PW Consulting: Cardiopulmonary Autotransfusion System Market Set to Reach USD 742.1 Million by 2032

Cardiopulmonary Autotransfusion System Market — Strategic Briefing for 2026

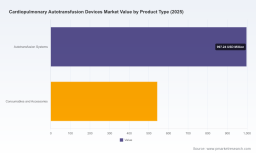

PW Consulting’s latest market research positions the worldwide cardiopulmonary autotransfusion system market at USD 483.1 Million (base year 2025), with a clear trajectory toward USD 742.1 Million by 2032 — representing a compound annual growth rate (CAGR) of 6.5% across the 2026–2032 forecast window. For executives making capital-allocation and product-strategy decisions in 2026, this market presents both predictable volume growth and materially shifting competitive dynamics driven by clinical evidence, regulatory clarity, and manufacturing economics.

Cardiopulmonary Autotransfusion System Market

Why 2026 Is a Pivotal Year

Four converging forces make 2026 the strategic inflection point for players across the value chain:

- Clinical validation is accelerating. Recent head-to-head and device‑specific clinical studies are refining buyer criteria from “device capability” toward “demonstrated patient‑level outcomes and processed blood quality.”

- Regulatory and reimbursement clarity is consolidating procurement frameworks, tightening the feedback loop between clinical evidence and adoption at scale.

- Manufacturing and supply‑chain pressure is increasing unit-cost sensitivity: disposable spend, component shortages, and sterilization capacity are central to hospital total cost of ownership (TCO) discussions.

- Technology differentiation is moving beyond raw performance to systems thinking — integration with perfusion platforms, software-assisted workflows, and data capture for quality and compliance.

Market Dynamics — What’s Driving Growth

The market growth we forecast is not uniform; it is being driven by specific demand and supply-side mechanisms that matter for strategic planning:

- Elective and emergent cardiac and trauma surgical volumes remain the primary demand engine, with incremental adoption coming from higher‑risk orthopedic and hybrid procedures.

- Device form factor innovation (continuous systems vs. bowl-based systems) is re-prioritizing procurement decisions based on throughput, hematocrit performance, and perfusionist workload.

- Regulatory clarity (device classification and 510(k) pathways) and evolving reimbursement codes are compressing time-to-adoption for clinically proven devices.

- Hospital procurement is shifting to lifecycle cost models, forcing suppliers to defend price while demonstrating operational savings through disposables management and reduced allogeneic transfusions.

What the Report Contains — Practical, Actionable Tools

PW Consulting’s report is built as a practitioner’s toolkit for 2026 decision-makers. Rather than a superficial market overview, the deliverable includes operational and financial models designed to be executable by commercial, R&D, and supply-chain teams.

- Supply‑chain map: a tiered supplier ecosystem with critical‑path components, concentration risk scoring, and alternative‑sourcing options to support dual‑sourcing decisions.

- BOM (Bill‑of‑Materials) deconstruction logic: a reproducible framework for estimating cost-in‑use and candidate cost-reduction levers without disclosing client-sensitive unit price data.

- Yield and throughput adjustment models: sensitivity matrices showing how small changes in yield, sterilization turnaround, or disposables usage impact hospital TCO and supplier margin.

- Technical roadmap and IP landscape: a synthesis of patent clusters, emergent technical themes (e.g., platelet recovery, dynamic cell salvage), and likely R&D trajectories through 2030.

- Regulatory and reimbursement matrix: mapping of device classifications, key predicate filings, and reimbursement pathways that influence rollout velocity.

- Commercial playbooks: procurement win strategies, service footprint planning, disposable contract archetypes, and clinical evidence sequencing to secure design wins.

Each tool is accompanied by scenario-driven use cases that show how procurement teams, product leaders, and private equity sponsors can translate analysis into 12–24 month operational plans without exposing proprietary pricing or customer lists.

Competitive Landscape — Dimensions That Win Design Wars

Our competitive analysis focuses on strategic dimensions that determine long-term advantage rather than short-term market share snapshots. Key dimensions include technological moat, system integration, clinical evidence, service and training footprint, disposable economics, and regulatory timing.

- Integration and Systems Moat — Companies that offer or tightly integrate autotransfusion solutions with cardiopulmonary bypass and perfusion platforms can lock workflows and reduce churn by embedding into perfusionist routines.

- Technology Differentiation — Continuous autotransfusion designs and dynamic cell salvage variants present distinct clinical and operational value propositions that influence buyer preference in high-throughput centers.

- Clinical Evidence and KOL Influence — Design wins at major cardiac centers are heavily influenced by prospective studies and peer-reviewed outcomes that demonstrate RBC recovery, platelet function preservation, and reduced allogeneic transfusion.

- Software and User Experience — Devices that reduce operator complexity and training burden via intelligent control software tend to shorten procurement cycles and lower labor-related objections.

- Service and Disposable Economics — The economics of disposables, sterilization, and field service are often decisive in tender outcomes; suppliers that manage this total cost can achieve premium positioning.

Examples drawn from the field include incumbent platforms that leverage integration with perfusion equipment to create workflow lock-in; vendors differentiating on next‑generation features that preserve platelet function; and firms that have deployed software releases to simplify clinical operation. Recent discrete developments — such as comparative clinical studies between leading devices and regulatory clearances for updated disposables or software modules — are actively reshaping purchase algorithms in hospitals.

To explore the full company-by-company analysis and the underlying evidence base that supports our competitive scoring, see the full report: Access the PW Consulting market report .

Priority Actions for Investors and OEMs in 2026

For organizations allocating capital or revising product roadmaps in 2026, we recommend a focused set of priorities that balance near-term containment with mid-term differentiation:

- Prioritize modular disposables cost initiatives and supplier diversification in Q1–Q2 2026 to protect margins against sterilization and material price shocks.

- Accelerate clinical evidence generation where product differentiation is claimed; prospective cohort data and device comparators materially speed procurement approvals.

- Embed software and data-capture features to convert device interactions into compliance and quality narratives that hospitals can use for internal justification.

- Pursue targeted tuck‑in M&A for component suppliers with production capacity or unique consumable designs to control the disposable cost base.

- Design procurement offers that align with evolving reimbursement and value-based care models, emphasizing measurable reductions in allogeneic transfusion and OR time.

Methodology — How PW Consulting Produces Actionable Truth

Our 2026 market forecast and analysis rest on a multi-layered, reproducible methodology we describe as Layered Triangulation. The approach combines patent and regulatory‑filing analytics, controlled BOM teardown exercises, anonymized hospital procurement datasets, and primary interviews with perfusionists, OR managers, and procurement directors. We complement primary data with device bench testing and sterilization throughput assessments performed in certified labs.

To validate and enrich non-public inputs, we convene expert panels and utilize anonymized purchase-order streams provided under NDA from hospital networks and distributor partners. This enables us to reconcile list prices with realized transaction economics and to identify structural supply constraints that public filings alone do not reveal. Our methodology is auditable and repeatable for clients conducting diligence or preparing for regulatory submissions.

Regulatory, Reimbursement and ESG Considerations

In 2026, compliance and reimbursement mechanics are not peripheral — they are central to market access. Device-classification clarity is enabling faster adoption for cleared systems, and explicit reimbursement mapping reduces procurement latency. Simultaneously, hospital systems are applying ESG lenses to supplier selection, favoring partners with transparent supply chains, reduced single-use waste, or credible recycling pathways. These vectors materially influence procurement outcomes and should be embedded into product development and commercial engagement plans.

Next Steps — How to Use This Intelligence

PW Consulting’s report is designed to be executable by senior commercial and technology leaders who must make decisive moves in 2026. If you require a tailored executive briefing, supply‑chain deep dive, or acquisition screen using our proprietary scoring algorithms, PW Consulting can deploy a compact engagement to deliver prioritized action items within 4–6 weeks.

For full access to the dataset, scenario models, and company-level evidence that underpin our conclusions, download the report here: Download the PW Consulting market report .

In a market growing from USD 483.1 Million in 2025 toward USD 742.1 Million by 2032 at a 6.5% CAGR, the difference between capturing share and lagging lies in three capabilities: converting clinical evidence into procurement wins, securing disposable economics, and orchestrating regulatory and reimbursement pathways. PW Consulting’s toolkit converts these capabilities from abstract imperatives into executable plans for 2026.

For detailed analysis of this topic, please visit the official page: Cardiopulmonary Autotransfusion System Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.