PW Consulting Predicts Articulated Robot Market to Grow at a 15.58% CAGR, Signaling Rapid Automation Gains

Articulated Robot Market 2026: Strategic Playbook for Executive Decision-Making

Executive Summary

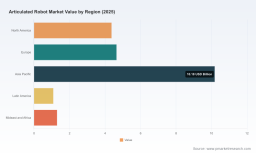

PW Consulting’s latest market research on articulated robots provides an indispensable strategic lens for corporates planning capital allocation, supply-chain redesign, and automation roadmaps in 2026. The articulated robot market has accelerated sharply over the past half-decade — expanding from approximately USD 9.86 Billion in 2020 to USD 21.59 Billion in 2025 — and our forecast shows continued rapid expansion, reaching roughly USD 59.47 Billion by 2032 at a compound annual growth rate (CAGR) of 15.58%. These macro trajectories are clear: the technology is moving from a selective productivity lever to an enterprise-grade capability that shapes product architectures, labor strategies, and competitive positioning.

Articulated Robot Market

Why This Report Matters for 2026 Decisions

In 2026, executives face an inflection point. The choice is no longer whether to automate, but how to automate in a way that preserves agility, controls total cost of ownership (TCO), and creates defensible operational advantage. PW Consulting’s Articulated Robot Market report is designed as a practical decision-support toolkit: it combines rigorous historical time-series (2020–2025), a granular forecasting model for 2026–2032, scenario stress-testing around supply and trade shocks, and executable go-to-market playbooks for vendors, OEMs, and large end-users.

Articulated Robot Market

- Timing and scale: The scale and growth rate in the report let procurement and finance teams model multi-year CapEx phasing with confidence, aligning automation investments to product and labor cycles.

- Risk-adjusted scenarios: We map out downside scenarios driven by geopolitical friction and component shortage, and upside cases that incorporate accelerated adoption of collaborative robots and software-driven services.

- Operational playbooks: The report translates market data into practical steps — supplier due diligence checklists, retrofit vs. greenfield decision frameworks, and staffing/skill transition matrices.

What’s Inside the Report (Practical, Actionable Content)

PW Consulting deliberately balances analytic depth with operational utility. The report contains:

Articulated Robot Market

- Proven forecasting methodology and an interactive model that lets decision-makers test CAPEX scenarios under alternative growth and cost assumptions.

- Market structure and concentration analysis, with implications for pricing power, service availability, and partnership strategies. Notably, the market demonstrates measurable concentration among leading suppliers (CR3 ≈ 51.2%, CR5 ≈ 60.5%), a dynamic that influences negotiation leverage and aftermarket strategies.

- Vendor scorecards assessing product breadth, software and controls maturity, service footprint, and ecosystem openness — designed for RFP shortlisting and supplier risk scoring.

- Regulatory and standards mapping that distills the practical compliance actions companies must take now to avoid retrofit costs later.

- Use-case playbooks for high-impact automation scenarios (e.g., high-mix/low-volume assembly, heavy-payload handling, precision machining, human-robot collaborative tasks), with unit-economics templates that executives can apply directly to project-level business cases.

- An M&A and partnership diagnostic for investors and strategic acquirers considering vertical integration, technology tuck-ins, or service platform consolidation.

Competitive Landscape: Strategic Takeaways

The articulated robot market is shaped by a cohort of established industrial leaders and a new wave of collaborative and software-centric challengers. Our competitive analysis synthesizes product positioning, go-to-market motion, and strategic intent across the largest vendors:

- FANUC Corporation (Yamanashi, Japan): A stalwart in precision six-axis articulated robots, with a strong value proposition in welding, painting, assembly, and high-precision machining. FANUC’s installed base and service network remain key advantages for customers prioritizing uptime and long-cycle manufacturing.

- ABB Ltd. (Zurich, Switzerland): Offers a comprehensive portfolio spanning material handling to heavy-payload solutions. ABB’s recent technical upgrades to its heavy-payload series reinforce its position in large-scale industrial projects and sectors that demand high-throughput automation.

- Yaskawa Electric Corporation (Kitakyushu, Japan): Known for heavy-duty, high-performance articulated robots; a preferred vendor for automotive and similar high-intensity manufacturing environments.

- KUKA AG (Augsburg, Germany): Differentiates through heavy-payload capability combined with AI-enabled software and digital services — a profile that appeals to manufacturers seeking higher levels of autonomy and predictive maintenance.

- Kawasaki Heavy Industries (Tokyo, Japan): Maintains a broad general-purpose lineup and continues to target SMB and mid-market general manufacturing with flexible, cost-competitive solutions — evidenced by targeted new-product introductions.

- Universal Robots A/S (Odense, Denmark): The pioneer in collaborative articulated cobots; their safe human-robot collaboration model lowers integration barriers for small-batch production and shop-floor augmentation.

- Mitsubishi Electric Corporation (Tokyo, Japan): Supplies vertical and horizontal articulated robots optimized for high-volume assembly and precision inspection tasks, with a strong presence in electronics and automotive component manufacturing.

Strategic implication: buyers must evaluate vendors not only on per-unit cost but on ecosystem strength — software openness, service SLAs, retrofit kits, and regional service footprints. For potential acquirers, the intermediate concentration (CR3/CR5 levels) signals opportunity for roll-up strategies in adjacent niches and aftermarket services.

Recent Developments and Standards — What Companies Must Monitor

Recent industry activity underscores two opposing forces: rapid deployment in established automation hubs and growing regulatory and geopolitical headwinds. Highlights include:

- Industry scale: International Federation of Robotics reported 542,000 industrial robots installed globally in 2024, with Asia accounting for the lion’s share of new deployments. This geographic concentration is both an opportunity and a supply-chain dependency to manage.

- Product refreshes: Vendors continue to expand payload ranges and refine specs — a recent round of product launches and catalog updates demonstrates ongoing competitive investment in both traditional heavy-duty platforms and accessible, small-payload cobots.

- Standards evolution: New safety guidance (for example, updated collaborative robot safety parameters introduced in recent standards) and ongoing ISO committee work are changing integration practices and acceptance testing. Early alignment to these evolving standards can materially reduce time-to-production and retrofit costs.

- Geopolitical noise: Trade disruptions and regional supply constraints have already dented demand dynamics in recent periods — our scenarios quantify the enterprise-level exposures and mitigation levers (inventory strategies, multi-sourcing, regional manufacturing hubs).

Actionable Recommendations for 2026

PW Consulting translates market insights into five immediate actions for executives preparing their 2026 plans:

- Prioritize modularity and interoperability: Insist on open-control standards and software APIs in procurement to avoid vendor lock-in and enable cross-vendor orchestration as automation ecosystems evolve.

- Adopt a staged CapEx approach: Structure automation programs in phases aligned to critical product/volume inflection points; use scenario-adjusted NPV models to protect upside while limiting downside exposure.

- Invest in skill transitions: Re-skill frontline engineers to system integrators and automation architects; prioritize O&M competence to extract value from installed bases.

- Stress-test supply-chain resilience: Build and maintain alternative sourcing and regional service agreements to mitigate the impact of trade frictions and lead-time volatility.

- Embed compliance early: Align pilot designs with the latest safety and performance standards to avoid costly revalidation and to shorten time-to-scale.

Why PW Consulting’s Report Is the Next Step

Our report functions as a “decision accelerator.” It gives procurement, operations, and strategy teams the raw market intelligence they need plus applied diagnostics and templates to turn insight into executable plans. Importantly, the report preserves commercial confidentiality for granular segmentation and contract-level metrics — those detailed regional and application splits, supplier-level market shares by revenue and unit shipments, and downloadable forecasting models are intentionally housed in the full deliverable to enable secure, client-grade analysis.

For executives who need to move from strategy to execution in 2026, the comprehensive datasets and scenario tools in PW Consulting’s Articulated Robot Market report will shorten the timeline from decision to deployment and materially reduce implementation risk.

Call to Action

Download the full report to access the interactive forecasting model, vendor scorecards, and downloadable action templates. For organizations that require bespoke advisory, PW Consulting offers tailored workshops and implementation roadmaps that translate insights into procurement strategies, pilot designs, and M&A due diligence briefs.

For detailed analysis of this topic, please visit the official page: Articulated Robot Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.