PW Consulting: USB Wall Charger Market to Reach USD 2,096.49 Million by 2032, Growing at a 3.9% CAGR (2026–2032)

USB Wall Charger Market 2026: Strategic Imperatives from PW Consulting’s New Industry Report

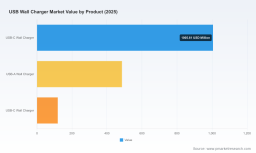

PW Consulting today releases its comprehensive industry briefing on the USB wall charger market, built to inform executive decisions across product, supply chain, regulatory and M&A agendas for 2026 and beyond. Grounded in a detailed historical analysis (2020–2025, base year 2025) and forward-looking forecasts through 2032, the report blends a proprietary market model with pragmatic, executable recommendations. The market we modelled reached approximately USD 1,610.8 Million in 2025 and is forecast to expand to about USD 1,729.4 Million in 2026, tracking a compounded annual growth rate (CAGR) of 3.9% over the 2026–2032 forecast window and reaching over USD 2,096 Million by 2032.

USB Wall Charger Market

Why this report matters for 2026 strategy

-

Timing matters: 2026 is an inflection year for both product rules and component availability. Regulatory, standards and silicon roadmaps converge this year, creating windows of opportunity and periods of elevated compliance risk.

USB Wall Charger Market -

Technology diffusion drives commercial differentiation: GaN power stages, multi‑port PD implementations and integrated hub/charger architectures are shifting value away from legacy single‑port designs to higher‑margin system solutions.

USB Wall Charger Market -

Consolidation and specialization are simultaneous forces: market concentration metrics point to a moderately fragmented supplier landscape where both scale and niche engineering capability win deals—especially in premium and regulated segments.

Key market dynamics shaping 2026 decisions

-

Standards and regulation: The EU common charger directive and evolving USB Power Delivery specifications materially change product roadmaps. The directive’s phased scope expansion through 2026 raises mandatory USB-C requirements for more device classes; concurrently, the USB‑IF has extended compliance grace periods into late 2026 for certain silicon generations. These two forces create a transitional window in which legacy and next‑gen designs coexist—an important tactical period for product launches and inventory decisions.

-

Component and BOM pressure: The adoption of GaN and higher-wattage PD controllers has altered unit economics. Our contract-manufacturer BOM benchmarking highlights material differentials across common casing materials and chassis choices—small per-unit differences that compound at high volumes and should inform sourcing and value‑engineering initiatives.

-

Platformization of charging: Reference designs and integrated silicon (controller ICs and powerstage modules) enable OEMs to accelerate time-to-market and reduce engineering risk. Reference designs targeted at high‑wattage and multi‑port applications are enabling adjacent product plays (portable stations, e-bikes, power banks) and opening white‑label opportunities for non‑traditional power suppliers.

Report contents — what executives will get

-

Market model with transparent assumptions: historical series (2020–2025), base‑year calibration and a scenario-based forecast (2026–2032) with sensitivity levers for technology adoption, regulatory ramp and component pricing.

-

Delivery‑oriented playbooks: product specification templates, BOM benchmarking (including casing material cost bands), supplier scorecards, and a channel strategy matrix designed for both direct-to-consumer and B2B OEM sales motions.

-

Competitive and technology landscape: vendor dossiers, reference‑design tracking, IP and standards risk mapping, and go/no‑go decision frameworks for GaN, multi‑port PD and integrated hub designs.

-

M&A and partnership intelligence: an evaluated shortlist of targets and partners by strategic fit, engineering capability and go-to-market synergies, plus valuation sensitivity based on consolidation scenarios.

-

Regulatory compliance playbook: product certification timelines, testing checklists and mitigation options calibrated to the USB‑IF compliance revisions and the EU common charger implementation timeline.

Competitive landscape — where incumbents and challengers stand

-

Anker Innovations: Strength in branded multi‑port GaN chargers and consumer recognition. Anker’s PowerIQ ecosystem and emphasis on higher‑watt PD products position it strongly in premium and travel categories.

-

Belkin International: Leverages channel relationships and a long-standing OEM/retail presence. The BoostCharge series and GaN lineups are engineered for mainstream retail and enterprise accessory programs.

-

Aukey, Ugreen and Baseus: Fast followers from Shenzhen with aggressive price-performance roadmaps. These manufacturers combine GaN adoption with modular multi‑port architectures and, in some cases, hub integration to capture adjacent accessory spend.

-

RAVPower and Mophie (ZAGG): Brands that trade on reliability and mobile optimization. Their product portfolios emphasize mobile device fast charging and curated retail placement.

-

Phihong: A distinct position in regulated, medical‑grade AC‑DC chargers—an attractive niche if your strategy targets professional equipment or highly regulated end markets.

-

Semiconductor leaders (Texas Instruments, STMicroelectronics): These firms are strategic enablers. New controller ICs and reference designs compress development cycles and raise the technical baseline for premium charger designs. Their roadmaps effectively dictate what is feasible for OEMs on cost, features and compliance timing.

Recent product and standards developments to watch

-

Controller and reference design cadence: STMicroelectronics’ introduction of a hybrid USB PD sink controller and Texas Instruments’ integrated high‑wattage charger reference designs materially lower engineering risk for premium designs—accelerating the timeline for multi‑port, high‑power chargers.

-

USB‑IF updates: The recent compliance specification revision and extended grace period create both breathing room and a deadline for silicon and product qualifications—firms must map their certification paths now to avoid forced rework later in 2026.

-

Regulatory impacts: The EU common charger law’s extension to portable computers and its prior handset coverage affect product portfolios and market access decisions. The directive’s projected e‑waste savings underscore the policy’s durability and the inevitability of USB‑C standardization.

Strategic playbook for 2026 (practical actions)

-

Product roadmap prioritization: Defer low‑margin legacy SKUs with high compliance risk; accelerate GaN and PD‑capable SKUs that leverage reference designs or proven controller silicon to reduce NRE and certification timelines.

-

Procurement and cost engineering: Re‑negotiate casing and chassis sourcing with suppliers and qualify alternate materials. Our BOM benchmarks show small per‑unit casing differentials that meaningfully impact unit economics at scale—make this a procurement priority.

-

Channel and go‑to‑market: Separate playbooks for CPG/retail, OEM accessory programs and B2B regulated segments. Invest in packaging and communications that emphasize certified compatibility and safety to defend premium price points.

-

Regulatory and certification: Lock in certification calendars tied to the USB‑IF update and EU timelines; build contingency inventory where needed for products approaching end-of-life silicon windows.

-

M&A and partnerships: Look for tuck‑ins that add GaN expertise, medical‑grade credentials, or established distribution in regions where you lack scale. Prioritize targets with clean test histories and modular product platforms.

Risk profile and scenario planning

-

Scenario A — Accelerated GaN adoption: Faster unit price deflation for GaN could pressure incumbents that rely on legacy BOMs; winners will be those who owned early reference‑design transitions and secured silicon supply.

-

Scenario B — Regulatory tightening: Stricter enforcement or shortened compliance windows increase rework and recall risk—companies with rigorous pre‑certification processes will gain share.

-

Scenario C — Component concentration: If a small set of silicon suppliers tightens allocations, pricing volatility and fulfillment risk increase—mitigation requires diversified BOMs and multi‑source qualification.

What PW Consulting’s dashboard unlocks

-

Proprietary dashboards let you toggle assumptions and view revenue, ASP and volume outputs across scenarios—enabling board‑level what‑if modeling without exposing the underlying confidential splits in this release.

-

Executive briefings and custom workshops focused on product portfolio choices, supplier negotiations and acquisition screening—built to convert insight into prioritized 90‑day roadmaps.

PW Consulting’s new USB Wall Charger Market report is engineered to be directly actionable for 2026 planning cycles: it pairs a validated market model (base year 2025, forecast 2026–2032 with a 3.9% CAGR) with execution playbooks that reduce certification and time‑to‑market risk while optimizing unit economics. For procurement, product and corporate development leaders preparing budgets and roadmaps this year, the intelligence in this report translates into concrete levers you can pull now to shape outcomes through 2026 and into the next expansion phase.

To access the full dataset, segmentation splits, vendor scorecards and downloadable scenario dashboards, visit PW Consulting’s report page or contact our industry team for a tailored executive briefing. The public summary above demonstrates the analytical depth and the operational orientation of our work while directing decision-makers to the full dataset required for rigorous planning.

For detailed analysis of this topic, please visit the official page: USB Wall Charger Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.