PW Consulting: PV Ribbon Market Poised for 7.3% CAGR Through 2032

PV Ribbon Market: Strategic Imperatives for Corporate Decision-Making in 2026

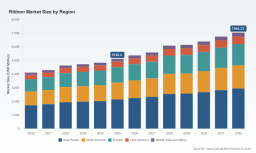

The PV Ribbon market is entering a decisive growth phase in 2026. PW Consulting’s latest market model shows the industry expanding from a 2025 base of USD 1,079.0 Million to an estimated USD 1,767.0 Million by 2032, driven by a compound annual growth rate (CAGR) of 7.3% over the 2026–2032 forecast window. These headline figures understate a more complex reality: shifting raw-material flows, emerging regulatory constraints, and concentration dynamics that together create both acute risks and actionable opportunities for investors, procurement heads, and product teams.

PV Ribbon Market

Why This Matters Now

Executives allocating capital or redesigning supply chains in 2026 must treat the PV Ribbon market as both growth platform and risk zone. Several structural forces make immediate, informed action prudent:

- Accelerating demand vector: The market trajectory from 2020 to 2025 establishes a steeper growth baseline entering our forecast; 2026 is the first planning year where many capital projects begun in 2024–2025 need results.

- Material and input volatility: Polymer, wax, and resin price swings continue to impair margin stability—an issue heightened in thermal-transfer segments.

- Regulatory and trade pressure: Active administrative reviews and trade measures related to narrow woven ribbons create compliance exposures for global sourcing strategies.

- Concentration and supplier economics: The market displays measurable concentration (CR3 39.0%, CR5 45.0%), which affects negotiating leverage, design-win dynamics, and M&A opportunities.

What PW Consulting’s PV Ribbon Market Report Delivers

Our report is designed as an executable intelligence packet for 2026 decision cycles. It moves beyond descriptive sizing and provides practitioners with decision-grade tools that can be applied to procurement, product development, and M&A diligence without requiring technical rediscovery on the shop floor.

- Supply chain map with node-level risk scoring (upstream polymer sources, processing, finishing, and logistics corridors).

- Bill-of-Materials (BOM) decomposition templates that identify the top cost levers by SKU and production route.

- Yield-adjustment models that translate incremental process improvements into EBITDA uplift under multiple price scenarios.

- Technology roadmap that aligns weaving, coating, and thermal-transfer chemistry timelines with supplier capability curves.

- Compliance matrix linking product families to certification and trade-risk gates (e.g., quality standards and anti-dumping/countervailing review touchpoints).

Each tool is accompanied by practical playbooks—procurement negotiation scripts, pilot design checklists, and KPI dashboards—so teams can convert insight into 90–180 day pilots and measurable cost outcomes in 2026.

Competitive Landscape: Dimensions that Decide Design Wins

Our 2026 analysis frames competition across capability vectors rather than offering point forecasts for each firm. This framing helps clients identify where to allocate resources to win in RFPs, new product launches, and retailer qualification processes.

- Scale and throughput: Volume producers command cost advantages in standard decorative and industrial ribbon SKUs; scale also rationalizes investment in automation and inventory buffering.

- Customization and speed-to-sample: Firms that pair broad color/material libraries with rapid prototyping infrastructure secure design wins in premium packaging and bespoke luxury segments.

- Quality and compliance credentials: ISO 9001 and OEKO‑TEX style certifications act as gatekeepers for many multinational buyers; certification footprints matter more than ever in 2026 procurement decisions.

- Materials science and performance fibers: Producers able to work with high-performance yarns (e.g., Kevlar, Nomex) or engineered polymer blends differentiate for industrial and safety-critical applications.

- Vertical integration and supply partnerships: Control over key upstream inputs or exclusive recycling feedstock agreements can compress cost volatility and improve gross margins.

- Channel relationships and brand trust: Longstanding partnerships with retailers, floral distributors, and OEMs translate into preferred-supplier status for new SKUs and seasonal volume commitments.

Representative actors in the competitive set illustrate these dimensions. For example, US-based Berwick Offray is notable for large-volume decorative production and retail channel depth; several Taiwan and China-based manufacturers provide high-mix customization and OEM services; specialist mills in Europe and the US focus on performance webs and technical tapes. PW Consulting’s client-facing profiles synthesize these positional strengths and point to the single most important tactical lever for each company type—without disclosing our proprietary 2026 scenario outcomes.

Access the full PV Ribbon Market report for granular competitor matrices and interactive capability maps that explain who wins in which buying contexts and why.

Technology and Materials Evolution in 2026

Material dynamics are fundamentally reshaping cost and product strategy entering 2026. Global polyester fiber production increased notably in recent years, and recycled polyester availability is growing—yet recycled share dynamics and feedstock economics present hybrid opportunities rather than turnkey solutions. Thermal-transfer ribbon producers face input-price noise across polymers, waxes, and resins, which amplifies the value of BOM-level hedging and supplier scorecards.

- Recycled-content adoption: Supply availability and certification requirements (chemical safety and traceability) are now procurement gates for multinational buyers.

- Performance fibers: Demand in industrial and safety segments compels investments in narrow-woven capability and post-processing that meet higher thermal and tensile specifications.

- Automation and AI: Machine learning is being applied to width control, thread-count optimization, and inline quality inspection—yield models in our report quantify the ROI of incremental automation investments.

- Color and surface finishing: Digital color-matching and lower-changeover finishing lines reduce time-to-market for seasonal runs, a decisive advantage for design-driven buyers.

Methodology and Research Rigor

PW Consulting applies a layered triangulation methodology to ensure the market picture is both comprehensive and verifiable. Our approach combines patent and technical literature mapping, customs and trade-flow analytics, confidential primary interviews under NDA, BOM reverse engineering, and on-site production audits where access is available. We then reconcile these primary inputs with supply-side reporting and macro material production statistics to produce a consistent time series.

Key methodological elements include:

- Patent and standards tracking to identify emergent process and material innovations before they scale commercially.

- Customs-derived shipment flows and transactional price points to backfill regions and routes that lack transparent reporting.

- Confidential supplier and buyer interviews (procurement directors, plant managers, R&D leads) to clarify lead-time structures, minimum-order economics, and compliance practices.

- Quantitative modeling layers—BOM cost trees, yield sensitivity scenarios, and capex payback simulations—used to stress-test strategies across volatility regimes.

We do not publish raw confidential interview content; instead we extract calibrated parameters that feed our models and sector mosaics—this is how we derive the 2020–2032 time series and the 7.3% CAGR cited above.

Strategic Recommendations for 2026 Executives

Based on our analysis, boards and executive teams should prioritize three near-term moves to convert growth into durable value:

- Build a compliance-first sourcing playbook: map tariff and anti-dumping exposure for critical SKUs and realign preferred supplier lists to reduce discretionary risk.

- Invest selectively in yield and BOM optimization pilots: small-capex pilots that focus on finishing-line yields and adhesive/film substitutions unlock outsized margin improvement.

- Lock strategic partnerships upstream: secure recycled-polyester feedstock or exclusive polymer allocations to stabilize input cost and support ESG commitments.

- Accelerate design-to-production velocity: shorten sampling cycles through digital color libraries and co-located prototyping to win retailer design slots.

- Evaluate inorganic moves where justified by consolidation economics: given current concentration metrics, targeted tuck-ins can expand capacity and capability rapidly.

How to Obtain the Complete Intelligence Pack

PW Consulting’s full PV Ribbon Market report contains the complete regional and application splits, interactive revenue maps, company-level scenario matrices, and the operational playbooks referenced above. For corporate teams building 2026 budgets, this report provides the missing link between strategy and execution. Access the full dataset and interactive charts here: Access the full PV Ribbon Market report .

For detailed analysis of this topic, please visit the official page: PV Ribbon Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.