PW Consulting: Mining Machine Market Poised to Grow at 6.5% CAGR on Rising Surface and Underground Equipment Demand

PW Consulting: Strategic Outlook — Mincing Machines Market (2026)

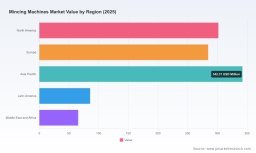

Now in 2026, the global mincing machines market is at an inflection point. After expanding from USD 127.8 Million in 2020 to USD 163.2 Million in 2025, PW Consulting’s baseline model projects the market to reach USD 176.0 Million in 2026 and to grow at a 6.5% CAGR through 2032, arriving near USD 253.5 Million by the end of the forecast window. This trajectory reflects both steady end‑market demand and accelerating capital investment driven by regulation, automation, and supply‑chain reconfiguration. For executives deciding 2026 capital allocation, these dynamics create a narrow window to reorient product roadmaps, sourcing, and go‑to‑market plays before regulatory and cost pressures crystallize in 2027–2028.

Mining Machine Market

Market trajectory: what’s changing (and why it matters)

The headline growth masks three converging shifts that determine winners and losers in 2026:

- Structural demand for higher throughput and frozen‑product capability — processors are consolidating and specifying machines that combine sanitation, throughput, and flexibility for multiple protein types.

- Cost pressure from component inflation and tariffs — rising motor, stainless steel, and electronic component costs push OEMs to redesign BOMs and rethink supplier geographies.

- Regulatory and compliance acceleration — new machinery safety and software/cyber rules are moving from guidance to enforceable standards, prompting capital and service investments ahead of full enforcement.

Each of these factors multiplies operational risk: a poorly scoped modernization program can leave manufacturers exposed to warranty costs, lost design wins, or regulatory non‑compliance. Conversely, targeted investments in modular design and service‑led revenue models can convert near‑term headwinds into durable pricing power.

2026 flashpoints: where decisions compress value

As boards debate 2026 budgets, three near‑term flashpoints compress decision timelines:

- Regulation compliance timing — major regional machinery regulations (covering functional safety, cybersecurity of embedded controls, and post‑market surveillance) require enterprises to demonstrate preparation during 2026 ahead of stricter enforcement windows.

- Component cost and supply risk — tariffs and material inflation materially change the math on offshore vs. nearshore sourcing; lead times for critical subassemblies are longer and more volatile.

- Design‑win economics — large processors are shortening bid cycles and demanding proof points (sanitization, uptime, energy efficiency) that are now decided in 2026 procurement rounds.

These flashpoints mean capital preservation alone is insufficient: companies must re‑engineer product and service propositions to protect margins while securing next‑generation contracts.

Operational toolkit in this report: practical levers for 2026 execution

PW Consulting’s Mincing Machines Market report is built as an execution playbook, not a slide deck. The deliverables are organized to move teams from insight to action within a single planning cycle:

- Supply‑chain topology and resilience map — visualizes tiers, single‑point‑of‑failure suppliers, and alternative sources to prioritize nearshoring or dual‑sourcing decisions.

- BOM teardown logic and cost‑reduction pathways — layered analysis identifies substitution, design simplification, and standardization levers that preserve performance while lowering total landed cost.

- Yield‑adjustment and throughput models — link machine configuration to plant yield and operating cost, enabling scenario testing of design trade‑offs without long pilot runs.

- Technical roadmap and modularization playbook — prescriptive pathways to migrate legacy platforms to modular architectures that accelerate feature delivery and lower field retrofit costs.

- Compliance readiness checklist and software update governance — operational templates for meeting the new machinery safety and cyber requirements with an audit trail suitable for regulators and large customers.

- Capex prioritization matrix and scenario stress tests — ranks investment candidates by payback under varied raw‑material and tariff scenarios.

Each tool is calibrated for 2026 realities: short procurement cycles, constrained CapEx, and emergent regulatory evidence requirements. The aim is to let product, procurement, and compliance teams converge on a single set of executable priorities within 90 days.

Competitive landscape — dimensions that decide 2026 design wins

Our competitive analysis focuses on the commercial and technical dimensions that determine design wins in 2026, not on speculative forecasts of individual corporate strategies. Across the installed vendor set, PW Consulting identifies three enduring competitive dimensions:

- Platform and service moat — vendors with broad installed bases and proven field service networks convert uptime credibility into pricing power; service‑led warranty models are a differentiator.

- Hygienic and frozen‑processing IP — design features that materially reduce microbial risk or reliably handle frozen inputs are primary decision criteria for large processors.

- Supply‑chain and manufacturing scale — scale advantages in procuring motors, bearings and high‑grade stainless components allow selective margin restoration under cost stress.

Applying those dimensions to identifiable players yields actionable positioning statements (examples in the full report):

- Hobart Corporation — deep aftermarket footprint and channel strength that accelerates enterprise adoption where service risk is the buyer’s primary concern.

- LEM Products — lean, niche engineering advantage in lower‑capacity segments; product simplicity and cost focus drive share in specific channels.

- Rome Grinding Solutions — recent launches signal focus on high‑throughput frozen handling; the combination of dual‑stage architectures and supplier partnerships is a design‑win vector.

- Seydelmann and Marel — strong hygienic design IP and automation integration capabilities position them as preferred suppliers for large processors pursuing throughput and compliance simultaneously.

- Weston and The Sausage Maker — channel and hobbyist reach that support a differentiated value proposition in smaller commercial and retail segments.

This framework highlights where rivals are vulnerable and where incumbent advantages are durable; for procurement and R&D leaders, it defines the short list of capabilities to secure in 2026. For detailed comparative matrices and capability heatmaps, read the report: Full Mincing Machines Market Report .

Methodology and evidence base

PW Consulting’s conclusions rest on a layered‑triangulation methodology designed to surface non‑public, transaction‑level signals while removing single‑source bias. Our core methods include patent citation mapping to detect emergent design IP, proprietary teardown labs for BOM validation, customs and invoice scraping to triangulate component flows, and structured interviews with OEM procurement and food‑processor engineering leads. We then validate commercial assumptions with machine‑level telemetry where available and controlled field trials. This approach produces both directionally robust market sizing and the granular levers used in the operational toolkit.

Critically, several inputs are sourced under NDA or via anonymized industrial data partnerships. That enables us to resolve supplier bottlenecks and manufacturing cost curves that are invisible in public filings. The report documents our triangulation confidence bands and audit trail without exposing sensitive third‑party contract details.

Practical 2026 playbook — six immediate actions

Leaders must convert insight into decisive moves this year. Recommended near‑term actions, all executable with the artifacts in our report, include:

- Run a 90‑day BOM reduction sprint focused on top 10 cost drivers and validate changes in the yield model before supplier changes.

- Prioritize modular upgrades that deliver compliance and uptime improvements with minimal CapEx — aim for retrofitable subassemblies that satisfy 2027 regulatory evidence needs.

- Secure dual‑sourcing for key subassemblies and open supplier RFIs that include total landed cost scenarios post‑tariff.

- Focus R&D on hygienic throughput and frozen‑product reliability — these are the shortlists in large processor RFPs in 2026.

- Reconfigure service contracts towards uptime guarantees and remote diagnostics to monetize installed bases and reduce warranty leakage.

- Stress‑test 2026 capex plans using the report’s scenario simulators to quantify downside under aggressive raw‑material and tariff assumptions.

These moves preserve optionality and create defensible revenue streams as regulatory and commercial pressures intensify.

How to use this report right now

Executives should use the report as a playbook to align R&D, procurement, and sales before the next procurement season closes. The combination of BOM teardowns, supply‑chain mapping, and the yield models allow teams to convert a single engineering change into measurable margin improvement and faster design‑win cycles. For procurement and strategy teams preparing 2026 budgets, the report contains actionable scenario tools, comparative vendor capability matrices, and compliance readiness templates designed for immediate deployment. Access the full toolkit here: Full Mincing Machines Market Report .

PW Consulting’s 2026 Mincing Machines Market analysis is intentionally prescriptive: it shows the levers that matter this year, documents the evidence behind them, and delivers decision‑quality tools while withholding sensitive commercial tables to preserve client confidentiality. For boards and C‑suites needing a concise, executable runway into 2027, the report is designed to be the single source of truth.

For detailed analysis of this topic, please visit the official page: Mining Machine Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.