PW Consulting: Histidine Market Poised for 6.8% CAGR, Reaching USD 338.85 Million by 2032

Histidine Market 2026 Strategic Brief — Actionable Intelligence for Corporate Decision-Makers

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a concise strategic briefing drawn from our new Histidine Market research (base year: 2025). This is a forward-looking “trailer” designed to surface the levers that will matter to executive teams in 2026 while reserving the granular segmentation tables and proprietary models for the full report.

Histidine Market

Quick market context

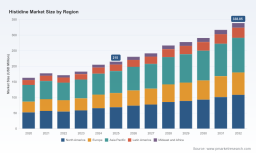

Histidine is transitioning from a specialty amino acid commodity toward a differentiated, high-value ingredient driven by biopharma demand, formulation purity requirements, and renewed interest in precision nutrition for feed and food. Our consolidated market model (USD, Million) shows the industry moving from an estimated 215.0 in 2025 to a projected 338.85 by 2032, reflecting a compound annual growth rate (CAGR) of 6.8% across the 2026–2032 forecast window. The trajectory masks near-term volatility during 2020–2022 and a clear recovery pathway thereafter; 2026 is modeled as the first full-year inflection after firms normalized post‑pandemic supply adjustments.

Histidine Market

Why this matters for 2026 corporate strategy

- Timing for investment: The mid‑decade acceleration embedded in our 6.8% CAGR suggests 2026 is a pivotal year for committing to capital and capacity options that will come online through 2028–2030.

- Supply‑chain architecture: Buyers and risk managers should treat 2026 as a planning horizon for diversified sourcing, given the market’s structural fragmentation and episodic policy shocks.

- Product and pricing stratification: Increasing segmentation between high‑purity, GMP‑grade histidine for biopharma and lower‑spec material for feed/food creates margin expansion opportunities for differentiated suppliers and pricing pressure for commoditized volumes.

- M&A and partnership windows: Strategic alliances and bolt‑on acquisitions executed in 2026 can capture disproportionate value as demand solidifies towards 2030.

What PW Consulting’s Histidine Market Report gives you (practical content)

The full report is a hands‑on toolkit for commercial, procurement, R&D, and corporate development teams. Highlights include:

Histidine Market

- A validated market sizing model (historical 2020–2025; forecast 2026–2032) with scenario sensitivities tied to price, feedstock input costs, and end‑market demand elasticity.

- Supplier scorecards and factory‑level capability maps that distinguish fermentation versus hydrolysis production bases, quality tiers (GMP, low‑endotoxin, low‑metal), and logistics‑to‑customer footprints.

- A regulatory and trade tracker that maps export controls, tariff trajectories, and compliance risk across major manufacturing hubs.

- Commercial playbooks: procurement negotiation scripts, dual‑sourcing templates, and short‑term contingency checklists (30/60/90 day actions) for supply disruption scenarios.

- Technology and process briefs on next‑generation fermentation strains, downstream purification techniques, and cost‑efficiency levers.

- M&A readiness packs: target screening filters, integration checklists, synergies calculator, and a prioritized five‑step due‑diligence agenda for histidine‑adjacent acquisitions.

- Executive dashboards: KPIs to monitor in 2026—inventory turnover, supplier fill rate, average realized ASP per quality tier, regulatory event exposure, and blended cost of goods sold (COGS) per kilogram.

Competitive landscape — how to read the supplier map in 2026

The histidine supply base is composed of specialized fermentation incumbents, chemical hydrolysis suppliers, and niche players focused on ultra‑high purity grades for life sciences. Key companies we profile in the report include Ajinomoto Co., Inc.; Kyowa Hakko Bio; Evonik Industries; Merck KGaA; Pfanstiehl Inc.; Daesang Corporation; and Changzhou Highassay Chemical. Each occupies distinct strategic positions:

- Ajinomoto: deep fermentation expertise and an expanding global supply posture—recent strategic moves emphasize collaborative partnerships to secure feedstock-to-product continuity.

- Kyowa Hakko Bio: reputation in bulk pharmaceutical‑grade material and consistent investments in process control to meet biotech client specifications.

- Evonik and Merck KGaA: play the high‑purity, GMP‑certified end of the market, capturing premium pricing where trace metals, endotoxin levels, and documented supply chains matter most.

- Pfanstiehl: focused on low‑endotoxin and low‑metal formulations tailored to formulation scientists in the US biopharma market.

- Daesang and Changzhou Highassay: regional volume players with agility in feed and food segments and the potential to scale specialty grades through technology transfer.

Market concentration metrics underline a fragmented market: the combined share of the largest three and five firms remains modest relative to many other specialty‑chemical sectors. This fragmentation creates both risk (coordination under stress) and opportunity (consolidation targets and differentiation plays). Our report provides a company‑by‑company commercial risk matrix, executive scorecards, and playbooks for partnering or competing with each archetype.

Notable recent developments and implications

- Strategic partnerships: The March 2025 announcement of a co‑development and supply arrangement involving Ajinomoto illustrates the practical industry response to capacity and reliability concerns—these types of partnerships can materially alter regional supply balances and should be included in 2026 sourcing deliberations.

- Regulatory shifts: A policy development in early 2026—temporary suspension of certain export controls on dual‑use items—has immediate implications for trade in chemical intermediates relevant to amino acid production. Buyers and manufacturers should model both the upside (easier access to intermediates) and the downside (policy reversals, sudden on‑shoring incentives) in their 2026 procurement strategy.

Strategic plays for 2026 — recommended priorities by function

- Procurement: Move from single‑year spot procurement to layered contracting—mix of short‑term flexible contracts, medium‑term fixed volumes, and long‑term strategic partnerships with supply guarantees tied to service level agreements and price pass‑through clauses.

- Operations and CapEx: Fast‑track feasibility studies for modular, scalable fermentation capacity if your organization targets high‑purity segments; defer large fixed CapEx for commodity grades where price competition and overcapacity risk remain.

- R&D and product: Prioritize formulation work that reduces ingredient sensitivity to histidine grade where feasible; alternative molecule strategies can be a hedge for biopharma formulators facing supply constraints.

- Corporate Development: Use 2026 to execute selective bolt‑ons—especially in purification tech and contract manufacturing—that yield rapid margin accretion and customer intimacy rather than broad geographic expansion without specialization.

- Risk & Compliance: Implement a live regulatory event dashboard and incorporate geopolitical trigger clauses into contracts; ensure visibility to changes in export control status of key intermediates.

Scenario thinking — three policy and demand pathways

Our model embeds three scenarios for 2026–2032: (1) baseline growth consistent with the published 6.8% CAGR, (2) constrained‑supply upside where regulatory easing and investment accelerate adoption of high‑purity grades (faster premiumization), and (3) soft‑demand downside tied to macroeconomic contraction or feedstock price shocks. For executive teams deciding in 2026, the key question is not which scenario will occur, but how to design options that preserve upside capture while limiting downside exposure. The full report includes probability‑weighted P&L and cash‑flow outcomes for each scenario.

Key risks to monitor in 2026

- Policy reversals affecting trade and intermediate access; even temporary suspensions or relaxations can produce near‑term inventory imbalances.

- Concentration risk in specialty grades: although the broader market is fragmented, the ultra‑high‑purity niche is tighter—loss of a single qualified supplier can trigger tiered price uplifts for formulators.

- Feedstock and energy cost inflation that compresses margins disproportionately for fermentation producers versus chemically synthesized volumes.

- Regulatory and quality compliance lapses—biopharma customers require documented provenance and GMP continuity, which raises switching costs and supplier certification time horizons.

How to use this briefing in your 2026 planning cycle

- Embed the report’s executive dashboard into your Q1 risk review and procurement cycle.

- Run a three‑week rapid due‑diligence on your top two suppliers using our supplier scorecard to test claims on capacity, quality, and contingency plans.

- Prioritize small, executable capex and partnership pilots for high‑purity fermentation capacity rather than large capital commitments to commodity routes.

- Use the scenario P&L outputs to stress‑test covenant compliance under different price and supply shocks.

Closing — why PW Consulting’s report matters for 2026

As companies refine strategies for the coming five years, 2026 represents an inflection point where demand recovery, premiumization for high‑quality histidine, and policy volatility intersect. Our report equips leaders with the models, checklists, and playbooks needed to convert market insights into defensible actions—whether that is securing supply, targeting high‑margin product segments, executing M&A, or hedging regulatory risk.

For access to the full data tables, granular regional and application splits, supplier scorecards, and customizable scenario models, please visit the report landing page or contact PW Consulting for a tailored executive briefing. The public brief above intentionally omits the detailed segmental numbers to preserve the strategic value of the complete dataset and to ensure your team receives the operationally actionable intelligence critical for 2026 decision-making.

For detailed analysis of this topic, please visit the official page: Histidine Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.