PW Consulting Forecast: Gas Engines Market to Grow from USD 5.84 Million in 2025 to USD 8.55 Million by 2032 at a 5.6% CAGR

Gas Engines Market 2026 Strategic Briefing — PW Consulting Industry Insight

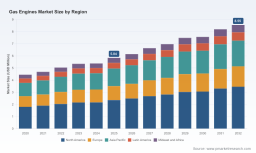

As organizations finalize capital allocation and product roadmaps for 2026, the gas engines market presents a nuanced growth opportunity shaped by decarbonization imperatives, evolving fuel quality standards, and an accelerating shift toward service-centric business models. PW Consulting’s latest Gas Engines Market study (base year 2025; forecast period 2026–2032) synthesizes five years of historical trends and a forward-looking scenario suite to equip executives with the actionable intelligence needed to navigate this transition. The market has expanded from approximately USD 4.45 Million in 2020 to USD 5.84 Million in 2025 and is projected to reach roughly USD 8.55 Million by 2032, implying a compound annual growth rate of 5.6% across the forecast window.

Gas Engines Market

Why this report matters for 2026 decision-makers

-

Capital allocation: With constrained budgets and competing priorities (grid resilience, renewables integration, emissions control), procurement and investment teams need clear, defensible scenarios to prioritize engine types, retrofit strategies, and lifecycle service commitments.

Gas Engines Market -

Product strategy: OEM and Tier‑1 leaders must reconcile short‑term demand for high‑efficiency natural-gas assets with mid‑term needs for hydrogen-ready or low‑carbon alternatives. Our analysis identifies which technical levers create differentiated value and which are commoditizing.

Gas Engines Market -

Regulatory compliance: New reporting and standards regimes are increasing compliance costs and influencing specifications. Operators and OEMs must anticipate these shifts to avoid warranty and operational risk.

-

M&A and partnerships: The market structure points to selective consolidation and buy-and-build opportunities for service-oriented players seeking scale in aftermarket parts and digital services.

Market trajectory: measured growth, persistent opportunity

Across the historical period (2020–2025) the sector has demonstrated steady expansion, rising from about USD 4.45 Million to USD 5.84 Million. The forecasted trajectory to roughly USD 8.55 Million by 2032 (CAGR 5.6% for 2026–2032) reflects a market that is neither hyper‑cyclical nor saturated — instead offering predictable, investment-grade growth. Importantly, concentration metrics indicate a fragmented supplier base: the top-three vendor share remains modest, and even the top-five combined share suggests significant room for differentiated specialization and local service plays. For corporates, that fragmentation translates into both execution risk and procurement leverage, depending on how a buyer approaches supplier rationalization and long‑term service contracting.

Strategic themes shaping outcomes through 2026 and beyond

-

Hydrogen readiness and fuel flexibility: OEM roadmaps increasingly cite hydrogen-capable platforms or dual‑fuel capability as core product differentiators. Buyers need a clear view of the trade-offs between upfront premium and future-proofing benefits.

-

Decarbonization via lifecycle approaches: Emissions reduction is shifting from discrete engine performance metrics to lifecycle emissions strategies that include fuel sourcing, electrification of auxiliaries, and integration with renewables and storage.

-

Service-led revenue models: Given the aftermarket margin profile and the importance of uptime for critical applications (data centers, grid stabilization), suppliers are investing in condition‑based maintenance, digital twins, and outcome‑based contracts.

-

Standards and fuel quality: International guidelines and regional reporting obligations are raising the bar for guaranteed performance, especially in marine and oil & gas segments.

-

Distributed energy and grid dynamics: Gas engines retain strategic relevance for peaking, CHP/COGEN, and remote power applications where flexibility and fast dispatchability are critical.

Competitive landscape — how incumbent strategies are evolving

The competitive set is diverse, spanning specialists with deep installed bases to multi‑platform industrial OEMs. Our assessment of leading participants highlights the strategic differentiation each brings to the market:

-

INNIO Jenbacher (Jenbacher, Austria) : With a large installed base measured in the tens of gigawatts, Jenbacher’s portfolio emphasizes dedicated gas engines and clear progress toward hydrogen-capable platforms. Their strength lies in application engineering for cogeneration and power generation, making them a reference point for long‑term reliability and fuel‑transition programs.

-

Caterpillar Inc. (Peoria, Illinois, USA) : Caterpillar leverages an extensive dealer and service network alongside natural gas and compression engine offerings. Their strategy centers on integrated power systems and lifecycle support, which is attractive to large industrial buyers seeking single‑vendor accountability.

-

Cummins Inc. (Columbus, Indiana, USA) : Cummins’ newer natural gas platforms and near‑zero emissions engines position them as a flexible player across heavy‑duty and stationary markets. Their emphasis on emissions compliance and modular electrification pathways is likely to accelerate adoption in regulated markets.

-

MAN Energy Solutions (Augsburg, Germany) : With an offering that spans small to mid-range power outputs, MAN focuses on low‑pollution engines and cogeneration. Their engineering depth supports industrial customers with bespoke configurations.

-

Rolls‑Royce Power Systems (mtu) (Friedrichshafen, Germany) : Mtu’s positioning targets high‑reliability applications such as data centers and grid stabilization. Their generator-set integration capabilities and fast‑response portfolios are differentiators where reliability is paramount.

-

Wärtsilä (Helsinki, Finland) : Wärtsilä’s range of 4‑stroke spark‑ignited engines is oriented to power plants and cogeneration, with strength in system integration for larger power projects and hybridization with energy storage.

-

Perkins Engines (Peterborough, UK) : Perkins competes on robustness for harsh environments, making them a preferred choice for remote or heavy industrial applications requiring rugged, serviceable platforms.

-

DEUTZ AG (Cologne, Germany) : DEUTZ targets water‑cooled gas and gasoline engines for industrial and off‑highway uses, addressing customers seeking compact, durable solutions for non‑road applications.

Together, these vendors demonstrate the plurality of routes to value: deep installed bases and application engineering, broad service networks, emissions leadership, and niche reliability plays. For potential acquirers or alliance partners, the market’s modest top‑tier concentration suggests inorganic consolidation and exclusive service partnerships remain viable strategies to capture aftermarket margin and lock‑in customers.

Regulatory & standards developments that will reframe procurement in 2026

-

Reporting obligations: Regional reporting deadlines for engine emissions—for example, medium and large engine reports due May 1, 2026 for the 2025 calendar year in certain jurisdictions—are increasing the administrative and technical burden on operators. Buyers must factor compliance‑related upgrades, metering, and recordkeeping into TCO models.

-

Fuel quality standards: The CIMAC Guideline 05 (2025 edition) on the impact of gas quality on gas engine performance introduces new expectations for marine applications and has broader implications for engine tolerance to variable fuels. This increases the importance of fuel quality risk assessments and may accelerate demand for conditioning and monitoring solutions.

What’s in the PW Consulting report — practical deliverables

-

Executive summary with strategic implications tailored to OEMs, utilities, independent power producers, and oil & gas operators.

-

Market sizing and forecast model (2020–2032), including scenario sensitivity and downside stress cases (methodology transparent and audit‑ready).

-

Technology and product maturity matrix, highlighting hydrogen readiness, dual‑fuel capability, and retrofittability.

-

Supplier scorecards and go‑to‑market playbooks: commercial KPIs, margin pools, service strategies, and partnership archetypes.

-

Regulatory impact assessment and compliance cost engineering templates for 2026 planning cycles.

-

M&A screening grid and a prioritized list of target archetypes (by capability, service access, and aftermarket potential).

-

Operational readiness checklists and procurement templates to accelerate RFP and contract negotiation cycles.

Recommended next steps for buyers and suppliers in 2026

-

Prioritize modular upgrades: Target platforms that allow staged hydrogen integration to protect near‑term ROI while preserving retrofit optionality.

-

Secure aftermarket coverage: Negotiate outcome‑based service agreements with clear performance SLAs and shared‑risk maintenance models.

-

Upgrade compliance capabilities: Invest in standardized reporting and fuel‑quality assurance to preempt enforcement and warranty disputes.

-

Build digital operations: Deploy condition monitoring and digital twin pilots focused on high‑value assets to validate service economics before scaling.

-

Evaluate inorganic moves: Use the report’s screening framework to assess targets that immediately strengthen aftermarket scale or proprietary sensor/software capabilities.

Why review the full report

This briefing is intentionally concentrated on strategic takeaways. PW Consulting’s full Gas Engines Market report contains the granular segmentation, regional demand curves, and supplier financial benchmarks necessary to run procurement simulations, build investment memos, and support board‑level decisions. For teams that must translate strategy into procurement language and financial models in 2026, the full dataset and scenario models are essential.

To access the complete report, including detailed segment-level intelligence, supplier dashboards, and the downloadable forecasting model, visit PW Consulting’s Gas Engines Market report page. Our team is also available to run bespoke workshops that translate the report’s findings into a 90‑day implementation plan aligned with your portfolio and risk appetite.

For detailed analysis of this topic, please visit the official page: Gas Engines Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.