PW Consulting: Wind LiDAR Market Poised to Grow at a 9.3% CAGR

Wind LiDAR Market 2026: Strategic Imperatives from PW Consulting

As PW Consulting’s Senior Strategy Advisor and Head Industry Analyst, I am pleased to introduce our new market study on the global Wind LiDAR sector. Built on a rigorous base year of 2025 and a historical review covering 2020–2025, this analysis translates recent technological, regulatory, and commercial developments into concrete implications for boardrooms, project teams, and capital allocators making decisions in 2026.

Wind Lidar Market

Executive snapshot

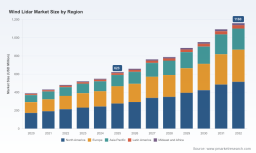

The Wind LiDAR market has moved from an early-adopter niche into an industrial-growth phase. Our topline sizing shows measured expansion from 2020 through 2025, with the market reaching USD 623 Million in 2025. Looking forward across our 2026–2032 forecast horizon, the market is projected to grow at a compound annual growth rate (CAGR) of 9.3%, reaching roughly USD 1.16 Billion by 2032. These macro dynamics reflect accelerating deployment of bankable measurement solutions, growing use of nacelle- and turbine-mounted systems for power performance, and an expanding addressable market driven by offshore applications (including floating lidar) and data-service monetization.

Wind Lidar Market

Why this report matters for 2026 decision-making

- Strategic capital allocation: Project developers, wind turbine OEMs, and asset owners must now plan capital and operating budgets that assume continuous growth in LiDAR adoption. The 9.3% CAGR embedded in our forecast translates into materially higher demand for both hardware and lifecycle services over the coming investment cycles.

- Bankability and financing: Lenders and insurers increasingly treat LiDAR-validated wind resource datasets as a de‑risking input. Recognizing which systems and service arrangements meet bankability standards will directly influence cost of capital on new projects.

- Procurement and supply chain: Procurement teams should adopt multi-year sourcing strategies that reflect capacity expansions and product roadmaps—decisions made in 2026 will affect delivery and O&M risk profiles through the next wind build cycles.

- Product and service strategy: Technology vendors and data service providers need to prioritize product lines and commercial models (hardware sales, managed services, data subscriptions) that align with shifting buyer preferences for turnkey, certifiable measurement solutions.

Core market dynamics and their strategic implications

- Standards and bankability are converging: The publication of IEC TS 61400-50-4 (2025) for floating systems and ongoing IEC and IEA working groups are accelerating acceptance of LiDAR-derived datasets in offshore and floating wind project underwriting. Firms that align early with these norms will gain privileged access to project pipelines where financiers demand “IEC-grade” evidence.

- Product innovation is rapid and focused: Recent product launches have extended measurement ranges and improved portability while lowering maintenance costs. These advances create a two-track market: high-specification devices priced for bankable, long-term projects and compact systems tailored for routine site reconnaissance and O&M analytics.

- Verticalization and services monetization: Data-as-a-service players and analytics providers are bundling LiDAR measurements with atmospheric modelling and AEP (Annual Energy Production) uncertainty analytics. This is changing procurement from being hardware-centric to outcome-centric, raising the value of proprietary analytics and validated measurement pipelines.

- Manufacturing scale and localization: Suppliers investing in capacity expansion and regional manufacturing are reshaping lead times and total landed cost. Buyers should incorporate supplier capacity and logistics in tender evaluations to avoid schedule risk during peak build periods.

- Market concentration and room for consolidation: The market exhibits a moderate concentration at the top tiers, leaving meaningful opportunity for strategic partnerships, niche specialization, and M&A among mid-tier suppliers and service integrators.

Competitive landscape — who to watch and why

Our vendor analysis profiles established electro-optical specialists, industrial sensor OEMs, and high-volume manufacturers that are driving both technology innovation and commercial scale. Key themes emerge across vendors: product differentiation (pulsed vs. continuous-wave), deployment focus (nacelle, ground-based, offshore/floating), and the degree to which companies offer integrated services versus stand‑alone hardware.

Wind Lidar Market

- ZX Lidars (Malvern, UK): A technical leader in continuous‑wave and pulsed systems that has moved the bankability conversation forward with recent product rollouts validated against IEC classification. ZX’s emphasis on performance validation at independent test sites positions it strongly with developers prioritizing “zero‑uncertainty” measurement claims.

- Vaisala Oyj (Vantaa, Finland): A long-standing provider whose WindCube family is frequently referenced in bankable offshore projects. Vaisala’s product line and services emphasize validated power performance testing and nacelle-mounted solutions, making it a preferred vendor where AEP certainty is a financing precondition.

- HALO Photonics / Lumibird (Chepstow, UK): Focused on ruggedized pulsed systems and compact footprint designs, this group is advancing scanning and long-range capabilities. Their releases target boundary-layer meteorology and wind energy markets where ease of deployment and low maintenance are critical.

- METEK GmbH (Elmshorn, Germany): METEK’s profiling and turbulence-capable systems are designed for detailed atmospheric characterization. Their combined hardware and scientific pedigree make them relevant for applications where turbulence, shear, and high-resolution profiling inform turbine selection and micrositing.

- Nanjing Movelaser Co., Ltd. (Nanjing, China): High-volume production and aggressive cost-positioning, combined with IEC/DNV certifications and OEM partnerships, make Nanjing Movelaser a pivotal player in driving commoditization of ground‑based and nacelle systems—particularly where price-sensitive, large-scale deployments are planned.

- Windar Photonics A/S (Taastrup, Denmark): A specialist in nacelle-mounted sensors with tangible installed-base penetration in certain OEM fleets. Their recent capacity increases and commercial traction illustrate a strategy of deep integration with turbine OEMs and fleet-level performance monitoring.

Collectively, the competitive set is differentiated by technology architecture, bankability pedigree, and ability to deliver lifecycle services. Our analysis indicates a market where partnerships (OEMs + lidar vendors + analytics providers) and certification credentials will often trump pure price competition in projects where financing leverage is material.

What the PW Consulting report contains (practical, decision‑ready content)

This study is structured to support immediate 2026 decisions. Key deliverables include:

- Topline market sizing and directional forecasts (base year 2025, historical 2020–2025, 2026–2032 projection frameworks).

- Regulatory and standards landscape, including interpretation of IEC TS 61400‑50‑4 and implications for floating projects, plus certification pathways favored by financiers and certification bodies.

- Vendor scorecards and comparative capability matrices (technology, bankability evidence, service models, scale), designed to support shortlist creation for RFPs.

- Procurement playbooks: RFP templates, evaluation scoring, commercial terms to prioritize (warranty, data rights, service SLAs, performance validation), and negotiation levers tied to volume and multi-year commitments.

- Use-case driven TCO models and sensitivity analyses for onshore, offshore, nacelle, and service-only scenarios—built to be repurposed for your portfolio’s specific risk and return assumptions.

- Strategic options and M&A screening: criteria for vertical integration, joint ventures with data providers, and acquisition targets to rapidly build capability.

In keeping with the “trailer” approach of this press release, detailed segment tables and granular split‑outs by region, type, and application are summarized in the full report and not reproduced here; prospective users are encouraged to consult the full dataset for procurement- and investment-grade figures.

Actionable recommendations for leadership in 2026

- Embed LiDAR validation in early-stage commercial due diligence for any project greater than your firm’s self‑retained risk threshold; require IEC-or-equivalent validation where finance is sought.

- Adopt a multi-vendor sourcing stance for hardware and data services to mitigate single-supplier capacity risk during construction peaks.

- Negotiate data rights and analytics access as part of hardware purchases—vendor lock-in through proprietary analytics can materially affect long-term O&M costs and optimization opportunities.

- Prioritize partners with demonstrated certifications and independent test validation if the project requires bankable datasets—this reduces AEP uncertainty and improves financing terms.

- For technology investors and OEMs: evaluate acquisitions or JV structures that grant faster access to validated LiDAR datasets and analytics capabilities rather than building in-house from scratch.

- Monitor standards and certification developments closely—alignment with the latest IEC and DNV guidance should be a gating criterion in vendor selection and product roadmaps.

Next steps and how to access the full study

PW Consulting’s Wind LiDAR Market Report offers the full dataset, vendor scorecards, procurement tools, and bespoke advisory engagements to convert these insights into executable plans. The press release level overview intentionally omits the granular subsegment tables and the full competitive scoring matrix to preserve the commercial utility of the complete report. For access to the full report, enterprise briefings, or an executive workshop tailored to your portfolio, please contact PW Consulting via our website to schedule a private briefing.

In a market expanding at a sustained mid‑single‑digit to high‑single‑digit CAGR and evolving standards around bankability and floating applications, 2026 will be the year that separates tactical adopters from strategic leaders. The decisions you make now—on vendors, certification evidence, procurement contracts, and data strategies—will materially shape your exposure, returns, and operational flexibility across the next wave of wind deployment. PW Consulting stands ready to translate our analysis into the decision support tools your team needs.

For detailed analysis of this topic, please visit the official page: Wind Lidar Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.