PW Consulting: Lawn Mower Market to Expand from USD 215.0 Million in 2025 to USD 325.35 Million by 2032, Driven by 6.1% CAGR

Lawn Mower Market 2026 Outlook: Strategic Imperatives for Growth and Resilience

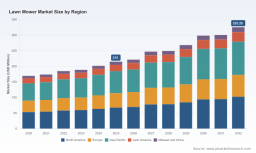

PW Consulting’s latest Lawn Mower Market report — base year 2025, forecasting through 2032 — delivers actionable intelligence for executives preparing strategic plans in 2026. The market has shown steady expansion from USD 169.5 Million in 2020 to USD 215.0 Million in 2025, and our model projects continued momentum to USD 325.35 Million by 2032. This trajectory corresponds to a 6.1% compound annual growth rate (CAGR) over the 2026–2032 forecast period and reflects sustained demand across product innovation, electrification, and service-led monetization.

Lawn Mower Market

Why this report matters for 2026 decision cycles

-

Timing: 2026 is a pivot year when regulatory pressure, component cost inflation, and accelerating technology adoption converge — creating windows for market share shifts and margin compression. Boards and C-suites need a multi-layered plan that balances capex discipline with targeted innovation.

Lawn Mower Market -

Clarity on concentration: The market shows meaningful concentration among top suppliers (CR3 ~65.4%, CR5 ~78.2%), which creates both stability at scale players and opportunity for nimble challengers to exploit niche performance or go-to-market gaps.

Lawn Mower Market -

Risk-informed growth: Our scenario-based forecasts quantify upside from accelerated electrification and downside from raw-material price shocks and tightening regional emission regulations — helping firms stress-test investment cases for product launches, factories, and M&A.

Macro and demand dynamics to watch in 2026

-

Electrification and autonomy are no longer niche: Battery-powered and robotic mowers are moving from early-adoption to mainstream purchase consideration, altering the product lifecycle and after-sales economics. Firms that combine platform batteries, service plans, and software capabilities will capture higher lifetime value.

-

Regulatory tightening is a market shaper: Federal and state-level rules — including the CPSC’s ongoing safety standard activities and harmonized test standards such as ANSI/OPEI B71.8 — raise the compliance bar for manufacturers. Local measures restricting gasoline use during high-ozone months are materially altering seasonal demand patterns and product feature priorities.

-

Input-cost volatility: Steel and electronic component prices remain elevated relative to pre-pandemic baselines, pressuring margins and driving supplier consolidation or reshoring discussions. Firms should prioritize supply-chain visibility and strategic hedging for critical inputs.

-

Services as margin lever: With hardware becoming more commoditized, recurring revenues from subscription-based battery services, preventive maintenance, and SaaS-enabled fleet management will be decisive for sustaining gross margins.

Competitive landscape — positioning and strategic moves

Our competitive assessment synthesizes capability and strategic posture across legacy OEMs, power-tool conglomerates, specialized commercial manufacturers, and fast-growing battery-native entrants.

-

The Toro Company (Bloomington, Minnesota): A long-standing leader with deep commercial and residential portfolios. Strengths include product breadth and dealer networks; strategic priorities are professionalization of service offerings and further integration of battery platforms.

-

Deere & Company (Moline, Illinois): Durable brand equity in riding and zero-turn segments with rigorous manufacturing scale. Deere’s playbook emphasizes reliability and dealer-led distribution — advantages for institutional landscaping accounts.

-

Husqvarna Group (Stockholm, Sweden): Early mover in robotic mowers and battery ecosystems; Husqvarna’s R&D orientation and software investments position it well for consumer automation adoption.

-

Stanley Black & Decker / Cub Cadet (New Britain, Connecticut): Strength in homeowner-focused riding solutions and channel leverage; their challenge is scaling service and telematics to match competitors that are already embedding software into product roadmaps.

-

Metalcraft of Mayville / Scag (Mayville, Wisconsin): A commercial-focused manufacturer that competes on durability and dealer relationships — an attractive target for buyers seeking high-margin B2B exposure.

-

EGO Power+ (Naperville, Illinois): A battery-native challenger that illustrates how chemistry, powertrain design, and go-to-market agility can erode incumbent product advantages in key segments.

Collectively, the leading players’ dominance (see concentration metrics) creates a predictable competitive backdrop — but it also reveals white space for companies that can combine fast product iteration, strong channel activation, and aftermarket services.

Strategic playbook for 2026 (what winners will do)

-

Prioritize platformization: Invest in modular battery and electronics platforms that can be shared across walk-behind, ride-on, and robotic lines to realize scale, reduce time-to-market, and simplify regulatory testing.

-

Operationalize compliance: Convert regulatory monitoring into a formal product gating process. Anticipate CPSC test and certification timelines and embed compliance checkpoints into R&D sprints to avoid costly recalls or launch delays.

-

Hedge supply risk with strategic sourcing: Move beyond tactical procurement to partnership agreements with cell suppliers and critical component manufacturers. Consider localized buffer capacity for steel and precision electronic parts to protect manufacturing continuity.

-

Monetize services: Launch subscription models for batteries, remote diagnostics, and preventive maintenance, with differentiated tiers for residential and commercial clients to capture recurring revenue and higher customer lifetime value.

-

Recalibrate channel economics: Incentivize dealers around uptime and service KPIs rather than unit sales; create shared success metrics that align dealer margins with lifecycle revenue.

-

Pursue focused M&A: Use bolt-on acquisitions to secure battery IP, telematics firms, or last-mile service providers — targeting capabilities that accelerate time-to-value and are accretive to aftermarket margins.

Regulatory and policy implications — immediate actions

-

Monitor CPSC and standards bodies: The CPSC’s ongoing engagements around walk-behind safety and the ANSI/OPEI standards are likely to reshape product test plans. Engage with standards committees and certify early to avoid market access delays.

-

Prepare for regional restrictions: Jurisdictions implementing seasonal restrictions on gasoline-powered equipment require fast-follower product strategies (e.g., swap-in batteries or hybrid options) and targeted marketing by geography and season.

-

Document compliance as a commercial asset: Use certification and validated test data as a differentiator for large commercial contracts and public procurement processes.

Operational and go-to-market playbooks included in the report

PW Consulting’s full report is structured as an executive-grade toolkit for 2026 planning cycles. Highlights include:

-

A probabilistic market model (2026–2032) with scenario toggles for regulatory stringency, raw-material shocks, and accelerated electrification.

-

Competitive heatmaps and capability matrices for incumbent OEMs and challengers, covering R&D, distribution reach, and software maturity.

-

Operational playbooks: supplier-risk heatmaps, fixed-cost levers, product launch checklists that integrate compliance testing timelines, and dealer incentive designs tied to aftermarket performance.

-

M&A screening templates and valuation sensitivities for targets across battery tech, telematics, and service platforms.

-

Commercial frameworks for subscription offerings, including churn assumptions, pricing bands, and break-even analyses under varying adoption scenarios.

To preserve the discovery value of the research, detailed segment-level breakdowns and proprietary assumptions are accessible in the full report — intentionally withheld here to invite deeper engagement with our analysts.

Near-term market signals and events (what to watch in 2026)

-

Industry trade shows and product unveilings: Major equipment expos scheduled in 2026 will spotlight next-generation commercial-grade mowers, battery systems, and automation tools — a primary source of observable product and channel strategies.

-

Regulatory filings and standards reaffirmation: Look for public comments and rulemaking on blade-contact safety and emissions, as these will affect testing costs and go-to-market calendars.

-

Input-price indicators: Producer Price Index trends for steel and electronic components will be an early warning of margin pressure and potential pricing cycles.

How PW Consulting can accelerate your 2026 planning

Executives can leverage our syndicated market model and bespoke strategy workshops to compress the time between insight and action. Typical engagements we run for clients in this sector include:

-

Scenario-driven portfolio optimization (3–5 weeks): Reallocating R&D and capex under downside and upside market cases.

-

M&A target prioritization (4–6 weeks): Identification and commercial diligence for battery, telematics, and service targets.

-

Channel redesign and dealer economics (6–8 weeks): Realignment of distribution incentives and service KPIs to drive aftermarket penetration.

Next steps — where to find the full intelligence

This release outlines the strategic contours and operational priorities that will define winners and laggards in 2026. For the complete dataset, proprietary segment analysis, and the downloadable market model with scenario toggles, please consult the full Lawn Mower Market report available from PW Consulting. Our analysts are also available for briefings to walk through tailored implications for your portfolio or board presentation.

PW Consulting — helping leaders in lawn and garden equipment translate market dynamics into decisive, risk-calibrated strategies for 2026 and beyond.

For detailed analysis of this topic, please visit the official page: Lawn Mower Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.