PW Consulting Forecast: Global Trash Compactors Market to Grow at a 4.5% CAGR from 2026 to 2032

Trash Compactors Market — Strategic Briefing for 2026 Capital Decisions

PW Consulting’s new Trash Compactors Market briefing synthesizes proprietary intelligence and open-source signals to equip boardrooms and investment committees for high-stakes allocation in 2026. The global market is now sized at USD 1,620.0 Million in 2025 and is projected to grow at a 4.5% CAGR through the 2026–2032 forecast window (reaching an estimated USD 2,110.0 Million by 2032). The 2026 baseline is USD 1,704.1 Million. These headline metrics mask structural shifts—supply-chain stresses, regulatory velocity, and an accelerating technology pivot—that make near-term decisions both urgent and consequential.

Trash Compactors Market

Executive snapshot: why 2026 is a pivot year

Executives should treat 2026 as a decision inflection point. Key forces compressing the investment timeline include:

- Raw-material inflation and trade friction that materially raise replacement and new-build unit economics.

- Procurement cycles shifting from CapEx-led refreshes to Opex-oriented service contracts and design-win lock-ins.

- Regulatory and ESG expectations that change procurement specifications and create new compliance costs and revenue opportunities.

- Technology adoption—sensorization, telematics, and AI-driven predictive maintenance—redefining total cost of ownership (TCO) and aftermarket margins.

Market trajectory and recent volatility

Between 2020 and 2025 the market expanded from USD 1,400.0 Million to USD 1,620.0 Million, a trajectory that reflects recovery from pandemic-era distortions and rolling infrastructure demand. The 4.5% CAGR projected for 2026–2032 represents steady expansion, but momentum is uneven across product forms and end uses; stakeholders should expect pockets of accelerated growth and intermittent softness driven by local policy changes and capital spending cycles.

Drivers shaping demand in 2026

Demand is being rewired by three interlocking trends:

- Service-led procurement: buyers increasingly evaluate compactors on lifecycle operating costs and serviceability rather than purchase price alone.

- Electrification and automation: electric and sensor-enabled systems are displacing manual units in high-density, high-frequency environments.

- Regulatory and ESG overlay: landfill diversion mandates and corporate sustainability targets prioritize compactors that deliver measurable volume reduction and energy efficiency.

Supply-chain pressure points

Steel is a dominant input for compactors. In early April 2026 U.S. hot-rolled coil (HRC) spot prices averaged approximately USD 1,040.0 per ton, up from roughly USD 905.0 per ton in the equivalent 2025 period, with global HRC trading near or above USD 1,000.0–1,118.0 per ton amid tariffs and mill disruptions. Elevated U.S. steel tariffs in 2026 sustain upward cost pressure. These dynamics create three tactical imperatives for procurement and product teams:

- Short-term: prioritize yield and nesting improvements in BOMs to defensively recover margin without eroding product durability.

- Medium-term: secure long-lead contracts and diversified mill sourcing to reduce spot exposure and pass-through volatility.

- Strategic: evaluate material substitution and modularization to reduce steel intensity where compliance and safety allow.

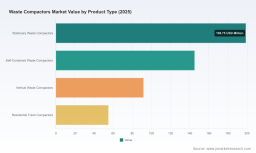

Segmentation nuance without the noise

The market remains bifurcated by product architecture and end-use. Electricization momentum is clear; larger commercial and institutional buyers are migrating to electrified and sensor-enabled platforms, while manual solutions retain relevance in lower-throughput settings. Regional demand centres are shifting, and the geographic balance of opportunity is changing; the full regional distribution and application-level splits are detailed in the full report’s distribution maps and heatmaps.

Competitive dimensions — what wins look like in 2026

Market concentration is moderate: CR3 is 28.5% and CR5 is 36.2%, indicating meaningful room for regional specialists and niche innovators. Across incumbents and challengers, design wins and share gains are being earned along distinct competitive vectors:

- Manufacturing scale and footprint — companies owning vertically integrated fabrication and regional service networks can shorten lead times and internalize steel cost pass-through.

- Aftermarket reach — firms with dense service coverage and spare parts velocity convert installations into annuity revenue and higher lifetime value.

- Design-for-service and modularity — product designs that simplify field servicing and parts replacement materially reduce TCO for large buyers and accelerate procurement preferences.

- Certification and compliance footholds — European and North American suppliers that pre-certify for municipal and institutional bid requirements win in tenders where compliance is a scoring criterion.

Applying these lenses to the listed incumbents illustrates differentiated moats without presuming future strategy. For example:

- Marathon Equipment Company: industrial-scale fabrication and a broad product portfolio that supports specification-led wins in commercial and municipal tenders.

- Wastequip LLC: multi-brand distribution and channel depth that underwrites national coverage and integrated waste handling solutions.

- Sebright Products Inc. and SP Industries Inc.: specialization in high-density and cart-handling equipment that caters to customers prioritizing volume reduction and custom fits.

- PTR Baler & Compactor and Orwak: strong heritage in baling and compaction for recycling-focused applications, with reputational strengths in European and North American institutional markets.

- Husmann, Gradeall, Capital Compactors, KENBAY: regional engineering advantages and export channels that serve specific geographies and compliance regimes.

These competitive insights underpin PW Consulting’s assessment of where margin pools will reallocate in 2026; for deeper company-level design-win factors and role-by-role supplier matrices, consult the full competitive chapter. Read the full findings here: Access the full PW Consulting Trash Compactors Market report .

Practical tools included in the report

PW Consulting’s report is intentionally operational. The deliverables that senior teams use to convert insight into action include:

- Supply-chain mapping that traces tier-1 and tier-2 suppliers, breakout of concentration risk, and alternative sourcing pathways.

- BOM decomposition logic and a manufacturability scorecard that isolates steel, hydraulics, control electronics, and sensor subsystems.

- Yield-adjustment and cost-recovery models that simulate tariff and spot-price scenarios and their P&L impact over three planning horizons.

- Technology roadmaps that align telematics, electrified drivetrains, and predictive-maintenance algorithms with procurement specifications and aftermarket monetization pathways.

- Commercial playbooks and RFP score templates designed to translate compliance and ESG criteria into procurement advantage.

These tools are configured to resolve 2026 pain points—rapid cost inflation, tightening bid compliance, and the need to capture recurring service revenue—without requiring clients to rebuild internal modeling capability from scratch.

Methodology — why our conclusions are robust

PW Consulting’s analysis is built on layered triangulation to reconcile public filings, field intelligence, and engineering verification. Core methodological pillars include patent-citation and standards-compliance analysis, structured OEM and supplier interviews under NDA, selective engineering teardowns and BOM-level validation, customs and shipment flow analysis, and anonymized channel checks with major buyers and maintenance providers.

We reconcile these inputs through statistical reconciliation and scenario-weighted modelling. Where direct disclosure is restricted, we infer structural relationships using cross-validated supplier invoices, bid documents, and observed design wins. This approach allows us to surface non-public cost dynamics and performance differentials while preserving client confidentiality and source integrity.

Implications and recommended next steps for 2026

Leaders should consider a focused playbook for 2026 that balances defensive and offensive moves. Immediate priorities include:

- Locking in critical steel supply via layered contracts and hedges to stabilize near-term margins.

- Prioritizing product re-designs that reduce steel intensity and increase modularity to improve field service economics.

- Accelerating telematics rollouts tied to aftermarket subscription models to capture TCO advantages.

- Aligning procurement RFPs with ESG metrics to capture premium bids from sustainability-motivated buyers.

- Targeted M&A or JV activity to shore up regional service networks where market share proves decisive.

Where to get the full intelligence

This briefing demonstrates the strategic value of PW Consulting’s Trash Compactors Market report for capital allocation and operational planning in 2026. For the comprehensive regional breakdowns, product-level economics, and executable sourcing models—each with downloadable worksheets and supplier contact maps—access the full report at: https://pmarketresearch.com/worldwide-waste-compactors-market-research .

For detailed analysis of this topic, please visit the official page: Trash Compactors Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.