PW Consulting: Commercial Tumble Dryers Market to Expand at 5.0% CAGR Through 2032, Fueled by Rising Demand for Electric Models

Commercial Tumble Dryers Market — Strategic Outlook for 2026

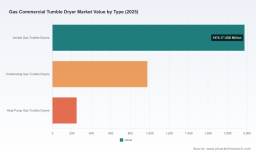

PW Consulting publishes a focused industry briefing derived from our full Commercial Tumble Dryers Market report (base year 2025). This preview synthesizes the high‑level trends and decision levers that matter to C‑suite leaders and capital allocators in 2026, demonstrating why immediate strategic action is required. The global market is evolving predictably yet unevenly: total revenues stand at 1,000.0 Million USD in 2025 and grow at a compound annual growth rate (CAGR) of 5.0% through our forecast window, reaching 1,407.1 Million USD by 2032. The market concentration is material (CR3 ≈ 55.0%, CR5 ≈ 70.0%), which shapes supplier bargaining power, design‑win dynamics and merger & acquisition appetites.

Commercial Tumble Dryers Market

Executive snapshot — what the numbers imply for strategy

High‑level metrics mask important structural shifts. The 5.0% CAGR reflects steady demand across commercial segments, but the pace and risk profile of returns vary by end‑use, fuel exposure and regulatory environments. In aggregate, the market exhibits mature replacement cycles in hospitality and on‑premise laundry, while pockets of incremental demand continue in healthcare and selected industrial applications. For investors and operators, the headline growth supports disciplined organic investment, but execution must be informed by localized fuel economics, service network density and regulatory compliance costs.

Why 2026 is a pivotal year for capital allocation

Several concurrent forces make 2026 a moment for decisive capital redeployment rather than passive portfolio maintenance:

- Energy cost volatility: Natural gas price trajectories and supplier contract structures materially affect operating cost models for gas‑heated equipment. Operators that lock in supply or hedge exposure will materially change lifecycle economics.

- Regulatory and rebate opportunities: Efficiency retrofit programs (for example, two‑stage modulating gas valve kits qualifying for utility rebates) change the simple payback math for upgrades versus full replacement; timing is critical to capture available incentives.

- Service and reliability risk: Recent field service notices (for example, a manufacturer recall/repair campaign to correct improperly torqued bolts on certain models) highlight the tangible commercial impact of warranty events on brand trust and operating uptime.

- Market concentration: With the top three suppliers controlling a majority share, design‑win competition is increasingly about non‑price levers (controls, connectivity, aftermarket response) rather than commoditized hardware.

What PW Consulting’s report delivers (practical tools, not just charts)

Our full report is structured to turn strategic hypotheses into executable plans. Key deliverables include:

- Supply chain map that traces component sourcing for heating systems, blowers and control electronics — enabling procurement teams to prioritize dual‑sourcing and negotiate lead‑time protections.

- Bill‑of‑Materials (BOM) decomposition logic and cost sensitivity models — designed so engineers and procurement can simulate raw material and commodity price shocks without re‑engineering the entire cost model.

- Yield adjustment and manufacturing throughput models that translate small quality improvements into margin recovery and CapEx deferment opportunities.

- Technology roadmaps that sequence efficient upgrades (e.g., modulating gas valves, variable airflow systems, and heat‑pump iterations) against regulatory milestones and rebate windows.

- Compliance and TCO matrices that link regional trade rules, emissions constraints and utility program eligibility to lifecycle cost outcomes.

Each tool is delivered as a decision‑grade template rather than prescriptive parameters — so teams can inject proprietary vendor quotes, contract terms and local utility tariffs to obtain board‑level scenario outputs for 2026 capital planning.

Competitive landscape — the dimensions that determine winners in 2026

Our analysis of incumbent manufacturers focuses on competitive dimensions rather than projecting individual 2026 plays. The marketplace is shaped by several enduring moats and tactical advantages:

- Installed base and aftermarket reach: Firms with dense field service networks convert product reliability into recurring revenue and preferential specification in large O&M contracts.

- Controls and integration: Companies that pair mechanical platforms with advanced control suites (residual moisture algorithms, IoT telematics, energy‑aware sequencing) win design slots where TCO matters most.

- Manufacturing scale and modularization: Producers with modular platforms achieve SKU rationalization and faster new‑model ramp at lower engineering cost.

- Regulatory and rebate competence: Vendors that qualify products for utility rebate programs or certify retrofit kits secure procurement advantage in rebate‑driven procurements.

- Quality assurance and field response: Warranty and corrective actions (as seen in recent service bulletins) directly influence specification committees and insurance underwriting terms for large institutional buyers.

Design wins in 2026 hinge less on headline efficiency numbers and more on a combination of system compatibility, retrofit pathways, consistent firmware/service updates, and demonstrable service metrics. To explore our deeper competitor scorecards and the OEM risk matrix, click here: Full Commercial Tumble Dryers Market Report .

Technology pathways and regulatory vectors to watch

From a technology adoption standpoint, three migration tracks coexist in 2026:

- Incremental gas‑system efficiencies (e.g., modulating valves, improved airflow management) that lower operating cost without major capital outlay and often qualify for incentives.

- Hybridization and electrification, including heat‑pump systems, which reduce fuel exposure but require higher upfront capital and different maintenance capabilities.

- Digitalization — connectivity, predictive maintenance and energy‑aware scheduling — which compress lifecycle costs and create aftermarket differentiation.

Regulatory movement on energy intensity and emissions is accelerating localized compliance costs and enabling new rebate structures. For procurement teams, assessing the trade‑offs between upfront CapEx and projected fuel/O&M exposures across these pathways is now a standard boardroom exercise.

Actionable implications for 2026 decision‑makers

Leaders should translate the high‑level market view into three pragmatic actions this year:

- Prioritize retrofitability and modular upgrades in procurement clauses to preserve access to utility rebates and reduce total replacement cycles.

- Stress‑test vendor commitments: require service KPIs, firmware update cadences, and spare‑parts lead‑time guarantees in long‑term agreements.

- Run rapid BOM and yield stress scenarios with supplier quotes to identify margin recovery levers and CapEx deferment opportunities ahead of planned tenders.

These actions protect operating margins while maintaining optionality for full platform transitions as electrification economics improve.

Methodology — why our conclusions are decision‑grade

PW Consulting’s findings are grounded in a layered triangulation methodology that combines quantitative and qualitative sources to reduce single‑source bias. Key elements include patent citation analysis to detect feature diffusion, multi‑tier supplier interviews to validate lead‑time and input price moves, on‑site BOM tear‑downs to measure architecture commonality, and dealer/installer panels to quantify field service incidence. We then reconcile these inputs against public financials and utility rebate program filings to form probabilistic scenarios that are robust to contestable assumptions.

Where we rely on non‑public inputs (for example, OEM service records or proprietary installer tickets), our team secures data via NDAs and uses aggregate anonymization to preserve supplier confidentiality while producing actionable insights. This permits clients to see realistic risk ranges and supplier scorecards rather than optimistic supplier claims.

Next steps — how to use this preview

This briefing is a deliberate preview: it surfaces the patterns, competitive dimensions and practical tools that will determine who captures superior returns through 2026. For procurement directors, product heads and private equity sponsors ready to move from diagnosis to action, our full report provides the granular regional distribution maps, supplier‑level scorecards and editable CapEx/Opex models needed to finalize 2026 budgets and tender specifications. Access the complete report here: Full Commercial Tumble Dryers Market Report .

For detailed analysis of this topic, please visit the official page: Commercial Tumble Dryers Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.