PW Consulting: Car Wax Market Poised to Expand at a 4.5% CAGR, Opening New Strategic Opportunities

Car Wax Market 2026: Strategic Imperatives from PW Consulting’s Latest Industry Brief

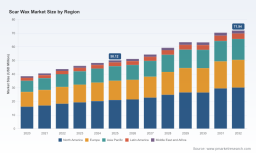

In 2026 the global car wax market stands at a strategic inflection point. After recovering from mid‑cycle volatility, the market reached USD 414.0 Million in 2025 and is projected to expand at a 4.5% CAGR over our 2026–2032 forecast horizon, reaching an estimated USD 563.4 Million by 2032. These headline metrics understate the tactical complexity facing manufacturers, distributors, and investors: value is being reallocated across formulations, distribution channels, and compliance obligations rather than delivered by simple volume growth.

Car Wax Market

Why 2026 Is a Critical Capital‑Allocation Moment

Three converging forces make 2026 a decisive year for capital deployment and strategic repositioning:

- Margin pressure from raw material cost oscillation—especially petroleum‑derived feedstocks—and rising logistics complexity;

- Premiumization of consumer demand, where a smaller share of the market captures outsized value through advanced polymer blends and long‑duration protectants; and

- Heightened regulatory and ESG scrutiny that elevates formulation transparency and supply‑chain traceability from nice‑to‑have to table stakes for large customers and fleet buyers.

Companies that act this year to lock in advantaged supply, retrofit production for lower carbon intensity, and validate higher‑value formulations will materially outperform peers through 2032.

Market Structure and Concentration

Our analysis shows the market remains moderately fragmented: the top three firms account for 27.5% of industry revenues and the top five for 34.2%. That concentration profile creates both opportunity and risk. Smaller, nimble formulators can win design‑in with premium detailers and OEM aftermarket programs, while large incumbents can leverage scale to optimize feedstock procurement and compliance overhead.

Product and Raw‑Material Dynamics

Understanding the chemistry that underpins performance is essential for 2026 decision‑making. Common car wax architectures combine high‑melting‑point microcrystalline waxes with softening agents and functional polymers to balance ease of application, durability, and gloss. Notably:

- Microcrystalline waxes—refined fractions of petroleum—provide adhesion and flexibility; their melting behavior and crystal morphology are key to end‑use performance.

- Blends are increasingly hybridized with synthetic polymers to extend longevity, which shifts cost and supplier risk toward specialty chemical providers.

- Sustainability pressures are prompting R&D toward biobased and lower‑VOC carriers, but replacement pathways require rigorous validation to match incumbent performance.

For commercial and procurement teams, these technical realities translate into three operational priorities: tighter raw‑material hedging, specification‑level supplier audits, and accelerated lab validation cycles—each detailed in our full report.

Practical Tools for 2026 Execution

The PW Consulting report is purpose‑built to move teams from insight to action. Key deliverables in the report include:

- End‑to‑end supply‑chain maps that identify single‑sourced inputs, logistics chokepoints, and tariff exposure;

- Bill‑of‑Materials (BOM) decomposition logic that isolates raw‑material cost drivers and their sensitivity to feedstock price moves;

- Yield‑adjustment and throughput models for blending and finishing operations to quantify margin uplift from process improvements;

- Technology roadmaps that compare incremental performance gains from polymer additives, nano‑fillers, and ceramic‑infused coatings versus cost and regulatory trade‑offs.

These are not theoretical blueprints. Each tool is accompanied by implementation playbooks—checklists, KPI templates, and decision matrices—designed to reduce the time between board approval and on‑line production. For teams prioritizing cost control, the BOM and yield models immediately identify short‑term interventions; for R&D and procurement leaders, the technology roadmap clarifies which material substitutions merit scale testing versus pilot programs.

Competitive Landscape: Dimensions That Matter

In 2026 the most relevant competitive advantages are less about marketing spend and more about defensible operational capabilities. Based on our cross‑sector benchmarking—covering specialist wax formulators, professional‑use suppliers, and broader chemical players—we group competitive moats into five dimensions:

- Formulation IP and testing credentials: proprietary blends and third‑party durability validation create procurement stickiness.

- Channel control: direct OEM programs, pro‑detailer partnerships, and national retail distribution each secure different margin profiles.

- Supply‑chain integration: backward integration into specialty waxes or long‑term offtake agreements reduces feedstock volatility.

- Regulatory and ESG compliance capability: documented chain‑of‑custody and lower‑VOC formulations accelerate access to fleet and municipal accounts.

- Operational scalability: automated blending, inline QA, and yield optimization enable margin expansion on modest top‑line growth.

To illustrate how these dimensions play out in practice, we include a benchmarking section in the report that references a wide spectrum of wax producers—from boutique, craft suppliers with tight specialty formulations to larger, global brands with distribution scale. While we do not publish proprietary 2026 strategy roadmaps for individual firms in this public brief, our competitive analysis shows what wins look like in the field—how design‑in occurs, which certification milestones unlock fleet contracts, and what supplier behaviors precede rapid share gains.

For readers interested in a company‑level comparison and the specific behaviors that presage market share shifts, consult our detailed competitor matrices and win‑loss analyses available in the full report: Read the full report .

Regulatory, ESG and Trade Compliance—Practical Impacts

Regulatory alignment is now a core commercial enabler for large customers. In 2026, procurement teams prioritize suppliers that can demonstrate:

- Traceability in hydrocarbon feedstock sourcing and processing;

- Lower lifecycle carbon intensities verified by third‑party frameworks; and

- Compliance with tightening VOC and waste‑management regulations in major markets.

PW Consulting’s compliance checklist and supplier audit templates de‑risk customer onboarding and accelerate qualifying timelines for larger contracts. For many suppliers, incremental compliance investment is the fastest path to higher‑margin, lower‑churn accounts.

Methodology: How PW Consulting Reaches Verifiable Conclusions

Our findings are built on layered triangulation and hands‑on verification. The methodology combines:

- Patent and standards analysis to map technological trajectories and identify emergent formulation IP;

- Proprietary customs and shipment analytics to quantify trade flows at a granular level; and

- Structured interviews with manufacturers, tier‑1 distributors, and major fleet procurement teams—conducted under confidentiality agreements—and hands‑on lab validation of representative formulations.

We emphasize that several inputs come from non‑public sources: anonymized supplier contracts, audited purchase orders, and in‑factory observations. These sources are synthesized via a multi‑step calibration process to remove bias and stress‑test scenarios. This methodology yields actionable forecasts and risk matrices that are directly applicable to procurement, R&D prioritization, and M&A diligence.

Actions for Executives in 2026

Based on our scenario analysis, executive teams should prioritize three actions this year:

- Lock in critical feedstock through diversified suppliers or hedged offtake agreements to stabilize gross margins;

- Invest selectively in formulation validation and third‑party durability testing to access premium distribution and fleet contracts; and

- Operationalize an ESG compliance program that couples supplier audits with product‑level lifecycle disclosure to protect growth in regulated markets.

Each of these actions is mapped to a short‑term ROI case and an implementation timeline in the report, so teams can convert strategy into executable roadmaps within a single quarter.

Conclusion: Where Value Will Be Captured

Growth in the car wax market through 2032 will be steady but selective. The headline CAGR of 4.5% masks a redistribution of value toward formulations and channels that meet higher durability, sustainability, and traceability expectations. PW Consulting’s report translates these macro dynamics into operational checklists, financial sensitivities, and go‑to‑market playbooks that senior leaders can deploy this year to capture disproportionate returns.

To access the full set of tools—supply‑chain maps, BOM decomposition models, yield uplift calculators, and competitor matrices—please follow this link: Read the full report .

For detailed analysis of this topic, please visit the official page: Car Wax Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.