PW Consulting: Acetyl Chloride Market Poised for Steady Expansion at a 4.0% CAGR Through 2032

PW Consulting: Strategic Preview — Acetyl Chloride (Valeryl Chloride) Market Outlook 2026

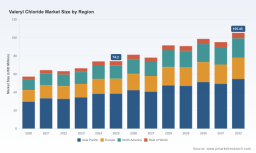

In 2026, corporate decisions about specialty acyl chlorides must be both fast and forensic. PW Consulting’s forthcoming Acetyl Chloride (Valeryl Chloride) Market report frames that decision context by combining a compact macro view with deep, executable intelligence on supply chains, technical routes, and competitive dynamics. The market has expanded from approximately 0.3 Billion USD in 2020 to about 0.4 Billion USD in 2025 and is projected to reach roughly 0.5 Billion USD by 2032, growing at a 4.0% CAGR across the 2026–2032 forecast window. This briefing highlights why those headline metrics matter for capital allocation, procurement strategy, and regulatory risk mitigation — and why stakeholders should consult the full report for transaction-level signals.

Acetyl Chloride Market

Executive Summary: Why 2026 Is Different

Three structural shifts compress investment timing into 2026:

- Regulatory tightening around chlorinated intermediates is raising compliance and disposal costs, altering supplier economics and prompting a reassessment of insured suppliers versus lowest-cost vendors.

- Raw-material sensitivity — particularly to valeric (n‑valeric) acid feedstocks and common chlorination reagents — is increasing margin volatility across the value chain.

- Consolidation at the top end of the market has produced a concentrated supplier set (CR3 ≈ 58.0%, CR5 ≈ 72.0%), concentrating counterparty risk and intensifying competition for long-term offtake agreements.

Collectively, these dynamics make 2026 the year to re-run supply-side stress tests, redesign contract trigger clauses for compliance contingency, and evaluate capital investments in containment and emissions control.

Market Dynamics — Drivers, Constraints, and Tactical Impacts

Key dynamics shaping near-term strategy:

- Cost Pass-Through and Feedstock Exposure: Valeryl chloride pricing remains tightly coupled to valeric acid availability and the cost of chlorination reagents. Procurement teams must model multi-source scenarios rather than rely on single-supplier forecasts.

- Regulatory and Handling Burdens: Compliance regimes such as REACH and heightened local environmental enforcement increase the effective cost of doing business for producers. The corrosive and flammable nature of the product demands lined or fluorinated packaging and strict storage protocols, which influences logistics and insurance terms.

- Concentration and Contracting: A compact supplier base drives lengthening lead times for qualified supply; design-win and qualification cycles are decisive in securing capacity during 2026 procurement rounds.

These factors converge to create a premium on three operational capabilities in 2026: validated multi-jurisdictional compliance, demonstrable quality consistency (COA traceability), and agile logistics agreements that cover special packaging and emergency containment.

Segmentation and Demand Trends (High Level)

The market continues to split along type and application lines, with demand concentrated in higher-purity grades for pharmaceutical and fine-chemical synthesis and steady demand from agrochemicals and specialty materials. Rather than rehearse detailed regional or application-level shares here, the report maps demand elasticity across purity tiers and end-use sectors and visualizes how the market’s center of gravity is shifting toward producers and consumers with integrated supply assurance capabilities. For a full breakdown and interactive distribution maps, consult the complete report.

Supply Chain & Operational Tools — What the Report Delivers

PW Consulting’s report is deliberately practical. We provide tools and templates that procurement, R&D, and operations teams can act on without waiting for consultancy workshops. Key inclusions:

- Supply-Chain Topology Map: A layered network view that highlights node-level regulatory exposure, alternate-route capacity, and critical logistics chokepoints.

- BOM Decomposition and Cost-Attribution Logic: A modular framework that separates reagent input costs, energy, compliance amortization, and packaging premiums so firms can run scenario-based margin forecasts.

- Yield Adjustment and Loss Models: Parametric models for reaction yield variability and downstream losses (hydrolysis, packaging migration), enabling stress-testing of procurement lots and safety stock policies.

- Technology Roadmaps: Comparative assessments of chlorination routes (e.g., thionyl chloride vs. phosphorus trichloride pathways), including practical implementation barriers and upgrade sequencing for emissions mitigation.

- Qualification and Audit Playbooks: Checklists and contract clauses for ensuring coating/lining specifications on drums, storage stability verification, and emergency response obligations.

Each tool is presented as a configurable template — we show logic and decision levers, but not prescriptive parameter outputs — enabling users to plug in their own internal data and regulatory constraints to derive actionable results tailored to 2026 operational realities.

Competitive Landscape — Dimensions of Advantage (Not Predictions)

Our industry mapping identifies a set of incumbent and specialist producers with distinct competitive moats. PW Consulting’s evidence-based analysis focuses on the structural dimensions that determine procurement choices and design wins rather than speculative company roadmaps. Important competitive vectors include:

- Quality and Purity Tiering: Providers that consistently certify high-purity grades and maintain detailed COAs command premium placements for pharmaceutical synthesis and R&D supply agreements.

- Regulatory and Compliance Footprint: Producers with REACH registrations, documented emissions controls, and formal waste-handling chains reduce buyer compliance overhead and shorten qualification cycles.

- Integrated Service & Customization: Firms offering contract synthesis, small-batch custom runs, or tailored packaging solutions improve design-win probability for complex intermediates.

- Logistics and Packaging Specialization: Suppliers that standardize fluorinated/lined drum supply chains and provide validated storage protocols often become de‑facto preferred partners for customers with tight handling specifications.

- Geographic Resilience and Diversification: Manufacturers with multi-site footprints or reliable third-party tolling arrangements mitigate single-node downtime and currency-related supply shocks.

Examples drawn from company profiles illustrate these dimensions across multiple jurisdictions: Chinese and Indian manufacturers lean on cost and custom synthesis capabilities; US specialty producers emphasize specification depth and packaging standards; certain Indian firms offer export-oriented compliance and COA-backed research-grade supply. For readers preparing 2026 sourcing strategies, these are the competitive attributes that will determine access to capacity and price negotiation leverage — the full report includes our segmented supplier scorecards and a procurement risk matrix.

Access the full Worldwide Valeryl Chloride Market Research report for supplier scorecards and procurement matrices: Access the full Worldwide Valeryl Chloride Market Research report .

Regulatory, Safety, and ESG Considerations

Production and handling of chlorinated acyl intermediates are under intensified scrutiny. The report synthesizes regulatory implications for 2026 procurement decisions:

- Compliance Costs: Expect increased capital expenditures for emissions control and disposal across OECD jurisdictions; non-compliant suppliers face market exclusion risks.

- Handling and Packaging: The corrosive, flammable nature of the product mandates specific drum linings and storage protocols — failures translate to both operational downtime and reputational risk.

- ESG Disclosure Pressure: Buyers and financiers increasingly demand supplier-level environmental metrics; companies lacking verifiable footprint reductions will see higher cost of capital.

These pressures favor buyers who proactively requalify suppliers, incorporate environmental indemnities into contracts, and prioritize suppliers that provide third-party emissions verification.

Methodology — How PW Consulting Reaches Actionable Conclusions

PW Consulting’s analysis rests on Layered Triangulation, a multi-source validation approach that combines patent citation mapping, regulatory filings, customs and trade flows, site-level audits, and structured supplier interviews. We corroborate modeled outputs against laboratory verification of representative lots and technical data sheets where available.

Specifically, our team: (1) extracts patent families and citation networks to infer technology transfer pathways; (2) overlays customs and shipment patterns to validate trade flows; (3) conducts confidential interviews with procurement heads and plant managers to capture non-public lead-time and qualification constraints; and (4) runs field audits or remote-sensing checks where physical verification is required. This methodological rigor is designed to produce defensible, transaction-level insight while preserving commercial confidentiality for interviewed parties.

Strategic Recommendations for 2026

For C-suite and procurement leaders evaluating capital or sourcing changes in 2026, PW Consulting highlights three immediate actions:

- Run a supplier qualification replay using the supplied BOM-decomposition templates to identify true landed cost under tightened regulatory scenarios.

- Prioritize long-term contracts with capacitated, compliance-ready suppliers and insert escalation clauses for feedstock shocks; include packaging and emergency-handling warranties.

- Initiate selective investments in upstream integration (captive valeric acid conversion) or co-investment with preferred suppliers to secure feedstock reliability and margin stability.

Each recommendation is supported by the operational models and supplier matrices contained in the full report, enabling immediate execution planning rather than high-level advisory alone.

Next Steps and How to Obtain the Report

This release intentionally outlines the strategic scaffolding and tools available without publishing granular segment values and supplier forecasts. For the complete dataset, interactive charts, supplier scorecards, and downloadable templates, request the full market study here: Access the full Worldwide Valeryl Chloride Market Research report .

PW Consulting’s Acetyl Chloride Market report is positioned to serve as a decision-useful guide through 2026 — combining macro clarity with the operational playbooks procurement, R&D, and corporate development teams need to convert uncertainty into competitive advantage.

For detailed analysis of this topic, please visit the official page: Acetyl Chloride Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.