PW Consulting: Automotive Voice Recognition Market Poised to Expand at a 14.2% CAGR, Revolutionizing In‑Car Voice Experiences

Automotive Voice Recognition Market: Strategic Intelligence for 2026 Decisions

Executive summary

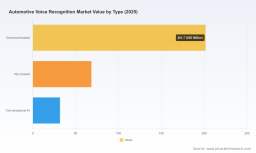

PW Consulting’s latest Automotive Voice Recognition Market report (base year: 2025; historical window: 2020–2025; forecast period: 2026–2032) delivers an evidence-based, decision-ready view for executives who must allocate product, platform and partnership capital during the pivotal 2026 planning cycle. The market is on a sustained expansion trajectory — our model shows a compound annual growth rate (CAGR) of 14.2% across the 2026–2032 forecast window. Measured against the 2025 baseline (USD 302.0 Million), the market is projected to evolve materially by 2032 under multiple demand and technology inflection points.

Automotive Voice Recognition Market

Why this report matters for 2026

-

Strategic timing: 2026 is when regulatory guardrails, edge compute capability and OEM product roadmaps converge. Procurement and platform decisions made this year will determine who captures the earliest monetization opportunities (voice commerce, subscription services) and who locks in embedded OEM relationships.

Automotive Voice Recognition Market -

Risk mitigation: The report translates evolving compliance requirements — notably the EU AI Act’s mandates for machine-readable metadata and digital audio watermarking — into concrete vendor evaluation criteria and integration checklists that preserve product velocity while reducing legal exposure.

Automotive Voice Recognition Market -

Value capture: We show how hybrid architectures (on-device ASR + cloud-based NLU/LLM augmentation) balance latency, cost and privacy to create defensible UX advantages while enabling new revenue streams.

Market posture and macro dynamics

Automotive voice recognition has moved beyond proof-of-concept. The category is now characterized by accelerated OEM adoption, investments by cloud and semiconductor leaders, and the emergence of “agentic” voice assistants that combine task automation with commerce enablers. The market concentration profile — with the top three firms commanding a substantial share and the top five comprising an even larger portion — signals that scale, IP breadth and OEM trust are meaningful barriers. This dynamic favors vendors that can demonstrate automotive-grade robustness, regulatory compliance and global OEM deployments.

Technology and regulatory inflection points

-

Edge-first resilience: Increasingly, production systems prioritize embedded, noise-robust ASR and edge-capable architectures to handle in-cabin acoustics, multi-speaker scenarios and disconnected operation. This shift affects procurement logic, hardware selection and long-term maintenance costs for connected vehicle fleets.

-

Hybrid agentic architectures: Generative AI has moved from lab demos to curated product features. Agentic platforms that orchestrate local intent resolution with cloud-based LLM augmentation enable richer conversational UX while containing data egress and latency.

-

Regulatory compliance as product requirement: By mid-2026 the EU AI Act and related standards will impose technical constraints (e.g., metadata, watermarking for synthetic speech). Vendors already integrating these controls provide a faster compliance path for OEMs and suppliers.

-

Supply chain and security: Public policy updates directed at connected vehicle supply chains require new provenance and security proofs for voice stacks — a point that should be embedded into vendor contracts and system architectures.

Competitive landscape — what to watch

The report synthesizes primary research and public disclosures to profile incumbent platform leaders, hyperscaler/sovereign entrants and OEM integrators. Several themes emerge:

-

Cerence AI: A clear leader in embedded, automotive-grade voice platforms with extensive in-vehicle shipments and a matured product portfolio (including hybrid agentic systems and xUI). Recent product updates (improved embedded ASR, modular streaming APIs) and live demonstrations at AutoTech2026 underscore Cerence’s strategy of delivering low-latency, on-device performance while meeting regulatory compliance requirements such as watermarking for synthetic speech.

-

SoundHound AI: Differentiates through natural language-first platforms and voice commerce capabilities. The company’s recent agentic launches and integration of vision features position it as a contender for OEMs seeking richer, transactional voice experiences.

-

OEM adopters and integrators (examples: Kia, Lucid, BYD): These OEMs are moving from supplier evaluation to embedded deployments of generative voice assistants as part of broader cockpit strategies. Partnerships with platform vendors enable rapid rollouts but also create new expectations around updates, multilingual support and lifecycle governance.

-

NVIDIA and platform partners: Semiconductor and AI framework vendors are accelerating developer-friendly stacks (e.g., embedded ASR toolkits and NeMo frameworks) that reduce integration friction for Tier 1s and OEMs opting to control more of the stack in-house.

Across the competitive set, the difference between winning and losing is increasingly determined by three capabilities: (1) robust on-device ASR for noisy environments, (2) modular APIs that enable OEM-specific integrations and UX customization, and (3) demonstrable compliance and security controls.

Report contents — practical takeaways we deliver

PW Consulting’s report is structured to support immediate program-level decisions, not just academic debate. Deliverables include:

-

Market sizing and forecast model (2020–2032) with scenario sensitivity for technology adoption, regulatory shocks and monetization success; baseline growth is 14.2% CAGR for 2026–2032.

-

Vendor scorecards and procurement templates: comparative assessments across technical capabilities (ASR accuracy in real-world cabin noise, NLU fidelity, on-device footprint), delivery readiness and commercial models.

-

Integration playbooks for hybrid architectures: recommended patterns for combining local ASR, privacy-preserving intent resolution and cloud-based LLM services, including sample RFP language and hardware sizing heuristics.

-

Regulatory compliance checklist: practical steps to meet EU and cross-jurisdictional requirements (metadata, watermarking, audit trails), plus governance and data retention guidance aligned with emerging best practice.

-

Monetization and partnership roadmaps: frameworks for assessing voice commerce, subscription models and aftermarket services, and guidance on partner selection to accelerate time-to-market.

-

Use-case prioritized matrix and ROI estimators for navigation, infotainment, communication and vehicle-control scenarios — designed to inform feature prioritization and hardware investment decisions.

Actionable recommendations for 2026 investments

-

Adopt a hybrid deployment roadmap: Combine on-device ASR for critical UX and privacy-sensitive flows with cloud-based augmentation for complex, agentic tasks. This reduces latency and data cost while enabling differentiated conversational features.

-

Prioritize regulatory-ready vendors: Choose suppliers who offer built-in compliance features (e.g., synthetic speech watermarking, machine-readable metadata) to reduce certification lead times and legal risk.

-

Design for modularity: Insist on modular APIs and clear upgrade paths so that improvements in generative models, ASR engines or NLU modules can be integrated without costly ECU replacements.

-

Define metrics that matter: Move beyond lab ASR accuracy; require measured performance in realistic cabin acoustics, multi-speaker tests and network-constrained environments.

-

Lock strategic partnerships early: For OEMs and Tier 1s, secure co-development terms that embed voice UX into product roadmaps and aftersales monetization paths — the window to shape standards and UX conventions is narrow.

How senior executives should use this research

-

Chief Product Officers: Use the vendor scorecards and ROI estimators to prioritize which voice capabilities to include in 2026 model-year releases and where to allocate engineering resources.

-

Head of Partnerships / Business Development: Leverage the partnership roadmaps and competitive profiles to negotiate exclusivity, co-marketing and revenue share arrangements tied to voice commerce and subscription services.

-

CISO / Legal: Apply the compliance checklist to procurement and integration standards to reduce audit friction and shorten time-to-market in regulated geographies.

-

Supply Chain / Procurement: Integrate security provenance and supplier resiliency criteria into procurement scorecards to align with recent Federal Register guidance on connected vehicle supply chains.

Closing perspective — why 2026 is a strategic inflection

Our analysis shows the automotive voice recognition market is transitioning from a feature-driven investment phase into an ecosystem where regulatory compliance, edge resilience and business model ingenuity determine winners. With the market expanding from a mid‑market baseline in 2025 and growing at a double-digit CAGR across our forecast horizon, organizations that align platform choices, legal preparedness and monetization frameworks now will secure disproportionate strategic advantage through 2032.

Next steps

This press release is a strategic preview. The full PW Consulting report contains the quantitative models, vendor scorecards, integration playbooks and contract templates needed to act immediately. For access to the complete dataset, segment-level analyses and practitioner tools referenced here, visit the report landing page or contact PW Consulting’s Automotive Practice to schedule a briefing.

For detailed analysis of this topic, please visit the official page: Automotive Voice Recognition Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.