PW Consulting: Potting Soil Market Poised for Recovery, Forecasting a 3.7% CAGR

Potting Soil Market 2026 Outlook: Strategic Imperatives for Capital Allocation

Executive snapshot

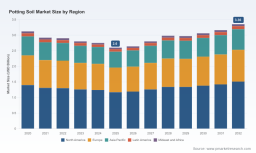

PW Consulting's Potting Soil Market study (base year 2025; historical period 2020–2025; forecast period 2026–2032) positions the global market at USD 2.6 Billion in 2025 and projects recovery-driven expansion to approximately USD 3.4 Billion by 2032, reflecting a compound annual growth rate (CAGR) of 3.7% over the 2026–2032 horizon. The recent five-year pattern shows a contraction through 2025 followed by a multi-year rebound beginning in 2026 — a profile that fundamentally changes the calculus for 2026 capital allocation and operational planning.

Why 2026 is a pivotal year for investors and operators

-

Regulatory inflection points are binding. Several major markets accelerate peat restrictions and embed extraction in land-use mitigation targets during 2026, creating immediate compliance and reformulation imperatives for both retail and professional channels.

-

Raw-material supply shocks are operating contemporaneously with regulatory shifts. Weather-driven peat availability issues and increasing coir costs are compressing supplier margins and elevating procurement risk, requiring more active supply chain strategies.

-

Product and packaging innovation are converging with consumer sustainability demands. Biodegradable packaging and peat-free formulations are moving from niche to table stakes for growth-focused brands.

-

Market structure remains fragmented: market concentration metrics indicate a dispersed supplier base (CR3 ≈ 24.6% ; CR5 ≈ 28.2%), which favors nimble incumbents and well-capitalized challengers that can rapidly scale new formulations and distribution models.

Market dynamics shaping 2026 decisions

-

Policy-driven peat phase-outs are creating near-term demand for alternative substrates and certification pathways; this increases compliance costs and short-term reformulation CAPEX for manufacturers.

-

Peat-free blends carry a price premium versus peat-containing alternatives; independent studies show the average premium is material enough to alter gross-margin dynamics unless production and sourcing strategies are optimized.

-

Supply-side tightness for peat and coir is contributing to elevated price volatility and logistics complexity, pushing procurement teams to adopt hedging, performance-based contracts, and alternative raw-material qualification programs.

-

Retail and professional channels are polarizing around performance claims (microbial inoculants, water-holding additives) and sustainability credentials, making design wins increasingly contingent on verifiable third-party metrics and reproducible agronomic performance.

Report toolkit: What the PW Consulting study delivers — and how clients use it

Our 2026-focused report is engineered for decision-makers who must convert strategy into operational plans under compressed timelines. We provide a suite of practical tools that translate market signals into executable actions without divulging the proprietary segment-level figures in this summary.

-

Supply‑chain map — end‑to‑end visibility from feedstock origins to retail shelves, highlighting choke points and modal exposure so procurement leaders can prioritize dual-sourcing and nearshoring investments.

-

BOM (bill-of-materials) decomposition logic — a standardized template that dissects formulations into cost drivers, enabling scenario-based cost-to-serve and margin simulations under alternative input-price trajectories.

-

Yield adjustment models — factory-level modules that quantify the impact of formulation changes, moisture control, and line-speed modifications on throughput and waste, supporting CAPEX vs. OPEX trade-offs.

-

Technology roadmap — a comparative view of peat alternatives, biochar and microbial adjuncts, wood-fiber processing technologies, and packaging innovations, structured around readiness, unit-cost trajectory, and regulatory risk.

-

Commercialization playbooks — go-to-market templates that link formulation attributes to channel-specific success factors (retail shelving, professional trial programs, co-branded OEM opportunities).

How these tools address 2026 pain points

-

Cost containment: BOM logic and yield models let manufacturers simulate cost parity pathways for peat-reduced mixes and quantify where process improvements offset raw material premiums.

-

Compliance readiness: the technology roadmap and supply‑chain map identify substitutes and certification pathways that reduce regulatory exposure while preserving product performance.

-

Speed-to-market: commercialization playbooks shorten the typical development-to-shelf cycle by aligning R&D, procurement, and channel partners on measurable design-win criteria.

Competitive landscape: dimensions that determine winners in 2026

The potting soil sector rewards a specific combination of capabilities more than mere scale. Our competitive analysis — based on proprietary supplier interviews, patent citation mapping, and retail shelf audits — shows the decisive competitive dimensions are:

-

Raw-material control and traceability: firms that secure stable, certified feedstock sources (or operate integrated peat alternatives production) reduce exposure to price spikes and compliance risk.

-

Formulation IP and agronomic validation: success is tied to demonstrable performance (water retention, nutrient release, microbial stability) validated through third-party lab and grower trials.

-

Channel sophistication: retailers prize consistent SKU performance and packaging ergonomics; professional horticulture demands consistent bulk formulations and logistical reliability.

-

Operational flexibility: manufacturers with modular lines or quick-change capabilities convert regulatory shocks into product variety without prohibitive downtime.

-

Brand and sustainability credentials: certification, transparent carbon accounting, and packaging innovations are increasingly gateways to premium placement.

Public and private firms that combine these attributes — for example, leaders in consumer brand reach, professional substrate know-how, or peat-free R&D — have clearer routes to Design Wins in both retail and commercial horticulture. For a deeper company-by-company analytical framework and comparative matrices, read the full PW Consulting industry brief: Access the full Potting Soil Market report .

Technology and product pathways to prioritize in 2026

-

Peat-reduced and peat-free blends with enhanced water management — formulations that restore or exceed peat performance via fiber technologies, biochar, and controlled-release matrices.

-

Microbial augmentation and inoculants — products that deliver measurable plant health benefits and support premium positioning, but require consistent cold-chain and stability controls.

-

Circular feedstocks — compost-from-waste initiatives are entering retail and professional channels; these require supply contracts, QA frameworks, and traceability systems to scale.

-

Packaging and circularity — biodegradable and lower-carbon packaging are accelerating retailer acceptance, but must be matched with shelf-life and handling tests.

Design wins in these pathways are determined by a set of repeatable commercial criteria: reproducible field performance, supply security, unit-cost trajectory, and credible sustainability verification. For practitioners seeking a prescriptive technology-phasing plan aligned to regulatory timelines, follow our implementation guidance: Access the full Potting Soil Market report .

Methodology: why our signals are uniquely actionable

PW Consulting applies Layered Triangulation across primary, secondary, and real-world trace data to produce defensible conclusions. Our approach integrates patent-citation analysis, customs and trade-flow synthesis, retail POS analytics, targeted supplier and grower interviews, and laboratory performance testing. We cross-validate observed pricing and availability signals with on-site audits and anonymized contract reviews so the recommendations reflect executable realities rather than theoretical models.

Critically for 2026 decision-making, we disclose how we capture otherwise opaque signals: direct interviews with supply‑base participants and downstream buyers, facility-level sampling and lab assays, and proprietary scraping of retail assortments and shipment records. These methods allow us to infer supply constraints, margin pressure, and early adoption indicators before they appear in conventional datasets.

Strategic implications and actions for 2026

-

Reassess raw-material strategies now: prioritize dual-sourcing, strategic inventory, and partnerships for circular feedstock to smooth 2026 volume volatility.

-

Accelerate product platforms that de-risk peat substitution while protecting agronomic performance; use our BOM templates to model margin and break-even scenarios.

-

Target modular capex that enables rapid SKU conversion over large mono-line investments — flexibility outperforms scale in a fast-regulating environment.

-

Implement third‑party verification and transparent carbon accounting to preserve access to premium retail placements and institutional buyers.

-

Pursue selective M&A or supply partnerships to secure feedstock control or proprietary formulation rights where internal development timelines are too long.

-

Embed digital manufacturing and yield-optimization tools to convert incremental efficiency gains into meaningful gross-margin recovery.

Conclusion and next steps

In 2026, companies that act with urgency — converting regulatory foresight and supply-chain intelligence into operational programs — will capture disproportionate share of the recovery and premium growth. PW Consulting’s Potting Soil Market report equips executives with the playbooks, models, and evidence base required to make those decisions with confidence.

To obtain the full dataset, regional and application breakdowns, and the company-level comparative matrices referenced in this executive brief, please download the complete report: Access the full Potting Soil Market report .

For detailed analysis of this topic, please visit the official page: Potting Soil Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.