PW Consulting: Oligonucleotide Pool Library Market to Expand from USD 1,875.0 Million in 2025 to USD 4,205.6 Million by 2032 at a 12.35% CAGR

Oligonucleotide Pool Library Market — Strategic Imperatives for 2026

Executive summary

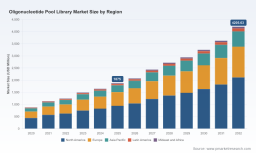

As oligonucleotide-enabled research and therapeutic pipelines accelerate, the oligonucleotide pool library market is entering a phase of sustained expansion and strategic bifurcation. Our latest market study finds the industry reached an estimated USD 1,875 million in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 12.35% through the forecast window, reaching roughly USD 4.2 billion by the end of the decade. For business leaders planning 2026 investments, partnerships, or M&A activity, the implications are clear: growth opportunity coexists with operational fragility—opportunities that require calibrated playbooks, not generic optimism.

Oligonucleotide Pool Library Market

Why this report matters for 2026 decision-making

- Timing of inflection: 2026 will be a pivotal execution year for companies that have product-market fit, scalable manufacturing, and risk-mitigated supply chains. The market momentum observed through 2025 translates into concrete capacity and commercialization choices in 2026.

- Regulatory tightening: New regulatory guidance and agency initiatives are reshaping acceptable manufacturing and quality frameworks for synthetic oligos; firms without dedicated compliance investments risk delayed commercialization or costly rework.

- Cost and supply volatility: Raw material dynamics and upstream concentration in key chemistries introduce short- and medium-term margin pressure; pricing strategies deployed in 2026 will determine competitive positioning for years.

- Strategic differentiation: Technical platform, application focus (e.g., CRISPR design, target capture, library prep), and integration with downstream workflows will separate winners from followers. Our report equips leaders to choose the right lane.

Market trajectory and drivers

The sector’s headline growth is driven by expanding demand across research genomics, drug discovery screening, and therapeutic development. Technological advances—higher-throughput array and chip-based synthesis, improved error correction, and tailored pool chemistries for CRISPR and NGS workflows—are increasing both the addressable use cases and per-sample value. Demand-side tailwinds include larger-scale CRISPR screens, proliferation of targeted sequencing assays, and growth in synthetic biology applications.

Oligonucleotide Pool Library Market

Despite the rapid expansion, structural characteristics matter: the market combines pockets of high technical entry barriers with broad demand from academic, biotech, and pharmaceutical customers. That mix produces opportunities for specialists and for vertically integrated suppliers who can bundle design, synthesis, and downstream analytics.

Oligonucleotide Pool Library Market

Dynamics shaping 2026

- Raw material and COGS sensitivity: Phosphoramidite chemistry remains the backbone of most commercial synthesis routes; volatility in these inputs can immediately impact price and lead times. Firms should expect episodic cost transference to customers and must model COGS sensitivity under multiple raw-material scenarios.

- Regulatory environment: Both regional and global regulators have signalled heightened attention to oligonucleotide manufacturing controls, characterisation, and immunogenicity assessment. Companies pursuing clinical applications need to accelerate regulatory-readiness initiatives in 2026, including method validation and robust analytical reporting structures aligned to new guidance.

- Pricing and commercial noise: Pricing tiers across providers vary substantially by pool size, service level, and bundled offerings. Competitive pricing actions—whether strategic discounting or premium positioning tied to service level—are likely to intensify, making fine-grained price elasticity and segmentation analysis mandatory for 2026 commercial plans.

- Supply chain & capacity: Outsourcing patterns and the emergence of regional suppliers alter lead-time risk profiles. Organizations must prepare for capacity transfer windows and supplier dual-sourcing as part of 2026 operational planning.

Competitive landscape — who matters and why

The market is served by a mix of dedicated oligonucleotide specialists, legacy life-science suppliers, and emerging regional players. Each type brings different strategic advantages and risks for partners, customers, and investors. Below we profile the core competitive set and the strategic posture each generally represents.

- Twist Bioscience (South San Francisco): Known for array-based oligo pools and integrated synthetic biology services. Strengths include scalable chip-based synthesis and a strong positioning for gene synthesis and high-complexity pool applications. Evaluate Twist for high-throughput collaborations and platform-integrated offerings.

- Integrated DNA Technologies (IDT) (Coralville): A broad oligo and reagent portfolio with deep customer relationships in research and translational workflows. IDT is a go-to partner for customers seeking breadth of service and established QC pipelines—important for program continuity in 2026.

- Agilent Technologies (Santa Clara): Positions microarray-derived pools into targeted sequencing and in-situ hybridization workflows. Agilent’s strength is its instrumentation and assay integration, which can accelerate adoption in labs standardising around specific platforms.

- CustomArray, LC Sciences, and specialist manufacturers: These firms focus on high-throughput and custom pool manufacturing and are relevant strategic partners for organizations that prioritise scale, customization, or price-sensitive sourcing.

- Genome services & CRO-aligned suppliers (GenScript, Daicel Arbor, Synbio, General Biosystems, Creative Biogene, Dynegene): These providers combine oligo pools with gene synthesis, NGS preparation, and functional genomics services. They are attractive acquisition targets for companies seeking to augment end-to-end capabilities or to enter new application verticals quickly.

Recent market signals to watch in 2026

- Notable supplier pricing adjustments and contracting changes have emerged as companies pass through raw material inflation and operational cost increases—contract renegotiation and dynamic price indexing will be common.

- Technology licensing and partnerships continue to reconfigure competitive advantage; deals transferring specialized chemistries or proprietary phosphoramidite variants can reprice capability differentials.

- Regulatory initiatives in major jurisdictions are crystallising expectations for manufacturing control and analytical rigour—compliance will be a source of competitive differentiation rather than mere cost.

The report — what PW Consulting delivers (practical, operational, actionable)

This report is built as a decision-support toolkit for 2026. It deliberately balances strategic foresight with hands-on tools that commercial, operations, and corporate development teams can use immediately:

- Proprietary market model with historical 2020–2025 data and scenario-based forecasts through 2032 (with sensitivity to pricing and adoption curves).

- Supply-side cost models and COGS sensitivity matrices that map raw-material shocks to margin outcomes under alternative sourcing strategies.

- A supplier risk & readiness matrix assessing technical capability, scale, geographic footprint, and regulatory posture for leading providers.

- Commercial playbooks for pricing, segmentation, and channel strategies tailored to suppliers, CROs, and pharmaceutical buyers.

- M&A and partnership decision frameworks, including integration risk checklists and surplus-capacity monetization approaches.

- Regulatory impact maps that align emerging guidance to product development milestones and dossier readiness steps.

- Concise executive dashboards for board-level decision making and investor briefings.

Strategic recommendations for 2026 (executive checklist)

- For manufacturers: Prioritize dual-sourcing of key phosphoramidites, invest incrementally in automated QC, and establish contractual price adjustment clauses to manage margin volatility.

- For platform and instrument providers: Build tighter integrations with oligo suppliers and offer bundled workflows that reduce buyer switching costs.

- For biopharma and genomics end-users: Negotiate multi-year supply agreements with performance SLAs, require supplier regulatory evidence packages, and pilot alternative chemistries where IP risk is manageable.

- For investors and M&A teams: Prioritize assets with differentiated manufacturing IP, robust quality systems, and demonstrable customer stickiness; avoid deals where raw-material exposure is unmanaged.

On confidentiality and why you should read the full report

We intentionally present the strategic narrative, core dynamics, and actionable frameworks here while withholding the detailed segment-level tables, regional breakdowns, and price-by-pool matrices that underpin our models. Those granular data and interactive models are included in the full PW Consulting report and are essential for transaction underwriting, budget reallocations, and sourcing decisions in 2026.

Next steps

Leaders preparing 2026 budgets, contracts, or investment memos should request the full dataset and scenario models to quantify downside exposure and upside capture strategies. The PW Consulting team is available for custom briefings, model walkthroughs, and tailored advisory engagements to convert the report’s insights into executable plans.

To access the full report, interactive models, and supplier scorecards, visit the PW Consulting Oligonucleotide Pool Library Market page or contact our advisory desk for a confidential briefing.

For detailed analysis of this topic, please visit the official page: Oligonucleotide Pool Library Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.