PW Consulting Forecasts 8.2% CAGR for External ODD Market Through 2032, Fueled by Portable Segment

External SSDs in 2026: Strategic Imperatives from PW Consulting’s External ODD Market Report

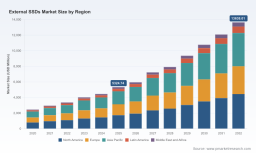

PW Consulting releases its 2026 External ODD Market (External SSDs) briefing, synthesizing five years of historical tracing (2020–2025) and a detailed 2026–2032 forecast horizon. The market we track has grown from USD 150.0 Million in 2020 to USD 190.0 Million in 2025 and is modeled to reach USD 328.0 Million by 2032, representing a 8.2% compound annual growth rate (CAGR) across the forecast period. This briefing explains why the dataset and tools in our full report are immediately consequential to capital-allocation, sourcing, and product-strategy decisions taken in 2026.

Why 2026 Is a Strategic Inflection Point

Clients are confronting a conjunction of supply-side scarcity and demand-side sophistication that forces near-term trade-offs: protect margin or chase feature parity. The macro picture in 2026 is dominated by constrained NAND availability, pronounced wafer-price volatility, and entrenched advance-booking of capacity. These dynamics compress negotiating windows and increase the premium on procurement intelligence and yield-optimizing product design.

-

Supply scarcity: Several tier‑one NAND vendors report near-full production bookings for 2026, creating a lead‑time and allocation regime that favors long-term agreements.

-

Price inflation: Upstream wafer pricing has moved sharply since early 2025, materially increasing component cost pressure across the portable storage stack.

-

Short‑term volatility: NAND module prices show continued month‑to‑month movement in early 2026, forcing procurement teams into dynamic hedging and tiered contracting strategies.

-

Financial strain on suppliers: Public remarks from controller and NAND ecosystem leaders signal advanced payment terms and higher working‑capital demands for certain foundry relationships.

Practical Strategic Implications for 2026 Decisions

Boardrooms and procurement chiefs must convert the macro signal into precise actions. Our research indicates five priority domains where 2026 decisions will determine competitive position in 2027–2028.

-

Supply-resilience and contracting: Shift from single‑sourcing to staged commitments with staggered prepayment schedules and performance-based volume guarantees.

-

Cost-to-feature trade-offs: Use BOM-level scenario modeling to identify which performance attributes deliver incremental ASPs that materially offset NAND inflation.

-

Design-win acceleration: Prioritize controller/vendor co‑engineering and OEM certification paths that shorten qualification cycles in a tight capacity environment.

-

ESG and compliance risk mitigation: Integrate regulatory due diligence into supplier selection to avoid retroactive exposure as trade compliance regimes tighten.

-

Portfolio rationalization: Re-assess low-margin SKU proliferation and focus R&D investments on modular architectures that can be re‑binned for multiple channels.

What the Full Report Provides (Operational Toolset)

PW Consulting’s full External ODD Market report goes beyond high-level narrative: it supplies actionable, model-driven artifacts executives use in negotiation and product planning. Key deliverables include:

-

Supply chain topology and counterparty risk maps showing second‑order dependencies and alternative sourcing lanes.

-

Reverse BOM decomposition logic with margin sensitivity layers—designed to help finance and product teams test pricing scenarios without exposing our proprietary assumptions here.

-

Yield and yield‑improvement adjustment models to quantify the P&L impact of controller firmware changes, packaging yields, and NAND binning strategies.

-

Technology roadmaps that align interface evolution (USB4/Thunderbolt generations) with controller availability and NAND roadmap timing.

-

Commercial playbooks for OEM design wins, retail channel segmentation, and enterprise procurement including template negotiation clauses that address capacity booking and force majeure in 2026 contexts.

These tools are intentionally prescriptive in form but abstracted in public commentary: the report demonstrates how each tool resolves a 2026 pain point (e.g., margin recovery under rising wafer prices, compliance screening for new overseas suppliers) while withholding proprietary parameterizations to preserve client value and drive controlled access. For the complete dataset and distribution maps, please visit Access the full report .

Competitive Landscape: Dimensions of Advantage

The External SSDs market in 2026 exhibits concentrated leadership with a CR3 of 52.0% and a CR5 of 68.0%, signaling that a handful of incumbents control meaningful channel leverage. Our analysis does not publish forward-looking revenue shares here; instead we characterize the axes on which competitors compete and the capabilities that define durable advantage.

-

Vertical integration and supply security: Firms with upstream NAND affiliations or captive production channels exhibit lower exposure to spot-price shocks and earlier access to new NAND nodes—this is a structural moat for product continuity.

-

Controller and firmware co‑design: Design wins are increasingly awarded to suppliers who can demonstrate co‑optimized firmware/controller stacks that unlock sustained sequential throughput and thermal profiles for next‑gen interfaces.

-

Brand trust and channel breadth: Established consumer brands preserve premium ASPs through retail distribution and B2B partnerships; this matters in a market where premium portable products command margin premiums during supply scarcity.

-

Specialist positioning: Providers focused on ruggedization, creative professional workflows, or platform-aligned ecosystems (e.g., Mac optimization) secure niche defensibility and higher attach rates for accessory and service bundles.

-

Cost‑leadership via ODM relationships: Vendors who master low-cost BOMs and yield optimization retain flexibility to contest value segments where OEMs trade performance for price.

Examples from the field illustrate these dimensions without disclosing our full strategic read: companies that combine NAND access with strong controller partnerships win quicker qualification with enterprise buyers; firms that emphasize ruggedized UX and certified workflows win creative-professional share. For detailed vendor matrices and scenario-aligned design-win checklists, see Download the full report .

Recent Product and Supply Signals (Contextual Evidence)

Market participants are already responding tactically. Early 2026 product announcements and supply-side statements validate the directional assumptions in our models:

-

Tier‑one consumer portfolios are advancing USB4 and high‑capacity propositions to capture high‑value professional workflows.

-

Several vendors are rebranding and consolidating SKU architectures to streamline channel messaging and reduce SKU proliferation during component constrained periods.

-

Industry commentary indicates wafer and module price escalation and prepayment terms for high-demand NAND, underscoring the liquidity and working‑capital implications of 2026 supply contracts.

Methodology: How PW Consulting Builds Confidence

Our 2026 external SSD market estimates rest on a Layered Triangulation methodology that combines primary conversations, transaction-level data, and technical reverse analysis. We cross-reference four information planes to reduce bias and expose asymmetric insights:

-

Primary intelligence: Confidential interviews with OEM purchasing leads, contract manufacturers, and selected component suppliers performed under NDAs, enabling visibility into allocation terms and lead‑time commitments.

-

Trade and shipment analytics: Customs and freight‑flow datasets aggregated at SKU level, reconciled with channel scanner data to calibrate regional demand trends and inventory turns.

-

Engineering reverse-analysis: Physical unit teardown, firmware metadata extraction, and BOM cost modeling that reveal controller/NAND pairings and enable robust yield sensitivity testing.

-

Patent and supplier network analysis: Citation mapping and supplier linkage graphs that uncover where design IP and component sourcing reveal persistent competitive moats.

These layers are reconciled through iterative validation loops and statistical back‑testing against historical shipments (2020–2025 base window). Our approach explains not only what happened, but the plausible operational mechanics driving supplier behavior—vital for negotiating contracts or sizing inventories in 2026.

Immediate Recommendations for 2026 Executives

Based on our synthesis, boards and operating committees should treat 2026 as a year to rewire choice architecture around supply predictability and profitable feature differentiation:

-

Re-prioritize supplier conversations around capacity and flexibility clauses rather than solely lowest-bid economics.

-

Invest in firmware/controller co‑development that yields marginal performance gains and shortened qualification cycles.

-

Rebalance portfolios toward modular SKUs that can be rebinned in response to NAND node availability, protecting ASP floor while preserving market coverage.

-

Embed trade- and ESG‑compliance checks into procurement scorecards to avoid downstream remediation costs as cross-border rules harden.

PW Consulting’s full External ODD Market report provides the working models, supplier matrices, and negotiation playbooks necessary to operationalize these recommendations. To access the complete analysis, interactive charts, and vendor playbooks, visit Access the full report .

Closing Note

2026 is not a year for passive monitoring; it is a year for structural repositioning. With NAND dynamics still trending toward constrained supply and continued pricing volatility, decision-makers who combine rigorous supply intelligence with targeted product and contract design will both defend margin and capture disproportionate share as capacity normalizes. PW Consulting’s External ODD Market report converts that imperative into a set of executable artifacts tailored for procurement, product, and corporate strategy teams.

For detailed analysis of this topic, please visit the official page: External ODD Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.