PW Consulting: Marine Propeller Market Hits USD 4.48 Billion in 2025, Poised for Strong Growth

Marine Propeller Market: Strategic Imperatives for 2026 — PW Consulting Market Brief

Executive summary

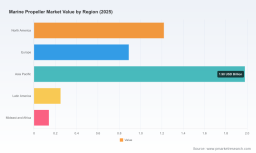

As a foundational element of ship performance and lifecycle emissions, the marine propeller market is transitioning from cost-driven replacement cycles toward technology-led value creation. Our PW Consulting Marine Propeller Market study (base year 2025) shows the global market expanding from roughly USD 3.56 Billion in 2020 to USD 4.48 Billion in 2025, and we forecast continued growth at a compound annual growth rate (CAGR) of 6.6% through our planning horizon (2026–2032), reaching an estimated USD 6.94 Billion by 2032. This briefing distills the report’s most decision-relevant implications for executive teams planning investments, procurement, or M&A in 2026, while intentionally reserving core segmented datapoints to encourage direct engagement with the full study.

Marine Propeller Market

Why this report matters for 2026 decisions

-

Strategic procurement: With lead-times, material prices, and regulatory constraints tightening, procurement teams that adopt demand-forecast linked contracting will reduce cost volatility and shipment delays.

Marine Propeller Market -

Product development: Propeller performance is increasingly a systems issue—blade design, hub technology, surface treatments, and integration with variable-speed drivetrains now determine commercial returns on fuel-efficiency investments.

Marine Propeller Market -

M&A and partnerships: Fragmentation persists alongside pockets of consolidation; 2026 is a window for bolt-on acquisitions that deliver manufacturing scale, proprietary tooling, or access to retrofit channels.

-

Aftermarket and services: Repair, scanning, and retrofitting services are a higher-margin growth path as owners seek to extend vessel life and meet life-cycle GHG intensity expectations.

Market dynamics shaping 2026 strategy

-

Regulatory acceleration: The adoption of new standards (e.g., ISO 18581:2026 for fixed-pitch hub cap design) and IMO lifecycle GHG guidance is shifting buyer requirements from purely mechanical specifications to lifecycle and compatibility requirements. Companies that embed compliance into design and validation workflows will shorten sales cycles.

-

Decarbonization as a purchasing vector: Shipowners are increasingly evaluating propulsion components through a Tank-to-Wake lens. Propeller selection and retrofits that demonstrably reduce fuel intensity will command preference and premium service contracts.

-

Raw material and shipbuilding cost volatility: Recent upward pressure on ship prices and material indices has a twofold effect—deferring some new-build propeller orders while accelerating aftermarket repairs and upgrades. Risk-managed sourcing strategies and strategic inventory positioning can mitigate margin erosion.

-

Geopolitical and trade friction: Proposed tariff actions on maritime products have raised procurement risk in 2025–2026. Suppliers and buyers should stress-test supply chains, evaluate near-shoring opportunities, and incorporate tariff scenarios into bid models.

-

Manufacturing innovation compresses lead times: Recent production-scale innovations demonstrate a step-change in responsiveness. For example, collaborative manufacturing approaches have reduced typical cast-and-produce cycles from months to weeks, unlocking aftermarket responsiveness and enabling just-in-time retrofit programs.

Competitive landscape — what to watch in 2026

The market sits between concentrated OEMs and a broad base of specialized manufacturers and service providers. Measured concentration indicates meaningful incumbent strength without insurmountable barriers for innovative entrants (CR3 ~55%; CR5 ~62%). The competitive field is evolving along three axes: materials and casting capability, precision machining/CNC specialization, and aftermarket scanning/repair services.

-

Michigan Wheel (Grand Rapids, MI; https://www.miwheel.com/) — Historically strong in recreational and commercial inboard/outboard propellers. Their strategic repositioning—illustrated by a recent sale of UK operations—signals focus on core markets and potential reallocation of capital to R&D and aftermarket channels.

-

VEEM Marine (Perth, Western Australia; https://veemmarine.com/) — Known for CNC-machined, performance-grade propellers including specialized high-speed designs. VEEM’s engineering-centric play is an archetype for premium, performance-sensitive OEMs.

-

Sharrow Marine (Detroit, MI; https://www.sharrowmarine.com/) — A technology-led small-fleet manufacturer with patented blade architectures. Their recent production-scaling collaboration with an automotive OEM demonstrates how cross-sector manufacturing partnerships can dramatically compress turnaround times and scale advanced casting techniques.

-

Nakashima Propeller Co., Ltd. (Okayama, Japan; https://www.nakashima.co.jp/eng) — A global supplier with depth across ocean-going and specialist vessels; their strategic M&A activity in 2025 highlights a consolidation play in select geographies.

-

AccuTech Marine Propeller (Dover, NH; https://accutechmarine.com/) — Exemplifies the high-margin aftermarket: advanced prop-scan diagnostics and precision repair/tuning tailored to vessel operators looking to avoid full replacement.

-

PowerTech! Propellers , Quality Castings Wisconsin , and Anchor Miami Propeller — These suppliers represent the diverse middle-market: standard stainless/aluminum producers, precision casters, and performance-focused regional providers that together supply the aftermarket and niche OEM segments.

Recent developments that change the playbook

-

Strategic industry moves: A notable 2025 strategic sale saw a North American supplier divest European operations to a global propeller manufacturer—an example of targeted geographic consolidation that reallocates resources toward R&D and high-margin segments.

-

Production scaling breakthroughs: A 2026 announcement from a leading propeller innovator revealed a collaboration with an automotive manufacturer that reduced sand-casting production timelines from roughly 130 days to about two weeks—reshaping aftermarket turnaround economics.

-

Market convenings and product evolution: The 2025 Annual Marine Propulsion Expo and new product launches throughout 2024–2026 have accelerated the diffusion of multi-blade, low-noise designs and integrated hub technologies.

What the full report provides (practical, executable content)

-

Robust demand model and scenario forecasts (2026–2032) calibrated to new-build vs. retrofit drivers, fuel-cost elasticity, and regulatory adoption pathways.

-

Supplier and capability maps that identify manufacturing capacity, precision machining clusters, and aftermarket service footprints—designed for sourcing and site-selection decisions.

-

Competitive heatmaps and capability overlays for the leading OEMs, highlighting technology specialisms and market moves without disclosing client-level confidentials.

-

M&A playbook and valuation sensitivities tailored to propeller businesses, including synergy templates for bolt-on acquisitions and carve-outs.

-

Procurement checklists and sample contract clauses that address tariff risk, IP protection for blade geometries, supply continuity, and compliance with ISO/IMO developments.

-

Aftermarket monetization templates—price/volume sensitivity, lifecycle breakeven for retrofit campaigns, and maintenance-as-a-service commercial models.

-

Technical appendix: testing protocols, performance metrics (efficiency, cavitation, NVH), and recommended validation templates for new propeller concepts.

Actionable recommendations for 2026

-

For OEMs and manufacturers: Prioritize capital allocation to near-term manufacturing capacity and digital quality controls (3D scanning, CNC automation) that shorten delivery cycles and support higher mix, lower-volume production economics.

-

For shipowners and operators: Commission prop-scan diagnostics as standard during scheduled dry-dock windows and evaluate retrofits when the projected fuel savings under plausible 5–7 year fuel price paths exceed replacement costs.

-

For investors: Target acquisitions that unlock aftermarket service networks or proprietary manufacturing methods; use the included valuation sensitivity models to stress-test assumptions around material costs and regulatory adoption rates.

-

For procurement leaders: Build contractual flexibility for tariff and supply shocks—layered sourcing, near-shoring pilots, and buffered consignment stock where total-cost-of-ownership analysis supports it.

-

For R&D leaders: Integrate lifecycle GHG metrics early in product development to align with IMO guidance and to create defensible differentiation in lifecycle-based procurement tenders.

Methodology & scope

The study uses a mixed-methods approach: bottom-up ship-class demand modeling, aftermarket replacement cycles, supplier capacity analysis, and scenario-based macroeconomic overlays. Base year is 2025 with historical observation from 2020–2025 and a forecast window of 2026–2032. All monetary values are stated in USD (Billion) and the central forecast assumes a 6.6% CAGR for the forecast period. Detailed segmentation matrices (by region, type, and application) and granular unit economics are available in the full report—released as part of PW Consulting’s 2026 maritime portfolio.

Next steps — access and engagement

This brief outlines the operationally relevant signals we believe will determine winners and losers in the marine propeller market over the next three years. For procurement-ready datasets, proprietary segmentation tables, and our interactive decision-support models (including the retrofit breakeven tool and supplier risk heatmap), please consult the full PW Consulting Marine Propeller Market report or schedule a tailored executive briefing. The full study contains the granular numeric splits, regional and application tables, and vendor-level benchmarking intentionally withheld here to preserve the strategic value of the complete deliverable.

For detailed analysis of this topic, please visit the official page: Marine Propeller Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.