PW Consulting: Electronic Faucets Market to Climb from USD 4.3 Million in 2025 to USD 15.6 Million by 2032 at a 10.4% CAGR

Electronic Faucets Market 2026: Strategic Imperatives from PW Consulting

PW Consulting publishes a focused industry briefing in 2026 that synthesizes market sizing, technology trajectories, supply‑chain intelligence, and regulatory dynamics for the global electronic faucets market. Our harmonized model projects the market expanding to 8.7 Million USD in 2026 and tracking to 15.6 Million USD by 2032, implying a 10.4% compound annual growth rate over the 2026–2032 forecast window. These headline metrics mask rapid structural shifts that will determine winners and losers in the next 18 months.

Electronic Faucets Market

Why 2026 is a decisive inflection point

Market momentum in 2026 is driven by converging forces that increase both opportunity and execution risk for manufacturers, system integrators, and channel partners. The most consequential are:

Electronic Faucets Market

- Acceleration of touchless and voice-enabled adoption driven by health, hygiene, and retrofit demand in commercial and residential sectors.

- Service monetization: vendors shift from pure hardware sales to hybrid capex/opex models (product + monitoring/service), increasing lifetime value but raising compliance and billing complexity.

- Escalating regulatory scrutiny and liability for tampering or non‑compliant installations, leading buyers to prioritize certified, tamper‑resistant designs.

- Supply‑chain reconfiguration and nearshoring to manage semiconductor volatility and logistics costs; OEMs with modular BOMs capture margin upside.

- Manufacturing upgrades using AI/ML for yield optimization and predictive maintenance, compressing time‑to‑scale for new designs.

What PW Consulting’s report delivers — practical tools for 2026 decisions

Our report is deliberately operational. It does not stop at topology and forecasts; it equips decision makers with implementable instruments that directly address 2026 pain points:

- Supply‑chain map with supplier tiering and single‑point‑of‑failure flags to prioritize sourcing actions.

- Proprietary BOM teardown logic that isolates high‑impact line items and substitution levers for cost reduction without degrading certification prospects.

- Yield adjustment models that translate factory NPI yields into working capital and lead‑time sensitivity analyses for ramp planning.

- Technology roadmap linking sensor stacks (IR, capacitive, ultrasonic, voice platforms), connectivity (Wi‑Fi/eSIM), and power management options to certification and retrofit pathways.

- Regulatory and compliance matrix that maps regional certification requirements to design controls and documentation needs.

Each tool is paired with a tactical playbook—how to run a three‑month pilot, how to structure supplier warranties, and how to sequence certification—to make 2026 capital deployment less speculative and more irreversible.

Data‑driven market view (high level)

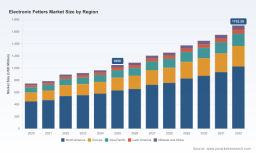

Our historical series and forward projections provide a coherent growth narrative from 2020 through 2032. The market expands from a low‑single‑digit base in 2020 to a mid‑single‑digit global market by 2024, establishing a 2025 baseline and accelerating into 2026. By 2032 our forecast reaches 15.6 Million USD. Market concentration is moderate: CR3 is ~32.0% and CR5 is ~40.0%, indicating room for consolidation and design‑win disruption but also meaningful incumbency advantages for scale players.

Detailed regional and application splits are included in the full report; we intentionally withhold the granular distribution here to encourage stakeholders to review the corresponding charts and scenario matrices that inform procurement and M&A planning.

Competitive landscape — the dimensions that determine design wins

Winning in 2026 comes down to mastering a small set of competitive dimensions rather than attempting to maximize all capabilities simultaneously. Our analysis shows buyers award design wins on:

- Proven tamper resistance and physical durability (materials, mechanical design, and tamper detection).

- Integrated software and cloud services that simplify commissioning, remote diagnostics, and warranty management.

- Channel and spec‑writer relationships (architects, facility managers, hospitality procurement) that shorten procurement cycles.

- Manufacturing cost base and flexible contracts enabling rapid price responses to tender dynamics.

- Regulatory and certification track record—buyers prefer suppliers who can demonstrate pre‑cleared compliance across priority markets.

We draw instructive parallels from adjacent device sectors. Recent vendor announcements in the electronic monitoring domain highlight transferable lessons: fiber‑optic tamper detection and advanced eSIM/5G connectivity underscore the premium buyers place on persistent, verifiable device health telemetry; incremental battery and ergonomic improvements demonstrate how small product engineering shifts materially improve compliance and end‑user acceptance; and state‑level penalties for tampering raise the cost of non‑compliance, favoring suppliers with documented tamper‑proofing approaches.

PW Consulting’s report does not publish full strategic forecasts for individual vendors in order to protect proprietary forecasting inputs, but it does profile the competitive moats we observe and the tactical levers (e.g., platform licensing, vertical integration, aftermarket service contracts) that most reliably translate to sustained share gains.

Supply‑chain and manufacturing levers to protect margins in 2026

Manufacturers who preserve margin and speed in 2026 apply disciplined levers across product, process, and procurement:

- BOM rationalization: prioritize components with multiple qualified sources and reduce custom ASIC scope where COTS solutions suffice.

- Yield‑first NPI: set production acceptance gates tied to financial triggers rather than shipment milestones.

- Contractual agility: embed price‑reopener clauses for critical commodities and scalable volume commitments with Tier‑1 EMS partners.

- Digital factory rollouts: deploy ML‑driven test‑and‑inspection to reduce false failures and speed up certification cycles.

- ESG and compliance as a sales instrument: certify material sourcing to reduce procurement friction with large buyers.

Methodology — how PW Consulting guarantees actionable fidelity

PW Consulting uses a layered‑triangulation methodology to deliver market intelligence that is reproducible and defensible. Key inputs include patent family mapping, customs and trade data, firmware and protocol reverse engineering, structured interviews across OEMs, tier‑1 suppliers, leading installers, and major channel partners, and a curated panel of procurement officers that validate pricing and TCO assumptions.

We also draw on proprietary primary data sources: anonymized device telemetry (with end‑user privacy controls), NDAs with manufacturers and EMS partners that disclose unit economics, and site‑level factory acceptance reports. These channels enable us to reconcile public filings and patent claims with real world build practices—without disclosing any confidential contract terms. Our BOM teardowns are tested against observed procurement invoices and adjusted using yield models derived from on‑site assembly observations and QC logs.

Regulation, ESG and compliance: operating realities for 2026

Regulatory intensity is rising in 2026. Several jurisdictions have tightened penalties for device tampering, and procurement bodies increasingly require clear documentation of product safety and end‑of‑life practices. At the same time, large commercial buyers are demanding verifiable ESG signals in supply chains. These trends shift purchasing criteria in favor of vendors that can deliver transparent compliance artifacts, robust remote diagnostics, and predictable service economics.

Strategic recommendations for capital allocation in 2026

For executives allocating capital this year, PW Consulting recommends a prioritized approach:

- Allocate a first tranche to platform and software that enable recurring revenue—this increases valuation multiples even if hardware margins compress.

- Invest in tamper‑resistant hardware features and third‑party certifications to win institutional contracts and reduce warranty exposure.

- Ring‑fence a rapid NPI budget for a “retrofit” product line tailored to commercial retrofit projects where adoption cycles are fastest.

- Pursue selective M&A or strategic supply agreements to shore up critical components where single‑sourcing risk is high.

- Embed ESG and end‑of‑life commitments into product roadmaps to avoid procurement exclusions by large accounts.

How to get the full intelligence and next steps

PW Consulting’s full Electronic Faucets Market report contains the granular charts, regional and application splits, supplier scorecards, and step‑by‑step playbooks necessary to convert insight into execution. For immediate access to the complete dataset and the downloadable executive packet, visit the report page at https://pmarketresearch.com/it/electronic-fetters-market .

PW Consulting stands ready to support tailored briefings, scenario stress‑tests, and NPI peer reviews to accelerate evidence‑based decisions in 2026.

For detailed analysis of this topic, please visit the official page: Electronic Faucets Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.