships.

-

Integration with clinical IT and decision-support: partners that can embed electrolyte results into physiological trend analytics or EMR workflows increase clinical reliance on POC outputs and raise switching costs.

-

Regulatory track record and evidence-generation capability: demonstrated ability to navigate FDA pathways, and to supply peer-reviewed clinical performance data, materially shortens sales cycles in regulated markets.

Established multinational players and several specialized POC vendors each exhibit combinations of these moats in 2026; market concentration is moderate, leaving room for targeted entrants that can displace incumbents on one or two of the dimensions above.

Recent industry signals and what they imply

Recent product clearances, strategic partnerships and launches indicate two practical trends:

-

Quality automation is becoming table stakes. The introduction of POC systems with in-line hemolysis detection and intelligent quality management accelerates clinical acceptance by reducing false positives and maintenance burden.

-

Data and physiology integration amplifies platform value. Partnerships that link blood gas/electrolyte outputs with continuous physiological monitoring create differentiated clinical workflows that favor incumbents who can demonstrate improved decision-making time.

These signals reinforce the recommendation that OEMs prioritize investments that simultaneously reduce consumable variability and create interoperable clinical value — an approach that materially improves tender outcomes in 2026.

How PW Consulting’s report solves 2026 pain points

Health systems face acute pressures to control costs while meeting compliance and ESG goals in procurement. OEMs and suppliers grapple with tightening margins and longer regulatory timelines. Our suite of deliverables maps directly to these pain points by providing:

-

Operational levers to reduce per-test costs via supplier re-design and yield-improvement recommendations.

-

Regulatory readiness templates that accelerate evidence generation and align clinical trials to reimbursement timelines.

-

Supplier risk mitigation playbooks that meet ESG sourcing expectations while preserving supply continuity.

Methodology — how we know what others don’t

PW Consulting’s analysis in this report is grounded in layered triangulation: we combine patent landscaping, regulatory filing audits, proprietary procurement datasets, supplier interviews and reverse-engineered BOM assessments to build a multi-source confidence model. Where public filings are thin, we use anonymized purchasing logs from hospital networks, structured interviews with OEM supply-chain executives, and lab-validated bench testing to validate component cost and yield assumptions.

The result is a replicable evidence chain: patent claims are cross-referenced to supplier part lists; regulatory timelines are mapped against internal clinical dossiers; and procurement pricing bands are correlated with BOM-derived cost floors. This approach allows us to surface non-public operational levers — for example, which subcomponents disproportionately influence per-test economics — without disclosing confidential supplier numbers.

Actionable guidance for 2026 stakeholders

Based on our analysis, PW Consulting recommends three priority actions for 2026:

-

For hospital systems: adopt a dual-track procurement strategy that preserves high-availability POC capacity in critical units while negotiating outcome-linked consumable contracts that cap variable spend.

-

For OEMs: prioritize product architectures that minimize field-service interventions and maximize consumable lock-in via demonstrable quality management and data integration capabilities.

-

For investors and acquirers: evaluate targets by their ability to deliver integrated platform value (device + consumable + analytics) and by the transparency of their supply chain risk profile — both are decisive in 2026 valuations.

Where to get the full operational intelligence

PW Consulting is publishing this briefing as a preview of the comprehensive Electrolyte Analyzers Market report. The full report contains detailed distribution maps, supplier-by-component sensitivity tables, bill-of-materials scenarios and executable supplier-risk mitigations that support immediate 2026 capital allocation and product strategy decisions. Access the full report and purchase options here: Worldwide POC Electrolyte Analyzer Market Research .

Closing perspective

2026 is a year of choice for participants in the electrolyte analyzers ecosystem. The underlying clinical need for rapid, reliable electrolyte measurement remains robust, but margin compression, regulatory friction and the economics of consumables mean that only those organizations that systemically address device uptime, lifecycle cost and clinical integration will win sustainable share. PW Consulting’s report equips leaders with the operational, regulatory and competitive intelligence needed to make those choices confidently.

For detailed analysis of this topic, please visit the official page: Electrolyte Analyzers Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.