PW Consulting Forecasts 11.2% CAGR for Global Cell Culture Market through 2032

Cell Culture Market 2026 Outlook: Strategic Imperatives for Bioprocess Leaders

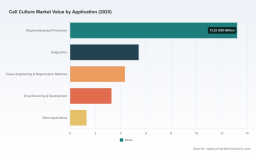

Executive summary

PW Consulting's latest Cell Culture Market report (base year 2025) reframes how executive teams should approach portfolio, manufacturing and go-to-market choices in 2026. Our macro-analysis shows a market that has grown from a mid‑teens billion-dollar base in 2020 to an estimated USD 27.6 billion in 2025, and is poised to expand at a compound annual growth rate (CAGR) of 11.2% across the 2026–2032 forecast window. By the end of that horizon the global market is modeled to roughly double from the 2025 base, driven by accelerating demand in advanced biologics, cell and gene therapy manufacturing, and higher-value research workflows.

Cell Culture Market

Why this matters for 2026 decisions

- Timing and scale. The market dynamics modeled in our report make 2026 a hinge year: regulatory clarity, process intensification, and productization of cell therapy manufacturing are converging to create windows of differentiated value capture that will narrow rapidly.

- Concentration and competitive thresholds. The market exhibits a moderate-to-high vendor concentration profile (CR3 ~50.3%; CR5 ~68.4%), indicating that leading suppliers retain pricing and access advantages — but also that meaningful share gains are achievable for well-executed entrants and M&A-backed challengers.

- Risk-adjusted investment. Our scenario work shows that investments in resilient supply chains, GMP capability upgrades, and platform media with clear performance claims deliver the best risk‑adjusted returns in a regulatory environment that favors flexible CMC approaches.

What the report delivers (practical, actionable content)

- Robust market sizing and trend maps anchored to 2025, with forward-looking forecasts through 2032 under multiple scenarios (base, accelerated, and downside).

- Value‑chain and margin diagnostics that reveal where capture is concentrated today — and where margin pools will migrate as biologics manufacture moves from bench to commercial scale.

- Commercial playbooks: go-to-market blueprints for incumbents and new entrants (direct sales vs. distribution, partnership models, and digital enablement for consumables and equipment).

- Supplier and raw-material risk assessment, including proprietary stress tests that quantify disruption exposure for critical media components and sterile consumables.

- Regulatory and quality readiness checklist keyed to recent FDA, EMA, and EU developments, translated into capital-expenditure and compliance roadmaps.

- Deal and partnership landscape, with M&A, licensing, and JV targets prioritized by strategic fit and integration complexity.

- Detailed vendor profiles and competitive positioning on technology, commercial reach, GMP footprint, and innovation pipelines.

Competitive landscape — who matters and why

Industry leaders continue to span legacy life‑science conglomerates, specialized media houses, and agile medium‑sized suppliers. The report includes in-depth, comparable profiles of the companies that shape the market today and are likely to define it tomorrow. Highlights:

Cell Culture Market

- FUJIFILM Irvine Scientific (Irvine, CA) has strengthened its presence across research and production-grade media, increasingly leveraging partnerships and platform productization to move from RUO to commercial offerings. Recent strategic collaborations and platform launches in 2026 demonstrate a playbook focused on end-to-end customer workflows.

- Thermo Fisher Scientific (Waltham, MA) remains a dominant integrated supplier with an expansive Gibco portfolio across mammalian, stem and 3D culture needs. Their scale and channel breadth continue to be a barrier for many niche players, but also create opportunities for targeted partnerships where flexibility or customization is required.

- Merck KGaA (MilliporeSigma) (Darmstadt) and Sartorius AG (Göttingen) both play critical roles in supplying GMP‑capable materials and process technologies. Their global production footprints and certified facilities support large-scale biologics programs and place them at the center of industrialization plays.

- Corning, Lonza, PromoCell, STEMCELL Technologies and Cell Biologics represent distinct but complementary strategic archetypes: Corning and Lonza bring scale and integrated manufacturing capabilities; PromoCell and STEMCELL focus on niche, high‑value research and therapy segments; Cell Biologics targets specialized xeno‑free solutions for primary and stem cell workflows.

- Across the set, recent moves — from PromoCell’s entry into GMP services to FUJIFILM’s cross-border collaborations in AAV production — underscore a theme: downstream manufacturing needs are driving upstream product innovation and commercial partnerships.

Regulatory and operational headwinds — and how to respond

The regulatory environment is shifting in ways that materially affect CMC strategy and speed to clinic. Key developments embedded in our analysis include:

Cell Culture Market

- FDA’s finalized flexible CMC approach (effective January 2026) and subsequent draft guidance in mid‑2026, which reduce time‑to‑clinic for small patient-population therapies but increase the importance of demonstrable control strategies and supplier qualification.

- EMA guidance that clarifies microbial purity and GMP expectations for reagents used in biological medicinal products, increasing documentation and supplier audit requirements.

- Full applicability of EU GMP Annex 1 since 2024, sustaining elevated activity in contamination control and sterile operations.

- Persistent supply challenges: variability in raw material quality and episodic supply-chain disruptions continue to impact manufacturing efficiency and batch yields across both R&D and commercial operations.

For 2026, management teams should prioritize supplier qualification programs, dual-source strategies for critical inputs, and investments in QC analytics that can turn raw‑material variability into a managed, measurable parameter rather than an unpredictable cost center.

Strategic plays that win in 2026

- Product-platform specialization: Move beyond “one-size-fits-all” media. Differentiated, application‑specific formulations for cell therapy, AAV production, and perfusion bioprocesses command premium pricing and tighter customer lock‑in when paired with technical support and scale-up services.

- GMP-enabled vertical moves: Firms that can credibly offer GMP‑grade media and custom formulation services (or partner tightly with those who do) will shorten commercialization timelines for customers and capture a larger share of lifecycle spend.

- Service-led commercialization: Bundling media/equipment with analytics, process transfer support, and contract development drives higher lifetime value and mitigates price erosion in commoditized segments.

- Resilient sourcing and modular manufacturing: On-shore or near‑shore capacity for critical, sterility-sensitive items combined with modular cleanroom investments reduces lead times and regulatory friction when scaling commercial production.

- Selective M&A and partnerships: Targets offering unique formulations, regional GMP capacity, or niche customer relationships are high-impact, low-effort ways to augment capability without long organic timelines.

How PW Consulting’s report supports board-level decisions

The report is structured to move quickly from insight to decision. Boards, strategy teams and commercial leaders can use our deliverables to:

- Prioritize capex and R&D allocation according to quantified margin pools and 2030+ scenario outcomes.

- Construct supplier‑risk heatmaps that feed into procurement KPIs and contingency planning.

- Identify and size acquisition targets using our deal-sourcing framework and integration playbooks.

- Define commercial contracts and channel strategies that capture more value per customer through bundled services and lifecycle partnerships.

Closing — the 2026 moment

2026 represents a strategic inflection point for players across the cell culture ecosystem. Regulatory flexibility and rising commercial demand are creating the technical and commercial conditions for significant value migration. The companies that act decisively — aligning productization, supply resilience and regulatory readiness — will be able to convert market growth into durable competitive advantage.

PW Consulting’s Cell Culture Market report supplies the market architecture, competitive intelligence and executable playbooks executive teams need to make those decisions with confidence. For licensing, sample pages, and access to our proprietary segmentation tables and supplier pricing models, contact PW Consulting or visit our official report page to obtain the full dataset and appendices.

For detailed analysis of this topic, please visit the official page: Cell Culture Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.