PW Consulting: Dust Sensors Market to Reach USD 0.82 Billion by 2032, Expanding at a 5.4% CAGR from 2026 — North America Holds USD 0.26B of the USD 0.57B 2025 Market

Dust Sensors Market: Strategic Imperatives for 2026 — PW Consulting Insight Brief

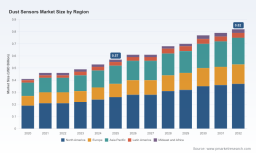

PW Consulting’s latest industry study on the Dust Sensors Market (base year: 2025; historical coverage: 2020–2025; forecast period: 2026–2032) synthesizes macro trajectory, regulatory inflection points, supply-chain realities, and vendor benchmarking into an operational playbook designed to inform executive decision-making in 2026. Our modelling shows market expansion at a steady compound annual growth rate (CAGR) of 5.4% (USD, revenue unit: Billion), with global market size rising from approximately 0.42 Billion in 2020 to 0.57 Billion in 2025 and continuing toward roughly 0.82 Billion by 2032. This brief explains why that trajectory matters to investors, product leaders, and procurement teams — and what the full report delivers to convert insight into action.

Dust Sensors Market

Why 2026 Is a Turning Point

-

Regulatory pressure is accelerating procurement cycles. Recent tightening of ambient air quality standards in major regulatory blocs has converted compliance from a long-term cost into an immediate procurement driver. Notably, the EU’s Ambient Air Quality Directive (Directive (EU) 2024/2881) reduces PM2.5 limit values and thereby raises monitoring demand (European Commission, 2026).

Dust Sensors Market -

Public-sector monitoring priorities are changing procurement profiles. The U.S. EPA’s 2025–2026 monitoring agenda explicitly endorses next-generation, low-cost sensor deployments in urban networks, creating new programmatic funding and scale opportunities (U.S. Environmental Protection Agency, 2026).

Dust Sensors Market -

Technology maturation is compressing time-to-market for integrated solutions. Laser and optical sensor families are benefiting from manufacturing process advances and component miniaturization, while software-driven calibration and edge analytics are reducing operational friction for large-scale networks.

Market Trajectory and Strategic Consequences

The Dust Sensors Market is neither nascent nor saturated. Our historical series shows steady growth between 2020 and 2025 (0.42 → 0.57 Billion USD), with foreseen continuation through the forecast window (2026–2032) consistent with a mid-single-digit CAGR. That pace reflects a balancing of headwinds (installation and calibration labor costs, component supply constraints) and tailwinds (regulation-driven procurement, urban air quality initiatives, and industrial emissions monitoring). For executives, the implication is clear: 2026 is a year to move from exploratory pilots to scaled rollouts — but to do so with an operational playbook that controls lifecycle costs.

What the PW Consulting Report Delivers (Practical, Executable)

-

Market sizing and scenario modelling: robust baseline sizing (2020–2025) plus three demand scenarios for 2026–2032 calibrated to regulatory, capital-availability, and technology-adoption sensitivities.

-

Supplier benchmarking and procurement playbooks: side‑by‑side evaluation of hardware accuracy, calibration needs, TCO models, and warranty/service economics to support RFP design and supplier negotiations.

-

Deployment and operations guide: standardized checklists for network design, installation labour planning, calibration cadence, remote diagnostics, and lifecycle upgrade pathways.

-

Regulatory impact assessment: jurisdictional heat-maps aligning monitoring obligations with plausible procurement windows, and stress-tested compliance cost estimates for 2026 program planning.

-

Technology deep dives: comparative analysis of sensing modalities (optical, laser, infrared, and electrochemical adjuncts), production constraints for optical components, and recommended integration patterns for edge analytics and cloud calibration.

-

Investment thesis and M&A roadmaps: valuation frameworks for early-stage sensor OEMs and consolidation scenarios useful for corporate development teams.

-

Case studies and reference implementations: anonymized examples of industrial emissions monitoring, urban air quality sensor networks, and embedded automotive/aerospace integration that demonstrate measurable ROI and operational pitfalls.

Competitive Landscape — Who Matters and Why

The market landscape combines global instrument manufacturers, specialized optical OEMs, and emerging low-cost sensor firms. While no single player dominates the market, the top vendors collectively represent under two-fifths of the market, leaving significant opportunity for differentiators in software, service, and systems integration.

-

ENVEA (France) — Known for industrial-grade monitors, their ProSens and Dusty lines are positioned for real-time emissions monitoring and filter leak detection. Recent product development continued in 2025 with a next-generation Optical Aerosol Spectrometer aimed at higher-fidelity PM monitoring in industrial settings (ENVEA, April 2025).

-

Chengdu Pulse Optics-tech Co., Ltd. (China) — Focused on laser and infrared dust sensing modules; manufacturing and optical-component expertise supports rapid OEM integration for air quality applications.

-

Cubic Sensor and Instrument Co., Ltd (China) — Specializes in industrial dust detection for powders and bulk solids, with productization aimed at process monitoring and leak detection in material-handling environments.

-

Zhengzhou Winsen Electronics Technology Co., Ltd (China) — Offers laser and IR sensor modules tailored to air-quality monitoring, with broad availability for device manufacturers and integrators.

-

Amphenol Advanced Sensors (United States) — Through its Telaire brand, it positions SMART Dust sensors and product lines for automotive HVAC and indoor air quality integration.

-

Sensirion AG (Switzerland) — Known for compact, high-quality PM sensors suited to HVAC and consumer air quality devices; their SPS30 series is a common choice for integration projects requiring compact form and high reproducibility.

-

Shinyei Corporation (Japan) — Longstanding maker of optical sensor modules (PPD series) for broad air quality monitoring use-cases.

Our full vendor profiles include product roadmaps, typical margin structures, channel strategies, and supplier risk scores, enabling procurement and M&A teams to prioritize engagement lists for 2026.

Regulatory and Supply-Chain Dynamics You Must Model

-

Regulation: The EU’s revised Ambient Air Quality Directive (Directive (EU) 2024/2881) tightens PM2.5 limits and streamlines standards for multiple pollutants, creating near-term monitoring demand in public and private portfolios (European Commission, 2026).

-

Monitoring Priorities: The U.S. EPA’s emphasis on next‑generation low‑cost sensors in 2025–2026 alters procurement levers available to city planners and state agencies (U.S. EPA, 2026).

-

Raw material and manufacturing constraints: Laser-based dust sensors rely on high-precision optical components and laser sources that in turn depend on advanced polymer injection molding and tight process control — a potential bottleneck for rapid scale-up (Chengdu Pulse Optics-tech Co., Ltd., 2026).

-

Labor and operational cost drivers: Installing, calibrating, and maintaining dense urban sensor networks creates non-trivial labour cost lines that must be modelled into TCO; optimization of calibration intervals and remote firmware/update strategies materially alters lifecycle economics.

Actionable Recommendations for 2026 Decision-Makers

-

For CEOs / Corporate Strategy: Treat the 2026 budget cycle as the pivot from experimentation to scale. Prioritize investments that combine hardware procurement with service contracts and analytics monetization to protect margins from component commoditization.

-

For CTOs / Product Leaders: Prioritize sensor fusion and edge calibration strategies that reduce field recalibration frequency. R&D investments in optics manufacturing partnerships will reduce unit cost volatility for laser-based sensing lines.

-

For Procurement / Operations: Use modular procurement contracts that separate hardware, maintenance, and software tiers. Insist on data formats, calibration provenance, and remote diagnostics as contractual deliverables to minimize long-term ops spend.

-

For Investors / Corporate Development: Target companies that pair sensor hardware with proprietary data services or unique channel access to institutional buyers. Consider bolt-on acquisitions that bring calibrated deployment expertise to accelerate scale.

Using This Report to Execute in 2026

PW Consulting’s Dust Sensors Market report is structured as an execution manual, not just an analytical compendium. Clients will find step-by-step procurement templates, prioritized vendor shortlists, and practical calibration/maintenance schedules that can be used directly in RFPs and board-level investment memos. The forecasting engine is transparent: you can toggle regulatory, price, and labor assumptions to produce bespoke demand scenarios for capital-planning and cash-flow modelling in 2026.

Because the market remains relatively fragmented — with substantial share available to differentiated entrants — the highest-value moves in 2026 will be those that lock in long-term service relationships, capture recurring calibration and analytics revenues, and mitigate component supply risk through manufacturing partnerships.

Next Steps

To convert these strategic implications into executable plans, PW Consulting’s full report provides the granular tools and supplier comparisons you will need for 2026 procurement cycles, deployment budgets, and M&A screening. Contact PW Consulting to obtain the comprehensive report and receive a tailored briefing that maps our findings to your organization’s strategic, technical, and financial context.

For detailed analysis of this topic, please visit the official page: Dust Sensors Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.