PW Consulting Predicts 5.6% CAGR for Military Antenna Market in 2026–2032, Signaling Strong Growth Ahead

Military Antenna Market 2026: A Strategic Briefing for Decision-Makers

By PW Consulting — Senior Strategic Advisor & Lead Industry Analyst

Military Antenna Market

Executive summary

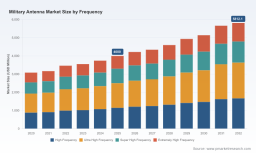

The military antenna market is transitioning from capability-driven procurement toward supply-chain-centric strategy. Our latest study — anchored on a 2025 base year and a seven‑year forecast horizon (2026–2032) — shows the sector expanding at a steady compound annual growth rate of 5.6%. The market grew from approximately USD 3.09 billion in 2020 to about USD 4.0 billion in 2025, and is projected to approach USD 5.8 billion by 2032. Those headline figures mask important inflection points: accelerating adoption of phased‑array and electronically steered apertures, growing overlap between military and commercial SATCOM requirements, and intensifying pressure on trusted supply and advanced RF component capacity.

Military Antenna Market

Why this matters for 2026 decision cycles

-

Procurement and program managers: 2026 is the year to move from tactical purchases to strategic supplier relationships. Lead times for advanced RF subsystems and qualification timelines for antenna arrays are lengthening; decisions made now will determine readiness windows in 2028–2030.

Military Antenna Market -

R&D and product leaders: technology windows are narrowing. Investments in GaN and beam‑forming capability will define competitiveness for the next platform generation.

-

Corporate development teams: the market’s steady growth creates M&A and partnership opportunities, particularly among specialized antenna houses, trusted foundries, and systems integrators that bridge airborne, maritime, and space use cases.

Market trajectory and the strategic implications

Our consolidated market model (historical 2020–2025; forecast 2026–2032) confirms steady expansion with low‑to‑mid single‑digit CAGR. That trajectory reflects two overlapping trends: an enduring defense modernization cycle in allied markets and an expanding addressable market from commercialized satellite services and unmanned systems. For strategy teams, the key implication is timing: slow, consistent growth reduces single‑year demand shocks but increases the cumulative opportunity for capacity investors and early technology adopters.

Demand drivers and technology trends

-

Phased arrays and electronic steering: force multipliers in EW, airborne survivability, and multi‑mission platforms. The trend toward distributed apertures and modular arrays increases design complexity and qualification burdens, but also raises value capture for suppliers who can deliver integrated RF subsystems.

-

GaN-based RF ecosystems: GaN on SiC is shifting the performance frontier for high-power, high-efficiency transmitters used in active arrays and anti‑jam GPS mitigations. Anticipated wafer, foundry, and packaging constraints create a tangible supply risk for firms that fail to secure capacity or trusted suppliers.

-

SATCOM convergence: military demand increasingly leverages commercial Ka/Ku bands and high-throughput LEO constellations. Certification and multi‑orbit qualification are now prerequisites for long‑term SATCOM roadmaps.

-

Miniaturization for unmanned systems: compact, wideband, and low‑SWaP antennas are now mission‑critical for UAVs and autonomous naval sensors, shifting a portion of demand to specialized manufacturers and custom contract work.

Supply‑chain and regulatory landscape — primary risks

-

Export controls and procurement sovereignty: recent regulatory changes have altered exportability for certain advanced reception pattern antennas. While some devices moved from a munitions‑list regime to export administration oversight, export‑control complexity remains a persistent source of delivery delay for sensitive apertures integrated with platform electronics.

-

ITAR and sovereign procurement bottlenecks: allied integration schedules are still affected by national sourcing rules and certification lags. These governance constraints reduce elasticity in global sourcing and slow the pace at which multinational programs can consolidate suppliers.

-

Component‑level pressure: tariffs and trade restrictions have materially increased the cost and lead time of key subcomponents — RF modules, connectors, PCB assemblies — and elevated the cost of cross‑border sourcing strategies.

-

Advanced materials scarcity: rising demand for GaN-on‑SiC wafers and related packaging services places strategic value on trusted foundry relationships and capacity reservation agreements.

Competitive landscape — who matters and why

The market features a mix of specialized antenna manufacturers, systems integrators, and legacy industrial suppliers. The competitive map can be read as four clusters: precision RF specialists, high‑volume commercial crossover vendors, platform‑integrated systems houses, and regional niche players. Key names we analyzed include established U.S. antenna manufacturers with broad military portfolios, specialized RF designers from Europe and Israel with strong airborne and UAV focus, and emerging high‑performance wideband suppliers from South Asia.

-

Legacy U.S. manufacturers continue to win platform and logistics contracts due to field heritage, aftermarket support networks, and integration experience.

-

Specialist designers — especially those with beam‑forming and anti‑jam GPS IP — are capturing premium program slots for unmanned and airborne applications.

-

Regional manufacturers are increasingly relevant for sovereign procurement strategies and rapid prototyping contracts where localization matters.

Recent commercial activity underscores these dynamics: manufacturers have secured targeted contracts for airborne and surface electronic warfare programs, new factory investments have expanded regional production footprints, and several firms closed small‑to‑mid‑sized defense contracts for UAV and anti‑jamming solutions. Collectively, these moves signal a market where capability specialization and supply reliability are being rewarded over simple price competition.

What our full report delivers — operationally focused contents

PW Consulting’s full Military Antenna Market report is built for 2026 decision cycles. It combines strategic narrative with operational playbooks that procurement, product, and corporate development teams can act upon immediately. Highlights include:

-

Actionable market-sizing with scenario modelling: baseline, rapid‑adoption, and constrained‑supply scenarios calibrated to procurement calendars and technology adoption curves.

-

Supplier scorecards and qualification playbooks: standardized evaluation matrices covering design maturity, qualification timelines, trusted‑source certifications, and lifecycle support commitments.

-

Technology roadmaps and investment triggers: clear gate criteria for GaN capacity investments, phased‑array demonstrators, and multi‑orbit SATCOM certification programs.

-

Procurement and pricing simulations: exercise models for multi‑year contracts, inventory hedging, and dual‑sourcing strategies to mitigate tariff and export‑control shocks.

-

M&A and partnership shortlist: diligence-ready profiles of acquisition and JV candidates aligned to capability gaps, cross‑border compliance, and industrial base strengthening.

-

Risk matrices: supply, regulatory, and technology risks mapped to mitigation actions, from mirrored production lines in trusted jurisdictions to pre‑negotiated foundry slots for critical RF components.

Practical recommendations for 2026 actions

-

Prioritize trusted‑source contracts for GaN and advanced packaging. If you rely on high‑power RF subsystems, secure supplier commitments now — lead times and qualification queues will extend into 2027–2029.

-

Embed export‑control strategy into RFPs. Design procurements that separate export‑sensitive subsystems and accelerate non‑sensitive integration through commercial channels to reduce hold‑ups.

-

Adopt modular architectures to shorten field upgrades. Modular antenna subsystems reduce obsolescence risk and make dual‑sourcing feasible without dramatic redesign costs.

-

Use phased investments for manufacturing capacity. Favor staged expansions and strategic partnerships with regional manufacturers to meet sovereign procurement demands without over‑committing capital.

-

Plan for qualification lead times in mission schedules. Qualification for airborne and multi‑orbit SATCOM can take multiple years; incorporate this into program milestones to avoid late‑stage delays.

-

Explore targeted M&A for capability gaps. Acquire or partner with niche beam‑forming and anti‑jam GPS specialists to accelerate capability offerings rather than building from scratch.

Conclusion — the strategic window

The military antenna market’s steady CAGR and predictable growth path create a strategic window for companies and defense acquisition authorities to shape supply architecture for the next decade. Firms that align investment with supply‑chain resilience, secure access to advanced RF materials, and build modular, certifiable antenna subsystems will convert market growth into sustained competitive advantage.

PW Consulting’s full Military Antenna Market report provides the granular, operational intelligence required to execute those moves — from supplier scorecards and procurement simulations to investment triggers and M&A shortlists. For procurement teams and strategy leaders preparing 2026 budgets and capability roadmaps, this is the moment to translate market momentum into durable program outcomes. Access to the complete dataset, segmentation analytics, and supplier benchmarking is available through our client portal.

For detailed analysis of this topic, please visit the official page: Military Antenna Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.