PW Consulting: Interior Design Market to Expand at 6.5% CAGR, Reaching USD 331 Billion by 2032

PW Consulting: Strategic Brief — Interior Design Market Outlook 2026 (Executive Preview)

Executive summary

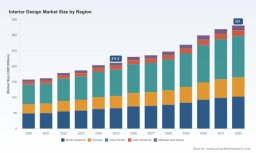

PW Consulting’s latest Interior Design Market report (base year 2025) delivers a practical, executive-grade view of a sector transitioning from recovery into sustained expansion. The global market expanded from roughly USD 158 billion in 2020 to USD 211.5 billion in 2025. Under our base-case modelling, the market is forecast to continue growing through 2032, reaching an aggregate size above USD 330 billion — a trajectory underpinned by a 6.5% compound annual growth rate across the 2026–2032 forecast window.

Interior Design Market

Those headline figures mask sharp structural shifts that will influence strategic decisions throughout 2026: accelerating premiumization in developed markets, resilience-driven sourcing reconfiguration, increasing regulatory attention on professional practice, and the emergence of circular-materials demand vectors. This release is a preview: it demonstrates the analytical depth and actionable orientation of the full report while reserving the granular segment tables and proprietary scoring that corporate teams need for implementation.

Interior Design Market

What the report delivers — practical sections for immediate action

- Market sizing and validated historical time series (2020–2025) and scenario-based forecasts (2026–2032), with transparent method notes and sensitivity checks.

- Demand-driver deep dives — consumer preferences, construction and renovation cycles, commercial fit-out dynamics, institutional procurement patterns, and product-technology inflection points.

- Competitive landscape portraits and strategic scorecards for leading manufacturers, retailers, and integrated design firms, including capability maps and go-to-market implications.

- Supply-chain risk heatmaps addressing tariffs, raw-material volatility, labour constraints, and nearshoring opportunities.

- Operational playbooks: pricing resilience, procurement levers, modularization strategies, and digital customer journeys for design services.

- M&A and partnership screening templates: target profiles, valuation heuristics, and integration risk checklists tuned to 2026 market realities.

- Regulatory and licensing tracker with state- and national-level developments, plus recommended responses for professional bodies and firms.

- Sustainability transition pathways: modal shift options, circular-design pilots, and supplier engagement scripts to meet both regulation and premium-consumer expectations.

Why this matters for decisions in 2026

- Investment prioritization : With mid-term growth projected at a steady mid-single-digit CAGR, capital allocation must favor capabilities that compound value — design IP, vertically integrated manufacturing where it drives margin, and digital platforms that reduce time-to-spec.

- Pricing & margin defense : Rising material costs and tariff pressures continue to compress gross margins. The report provides a staged price-pass framework and product-bundle tactics to preserve realized margins without eroding demand.

- Supply-chain resilience : We map supply nodes by risk level and recommend a three-tier sourcing posture (strategic partners, flexible nearshore suppliers, contingency stock). Executives can use the playbook to reduce single-point dependencies and lower lead-time variability.

- Talent and licensing : New licensing activity and workforce tightness mean firms must adopt hybrid staffing models — combining credentialed interior professionals with digitally enabled contractors — to scale design capacity cost-effectively.

- Sustainability as value capture : Sustainability is no longer just compliance. Early movers on circular materials and transparent supply chains can command pricing premiums and unlock institutional procurement mandates.

Competitive landscape — strategic implications for incumbents and challengers

The market remains fragmented, with a set of well-capitalized incumbents and a larger cohort of specialist players. The full report includes detailed scorecards; below we synthesize strategic postures of exemplar firms and the choices they signal to competitors.

Interior Design Market

- Sanderson Design Group PLC (UK): A heritage-led producer with a portfolio approach to brands and categories. Its strength is brand equity and licensing flexibility across wallpapers, fabrics, and allied interior products. Strategic priorities for rivals include leveraging heritage IP through collaborations and accelerating digital pattern libraries for faster customization.

- RH (United States): A luxury lifestyle retailer integrating high-touch design services with a premium product assortment. RH’s model highlights value in experiential retail and curated design ecosystems. Competitors should evaluate whether replicating a gallery-like retail experience or partnering with curated designers yields higher return on invested capital in luxury segments.

- Ethan Allen Interiors Inc. (United States): Vertically integrated manufacturing and retailing with an emphasis on custom-crafted furniture and in-house design services. This integration enables control over lead times and quality — a key advantage when material inflation and tariffs are common. For brands considering vertical moves, our report lays out a phased build-versus-buy cost model.

- Mohawk Industries, Inc. (United States): A large-scale materials and components producer serving both residential and commercial channels. Mohawk’s position underscores the strategic importance of upstream scale and product diversification (flooring, panels, tile). For interior brands, the lesson is to secure material supply lines and to co-develop low-emission product ranges that align with procurement mandates.

Across these profiles the common strategic levers are clear: (1) control of product differentiation (brand or manufacturing), (2) channel optimization (direct-to-consumer combined with trade partnerships), and (3) supply-chain control. The full report provides comparative matrices that score each firm across these axes and identify potential M&A pairings that would unlock complementary strengths.

Near-term catalysts and policy context

Industry momentum in the opening months of 2026 — exemplified by major trade events and awards programmes — will shape trend adoption and buyer sentiment. Calendar highlights such as interior trade shows and awards cycles accelerate concept-to-market timelines and create sourcing windows for new materials and finishes.

Concurrently, regulatory and cost pressures are material. Industry bodies have flagged rising material costs, tariffs, and labour shortages as near-term disruptors; building-material tariff actions already show measurable impacts on upstream costs. Separately, a wave of state-level attention to interior design licensing is reshaping professional credential expectations in several jurisdictions. These forces combined will make disciplined scenario planning and contingency provisioning non-negotiable for 2026 plans.

How to use this report in your 90/180/360-day plan

- 90 days — Rapid diagnostic: use the report’s supply-chain heatmaps and competitor scorecards to identify two immediate procurement diversifications and one pricing adjustment to protect margins.

- 180 days — Operationalize: deploy a pilot for modular product lines or digital design services, and shortlist two potential acquisition or partnership targets using our M&A filters.

- 360 days — Scale and embed: implement capability build plans for manufacturing or digital channels, and initiate cross-functional programs (sourcing, design, sustainability) tied to measurable KPIs.

What you won’t find in this preview

This executive preview signals the depth of our analysis while intentionally omitting the granular segment-level tables, regional splits by application, and proprietary scoring algorithms that underpin client-grade strategy work. Those detailed datasets and the accompanying interactive dashboards are available exclusively in the full report and client portal — they are the instruments firms use to convert insight into executable targets and budgets for 2026.

Next steps

Leaders preparing budgets and M&A pipelines for 2026 should treat this report as both a map and a drillbook. If you are prioritizing margin defense, supplier resilience, or a step-change in your direct-to-consumer capabilities, the full report provides the scenario outputs, unit-economics templates, and vendor shortlists necessary to move from boardroom intention to operational execution.

Contact PW Consulting to access the complete report, the interactive dashboards, and bespoke briefings tailored to your strategic priorities. Our analysts are scheduling limited advisory slots for clients who require hands-on assistance implementing the 2026 playbooks identified in this research.

For detailed analysis of this topic, please visit the official page: Interior Design Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.