PW Consulting: Laser Drilling Machine for Aerospace Market Forecast to Expand at 6.98% CAGR Through 2032

PW Consulting: Strategic Brief — Laser Drilling Machine for Aerospace Market (2026 Decision Playbook)

Executive snapshot

PW Consulting today publishes a targeted strategic briefing derived from our full market research report on the Laser Drilling Machine for Aerospace market. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, the study combines quantitative market-sizing with actionable decision frameworks to guide procurement, R&D, and investment choices in 2026 and beyond. At the macro level, the market is expected to expand at a compound annual growth rate of 6.98% from the 2025 base, reflecting accelerating demand for precision micro-drilling across turbine, engine and airframe supply chains.

Laser Drilling Machine for Aerospace Market

Why aerospace leaders should read this now

-

Certification and time-to-qualified-supplier have become determinative procurement gates. Delays in NADCAP or OEM approvals can add months to program timelines and materially alter supplier selection economics.

Laser Drilling Machine for Aerospace Market -

Technology choices made today — laser type, axis architecture, and integrated software — lock in performance, throughput and maintainability for a decade. Our report quantifies trade-offs for capital and operating models used by OEMs and tier suppliers.

Laser Drilling Machine for Aerospace Market -

Aftermarket and service economics are an increasingly important source of margin for machine vendors and a critical cost for operators. The report provides a pragmatic services playbook to align maintenance strategies with utilization targets.

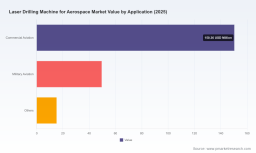

Data-driven view: market trajectory and what it means

From a measured base year in 2025, the overall market continues to scale as aerospace programs push higher-density cooling designs, lighter engine architectures and increased production rates. Our topline sizing and forecast show a clear expansion through 2032, driven by elevated OEM program activity, rising aftermarket throughput, and steady substitution of legacy processes with high-precision laser systems. For decision-makers, the takeaway is simple: procurement windows are opening for those who have clarified their production and qualification timelines.

Core growth drivers and operational levers

-

Thermal management design complexity — modern turbine cooling strategies require dense arrays of effusion holes that are only practical with high-throughput, high-precision laser drilling.

-

Shifts toward fiber-laser architectures and multi-axis kinematics — these technologies deliver repeatable micro-holes and lower maintenance footprints, enabling better unit economics at scale.

-

Stringent certification regimes and OEM approvals — NADCAP and OEM-specific standards drive supplier selection and create an advantage for vendors with existing aerospace accreditations.

-

Automation and software integration — closed-loop monitoring, advanced CAM suites, and inline inspection are moving from “value-add” to “table stakes” in production environments.

Process and performance benchmarks

Laser drilling in aerospace is highly engineered: contemporary multi-axis systems can achieve sub-0.05 mm micro-hole capability with sub-10 µm positioning accuracy and, in high-throughput configurations, hundreds of bores per second on suitable geometries. These process benchmarks underpin comparative evaluations between laser types and machine architectures: throughput per shift, quality yield, and secondary processing needs (deburring, inspection) are sensitive to those choices.

Competitive landscape — what the market looks like to buyers

-

Established machine-tool OEMs have product lines purpose-built for turbine and engine work, offering integrated hardware + software stacks that simplify qualification for larger programs.

-

Specialist providers emphasize NADCAP/OEM approvals, process expertise on exotic alloys and composites, and vertically integrated service footprints that appeal to MROs and tier suppliers.

Notable vendor archetypes profiled in the report include multi-axis industrial OEMs with bundled software capabilities, regional specialists with deep certification portfolios, and agile service-centric firms that complement their equipment offerings with calibrated process know-how. While several vendors are often referenced by aerospace buyers for their technology leadership, the market remains sufficiently fragmented that partnership choice has measurable program-level consequences.

Recent industry signals and their implications

-

Trade events and industry fora over the last 12–18 months highlighted 3D drilling capabilities and integrated modules for automated drilling workflows — a signal that systems integration and process automation are market differentiators.

-

New product introductions and show demonstrations emphasize throughput scaling and automated toolpaths, reflecting supplier responses to OEM cycle-time pressures.

-

Regulatory and certification requirements continue to shape adoption; NADCAP and OEM-specific approvals are non-negotiable in many program flows and remain a key gate for suppliers and service providers.

What’s inside the full PW Consulting report (practical deliverables)

-

Proprietary topline sizing and seven-year forecast model with scenario toggles for production cadence, certification lag and replacement cycles.

-

Decision frameworks that translate process benchmarks into procurement criteria: throughput-per-capital, quality yield sensitivity, and total cost of ownership templates customized for aerospace workflows.

-

Vendor scorecards and a phased supplier-selection playbook that weigh technology fit, certification status, service footprint, and integration risk.

-

Operational checklists for qualification roadmaps (NADCAP timelines, OEM approval pathways), including a sample Gantt for a one- to three-machine onboarding program.

-

Aftermarket and spare-parts strategies, with monte-carlo style stress tests on uptime assumptions and their impact on unit economics.

-

Case vignettes from production settings capturing how machine configuration choices affected yield, cycle time and downstream inspection load.

Strategic recommendations for 2026 decision cycles

-

Align procurement to program milestones, not calendar years. Start machine qualification and NADCAP-related activities early in the program lifecycle to avoid costly production ramp delays.

-

Prioritize integrated solutions where process repeatability is mission-critical. Machines with proven CAM/inspection stacks shorten time-to-qualify and reduce first-pass yield risk.

-

Model service economics explicitly. For many operators, service contracts and spare-part availability eclipse capital amortization as primary drivers of lifetime cost.

-

Use proof-of-process gates to de-risk supplier selection. Run parallel qualification trials with shortlisted vendors to capture real-world throughput and secondary-processing impacts.

-

Consider staged automation: modular upgrades (e.g., Smart Driller-type modules) can defer initial CapEx while preserving a clear path to higher automation levels as production scales.

How PW Consulting’s analysis helps buyers, vendors and investors

For buyers, the research provides procurement-ready artifacts — scorecards, inspection criteria, and TCO templates — that speed decision cycles and increase confidence in supplier commitments. For vendors, the competitive intelligence and product benchmarking reveal where to invest in certifications, software, and service footprints to win aerospace business. For investors, the forecast and scenario analyses surface where consolidation, specialization, or service-enabled differentiation are likely to compress risk and create value over the coming planning cycle.

A reminder about the "trailer" approach

This strategic brief surfaces core trends, benchmarks and vendor archetypes to establish the context needed for 2026 decision-making. To preserve the tactical edge for organizations that require executable detail — including unit-level segmentation, regional dynamics, vendor scorecards, and modeled CapEx/Opex templates — the report’s full datasets and appendices are available through PW Consulting’s report distribution channels. The full deliverable contains the granular intelligence operational teams use to execute procurement and qualification programs.

Next steps

-

Procurement teams: use the included qualification Gantt and decision matrices to set internal deadlines aligned with program milestones.

-

Engineering and operations: request the report’s process benchmark annex to calibrate acceptance criteria and institute inline inspection metrics.

-

Senior leadership and investors: consult the forecast scenarios to stress-test CapEx plans and aftermarket service strategies over a seven-year horizon.

PW Consulting invites program managers, OEM sourcing leads, suppliers and private capital interested in the Laser Drilling Machine for Aerospace market to review the full report for actionable datasets and operational playbooks tailored for 2026 deployment decisions. For access to the complete analysis, vendor profiles, and the decision-support toolkit, please visit the PW Consulting report page.

For detailed analysis of this topic, please visit the official page: Laser Drilling Machine for Aerospace Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.