PW Consulting Forecasts Metallographic Cutting Machine Market to Expand at a 5.2% CAGR During 2026–2032

Metallographic Cutting Machine Market — Strategic Outlook for 2026: Why Leaders Must Recalibrate Investment and Sourcing

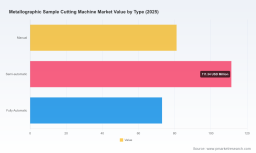

PW Consulting releases a focused industry briefing derived from our comprehensive Metallographic Cutting Machine Market study. The analysis uses 2025 as the base year and projects through 2032, with a compound annual growth rate (CAGR) of 5.2% for the forecast horizon 2026–2032. The global market is measured across a multi-year series (2020–2032) and shows a clear expansion from 2020 levels to an estimated 592.0 Million USD by 2032, signalling sustained opportunity for suppliers, OEMs, and end‑users allocating capital in 2026.

Metallographic Cutting Machine Market

Executive snapshot

Key, actionable observations for decision makers:

Metallographic Cutting Machine Market

- The market is growing at a steady, single‑digit CAGR (5.2%) driven by higher sample‑throughput requirements, materials diversity (from soft alloys to high‑HV ceramics), and rising automation in lab workflows.

- Market concentration is meaningful: the top three vendors account for c.75.0% of market share, and the top five for c.85.0%, creating both entry barriers and consolidation opportunities.

- Technology and service are co‑equal battlegrounds — precision hardware alone no longer secures Design Wins; after‑sales services, consumables strategy, and integrated software workflows are decisive.

- Supply chain and raw material dynamics are immediate levers for margin management: abrasives mix, mounting consumables, and sourcing of diamond wheels materially affect unit economics.

Why this matters in 2026

By 2026 firms face intersecting pressures that make timing critical for capital allocation:

Metallographic Cutting Machine Market

- Regulatory and compliance requirements continue to firm up around sample traceability and standardized preparation protocols, increasing the cost of non‑conformance for large labs and OEM test houses.

- ESG and Scope 3 considerations increasingly influence procurement: energy efficiency, consumable lifecycle, and local supply continuity matter when evaluating total cost of ownership.

- AI‑enabled process optimization is shifting value from raw throughput to data‑driven yield improvements; vendors that can embed analytics into cutting workflows unlock disproportionate ROI for customers.

What PW Consulting’s report delivers — practical toolkits, not platitudes

This study is engineered to be operationally useful for procurement, R&D, and strategy teams preparing 2026 budgets. The report contains proprietary instruments designed for immediate implementation:

- Supply‑chain topology and risk maps that show supplier tiers, single‑sourced nodes, and substitution pathways to speed contingency planning without exposing contract specifics.

- BOM decomposition logic and cost‑baseline templates that let users model component‑level cost drivers (motors, gearboxes, control electronics, wheels, coolants) and run sensitivity scenarios.

- Yield‑adjustment models that translate sample damage rates and rework into financial impact across lab portfolios — enabling rapid prioritization of capex for automation versus consumable upgrades.

- Technology roadmaps and capability matrices that align machine classes (manual, semi‑automatic, fully automatic) with typical laboratory workflows and downstream analytical requirements.

- Procurement playbooks and vendor benchmark frameworks designed to integrate compliance checks (standards adherence) and ESG KPIs into supplier scorecards.

Each toolkit is accompanied by implementation notes that explain how to apply them to concrete 2026 problems — for example, isolating the marginal benefit of a fully automatic cut‑off when throughput increases by X% or when a new alloy category enters the lab workload. Full calibration parameters and model inputs are held in the primary report to preserve commercial value and guide bespoke scenarios.

Competitive landscape — the axes of competition you must model

The market’s competitive dynamics are dominated by a mix of long‑standing precision incumbents and nimble regional players. Rather than rehearse product lists, PW Consulting frames competition along the dimensions that determine wins and margins:

- Product engineering moat — vendors with demonstrable low‑deformation cutting technologies and validated cutting protocols preserve premium pricing. Precision in microstructure preservation is a repeat Design Win factor for tier‑1 material labs.

- Service and consumable ecosystem — firms that bundle consumables, maintenance packages, and calibration services capture recurring revenue and strengthen customer lock‑in.

- Distribution and demo capability — mobile labs, regional demo fleets, and strong channel relationships lower the purchase friction for capital equipment and accelerate specification shifts.

- Systems integration — providers that enable data export, traceability, and process analytics create stickiness with enterprise customers pursuing lab digitization.

Applying these axes to the key players we track yields differentiated profiles (examples):

- Struers — positioned on precision engineering and an extensive product menu; moat lies in demonstrable low‑deformation technologies and strong laboratory brand recognition.

- Buehler (Illinois Tool Works Inc.) — a legacy brand with strength in consumable integration and broad channel access, enabling repeatable throughput wins across sectors.

- LECO Corporation — notable for handling large and complex samples; its trade‑show visibility and system breadth are tools for enterprise engagements.

- QATM (VERDER Group) — differentiates through modularity and accessibility, reinforced by active field demonstration programs.

- Metkon, NextGen, Trojan (Suzhou), PACE — regional and specialty suppliers that compete on cost, niche capacity, or service agility; these players are critical when mapping supply resilience and price pressure scenarios.

Recent vendor developments (guide releases, mobile demos, trade show activity) underscore an industry pivot toward field enablement and customer education — signals we incorporate in our Design Win probability frameworks. For a deeper vendor‑level competitive matrix and our proprietary scoring method, Access the full report.

Regulatory and raw‑material dynamics to model now

Two operational realities are shaping near‑term supplier selection and capex decisions:

- Standards and traceability — established ISO and national standards for specimen selection, cutting, and cleaning are increasingly invoked in procurement contracts, raising the cost of noncompliant equipment.

- Consumable economics — the choice between abrasive discs and diamond wheels is not purely technical: abrasives reduce upfront cost and speed cutting for softer metals, while diamond wheels are financially rational for high‑hardness materials and specialty labs once lifetime costs are modeled.

Methodology — why our findings are defensible and actionable

Our research follows a layered triangulation methodology that combines patent‑citation analysis, primary interviews, proprietary teardown validation, and trade‑flow analytics. Key methodological elements:

- Patent and technical literature review to trace technology diffusion and identify proprietary design elements correlated with low‑deformation outcomes.

- Primary sourcing intelligence from anonymized OEM and laboratory interviews, supplier workshops, and equipment demo sessions to validate real‑world performance and procurement criteria.

- Physical BOM teardowns and lab trials to quantify component cost buckets and validate yield‑impact parameters under controlled conditions.

- Cross‑checking commercial data with customs and trade‑flow signals to detect inventory movements and supply‑side shifts not yet public in filings.

This multi‑vector approach allows PW Consulting to surface commercial signals that are not readily visible in public filings alone — we do not disclose proprietary interview records or teardown inputs here, but the report documents the calibrations and confidence intervals that translate to board‑level decisioning.

Strategic implications and recommended next steps for 2026

For executives finalizing 2026 allocations we recommend a three‑track approach:

- Defensive procurement: Lock critical consumables and secure multi‑source agreements for diamond wheels and specialised coolants to blunt near‑term price volatility.

- Targeted automation investments: Prioritize automation where yield improvements and labor substitution are demonstrable; use the report’s yield model to identify the top 10% of workflows where ROI breakeven occurs within 18 months.

- Partnerships over product: Pursue alliances with vendors that can supply integrated consumable, service, and analytics packages to accelerate Design Wins and reduce lifecycle TCO.

Operationally, teams should run three stress scenarios using the enclosed model templates in the report: baseline growth at the market CAGR (5.2%), an accelerated adoption case where automation penetration climbs quickly, and a downside case driven by disruptive material mixes or regulatory tightening.

PW Consulting’s Metallographic Cutting Machine Market report is designed to convert market intelligence into executable actions for 2026. For the full data tables, segmented distribution maps, vendor‑level scoring, and downloadable toolkits, Access the full report.

Contact PW Consulting to schedule a briefing and workshop that transforms the report’s toolkits into a bespoke action plan aligned with your 2026 capital and sourcing calendar.

For detailed analysis of this topic, please visit the official page: Metallographic Cutting Machine Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.