PW Consulting: Dithiocarbamate Fungicides Market Poised for 2.5% CAGR Growth as Agricultural Demand Fuels Expansion

PW Consulting Strategic Brief — Dithiocarbamate Fungicides Market (2026): A Decision-Maker’s Preview

PW Consulting publishes a focused industry briefing to equip senior executives with the strategic vantage they need in 2026. This note previews our comprehensive Market Research on Dithiocarbamate Fungicides, highlighting why the next 12–24 months are decisive for capital allocation, regulatory positioning, and manufacturing upgrade plans. The full study includes proprietary schedules, scenario models and distribution maps; this briefing demonstrates the analytical depth while preserving the report’s core segmentation and company-level forecasts for subscribers.

Dithiocarbamate Fungicides Market

Market Snapshot (High-Level)

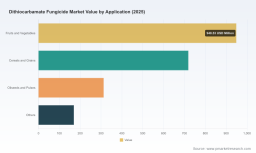

The dithiocarbamate fungicides market is recovering from recent volatility and entering a steady-growth phase. In nominal terms, global industry revenue moved from USD 773.4 Million in 2020 to USD 875.0 Million in our base year 2025, and our layered models project a return to expansion through the 2026–2032 forecast window, reaching roughly USD 1,047.3 Million by 2032. The forecast period CAGR is 2.5% (2026–2032), reflecting a market that is mature, supply-sensitive, and highly influenced by regulatory action and raw-material cycles.

Market concentration is meaningful but not monopolistic: the top three players account for roughly 52.0% of supply, while the top five reach about 56.0%. That structure creates both defensible incumbency and tactical openings for challengers with differentiated advantages.

2026 Dynamics That Drive Strategic Urgency

- Raw-material cost shocks: Carbon disulfide price volatility continues to transmit sharply to producer margins. Recent price moves underline the immediate need for hedging or sourcing redesigns.

- Regulatory redefinition: The European Commission’s 2025 draft on residue definitions (expressed as CS2) and rolling approval expiries have changed compliance baselines, creating asymmetric risks across portfolios and geographies.

- Compliance testing capacity: New commercial offerings for residue testing (e.g., Headspace GC-MS services launched in 2025) are shifting the economics of market access and customer acceptance, particularly in sensitive export corridors.

- Production geography: Supply is concentrated in established hubs that are facing both environmental scrutiny and rising input costs—accelerating decisions on nearshoring, tolling partnerships, or vertical integration.

Strategic Implications for 2026 Capital Allocation

For executive teams considering CAPEX, M&A, or reallocation of working capital in 2026, the following high-level implications emerge from our analysis:

- Protect margins through upstream options: Given feedstock cost volatility, options such as secured tolling agreements, strategic feedstock contracts, or minority stakes in carbon disulfide producers materially alter outcome distributions in our yield-sensitivity models.

- Regulatory arbitrage and registration portfolios: Changes in residue definitions and rolling approvals make registration portfolios a primary determinant of revenue continuity. Investment in dossier maintenance and targeted re-registration programs is frequently more value-accretive than greenfield capacity.

- Compliance-as-a-service: Partnering with accredited testing labs and embedding third-party residue verification into customer value propositions shortens sales cycles in regulated markets.

- Manufacturing modernization: AI-assisted yield optimization and digital process control deliver payback within planning horizons when combined with focused BOM rationalization and product-line pruning.

What Our Operational Toolkit Delivers (Practical, Not Prescriptive)

The full PW Consulting study contains practical tools designed for 2026 operational choices. Representative modules include:

- Supply-chain footprint and risk heatmap, identifying single points of failure and alternative routing logic.

- BOM decomposition and cost-to-serve templates, enabling rapid what-if analysis on feedstock shocks and freight disruption.

- Yield adjustment and scenario models that convert small percentage-point yield improvements into P&L impact under realistic price regimes.

- Technology and formulation roadmaps aligned to regulatory trajectories, showing investment timing and likely technology-adoption windows.

- Contracting levers and commercial terms library for tolling, take-or-pay, and flexible offtake structures.

Each tool is implemented as a decision-grade workbook or map rather than a one-size-fits-all prescription. The workbooks illustrate how to translate a regulatory or price shock into contractual and operational responses, without publishing the sensitive parameter values that we reserve for report subscribers.

Competitive Dimensions — What Wins and What Fails in 2026

Our competitive analysis focuses on the dimensions that determine long-term advantage rather than on single-year revenue forecasts. Across leading participants (incumbent producers, specialty formulators and large crop-protection houses), winning requires a combination of the following defensible attributes:

- Regulatory moat: breadth and currency of registration dossiers across jurisdictions; speed of re-submission; local data packages.

- Scale and cost position: contiguous manufacturing capacity, low-cost feedstock access and operational scale that absorbs price swings.

- Channel and service play: agronomy support, residue compliance guarantees, and localized technical service that translate into design wins with distributors and large growers.

- Product quality and formulation expertise: consistent batch quality, low-residue formulations, and compatibility with integrated pest management (IPM) programs.

- Strategic flexibility: capacity to pivot between technical grade supply, formulation, and contract manufacturing—often enabled by multi-site manufacturing footprints.

Examples of how these dimensions play out: global players with diversified crop-protection portfolios can offset regulatory losses in one molecule through portfolio repositioning, while regional producers with tight cost structures often compete successfully on price and service in domestic markets. Chinese manufacturers are notable for manufacturing scale; specialty formulators excel on downstream service; integrated crop-protection companies compete on distribution and bundled agronomy.

For practitioners seeking a closer view of these competitive trade-offs and company-level capabilities, see our detailed competitive matrix and supplier scorecards (download the full study here: PW Consulting Worldwide Dithiocarbamate Fungicide Market Research ).

Methodology — How We Derived Actionable, Non-Public Insights

PW Consulting’s conclusions rest on multilayered triangulation and validated proprietary inputs. Our approach combines:

- Primary interviews with procurement, regulatory, and plant operations managers across manufacturers, formulators, and distributors under NDA.

- Patent landscape and regulatory-dossier analysis to infer capability gaps and likely re-registration pipelines.

- Commercial import-export flow analysis using trade reporting and shipment-level data to reconstruct physical flows and lead times.

- Laboratory partnerships and independent residue testing benchmarks to validate product performance claims in major export markets.

We synthesize these strands using a Layered Triangulation framework: independent sources, correlated behavioral indicators (e.g., CAPEX schedules vs. customs volumes), and stress-testing via Monte Carlo scenarios for feedstock and regulatory shocks. This methodology explains how we access, validate, and privilege non-public signals such as near-term capacity adjustments and confidential supply contracts—always obtained under contractual confidentiality or via publicly permissible sources—and then convert them into decision-grade recommendations.

2026 Strategic Checklist for Executives

Use this one-page checklist as a governance trigger to guide board and executive decisions this year:

- Have we stress-tested margins for a 20–30% step-up in carbon-disulfide-equivalent input costs, and do we have contingency sourcing?

- Does our registration portfolio cover critical export markets under the new EU residue definition, and do we have active re-submission plans?

- Are we partnered with accredited residue-testing labs to shorten customer acceptance cycles in regulated markets?

- Is there an actionable CAPEX plan for yield improvement and digital controls that meets our payback threshold in the current cost environment?

- Would a strategic alliance (tolling, JV, or minority equity) in feedstock or in-country registration accelerate our go-to-market value more than greenfield investment?

- Do we have a prioritized list of SKUs to retain, reformulate, or retire under heightened compliance scrutiny?

Next Steps and How to Access the Full Suite

2026 is a pivotal year where regulatory and feedstock pressures converge with technological levers for operational improvement. Acting now on registration management, feedstock security and digital yield programs materially alters risk-adjusted returns. PW Consulting’s full report delivers the models, maps, and company-level scorecards that enable executable strategies—rather than generic advice.

To obtain the complete dataset, scenario workbooks and the supplier scorecards referenced above, please access the full report here: https://pmarketresearch.com/worldwide-dithiocarbamate-fungicide-market-research .

For bespoke briefings, scenario workshops or confidential supplier due diligence tailored to your portfolio, PW Consulting’s industry team is available to run targeted sessions that translate the report’s insights into near-term execution plans for 2026.

For detailed analysis of this topic, please visit the official page: Dithiocarbamate Fungicides Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.