PW Consulting: Margarine & Shortening Market to Rise from USD 76.5M in 2025 to USD 97.15M by 2032 at a 3.45% CAGR — North America Holds 29.7% Share

Margarine & Shortening Market: Strategic Imperatives for 2026 — PW Consulting Report Preview

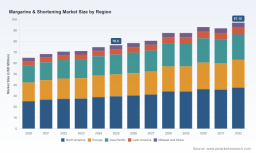

PW Consulting’s new Margarine & Shortening Market report (base year 2025) delivers actionable intelligence designed to guide executive decision-making as companies recalibrate for 2026 and beyond. Anchored in a detailed historical review (2020–2025) and forward-looking projections for 2026–2032, the study models an industry that has expanded steadily from USD 65.0 Million in 2020 to USD 76.5 Million in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 3.45% through the 2026–2032 forecast window. By 2032, our top-line scenario reaches approximately USD 97.15 Million. This preview outlines the report’s strategic value while preserving the proprietary segment-level detail that corporate leaders rely on PW Consulting to protect.

Margarine & Shortening Market

What the Full Report Contains (Practical, Executable Deliverables)

- Robust market-sizing and forward models (historical 2020–2025; forecast 2026–2032) with sensitivity scenarios tied to commodity price swings, foodservice recovery curves, and regulatory interventions.

- Executive-ready playbooks: procurement hedging strategies, capex prioritization for plant upgrades, and product roadmaps for reformulation (clean-label and plant-based trajectories).

- Operational diagnostics for site optimization, energy and waste reduction levers, and a BREEAM/LEED investment impact model linking sustainability upgrades to margin lift and risk reduction.

- Regulatory and compliance toolkit: allergen governance checklists, trans-fat labeling scenarios, and a compliance-readiness scorecard for new product introductions.

- Competitive benchmarking and M&A playbook: profiles and scenario-based valuation ranges for potential targets, integration risk matrices, and synergy capture templates.

- Customer and channel playbooks: foodservice, retail and industrial-baking go-to-market scenarios calibrated to demand elasticity and private-label dynamics.

- Raw-material and input-cost simulation engine that stress-tests profitability across palm oil, other vegetable oils, and energy price pathways.

Data-Driven Narrative: Why Growth is Moderated but Strategic Opportunity Remains

The market’s historical climb—from USD 65.0 Million in 2020 to USD 76.5 Million in 2025—reflects a mix of consumer reorientation (value-driven retail demand and a polarised premium segment), a rebound in foodservice, and steady industrial-baking volume. The moderate 3.45% CAGR we project for 2026–2032 captures both tailwinds (product innovation, plant-based reformulations, expanded industrial use) and headwinds (raw material price volatility, energy costs, and increasingly stringent labeling and allergen requirements).

Margarine & Shortening Market

Supply-side dynamics are central: raw material sourcing (palm and alternative vegetable oils) and energy inputs determine margin volatility. Our modelling demonstrates that a relatively small shift in oil pricing or energy tariffs can compress margins materially—precisely the risk that makes procurement and feedstock diversification top priorities for 2026 budgeting cycles.

Margarine & Shortening Market

Regulatory pressure and ESG expectations are now strategic rather than operational afterthoughts. Recent industry developments underline this point: in May 2025, AAK announced the development of a BREEAM-certified foodservice logistics and operations facility in Dalby, Sweden featuring solar installations—a clear signal that sustainable capital projects are being positioned to control operating costs as well as reputational risk. Puratos’ investment to expand margarine production capacity in Kragujevac (opened Nov 2024) underscores the value of localizing ingredient sourcing to manage feedstock and logistics exposure. Meanwhile, corporate actions around compliance remain visible: Vandemoortele’s acquisition of a major European margarines and spreads division in March 2025 was positioned, in part, to align scale with evolving trans-fat and labeling requirements, and a mid-2025 recall by a large supplier due to undeclared allergens highlights the material operational and brand risk of non-compliance.

Competitive Landscape — Who Moves the Market and How

The industry is moderately concentrated (CR3 ≈ 45%; CR5 ≈ 55%), which creates both stability and competitive opportunity. Incumbent agribusiness and ingredient integrators, specialty fat houses, and large consumer-branded firms each play a distinct strategic role:

- Bunge Limited (White Plains, NY) — A major industrial supplier with scale in shortening fats and margarine. Recent recall activity in 2025 has elevated operational risk considerations, underscoring the need for tightened allergen controls across supply chains.

- Cargill, Incorporated (Minneapolis, MN) — A vertically integrated player that combines oilseed processing and specialty fats; strong in supplying industrial bakeries and confectionery with technical R&D support for formulation optimization.

- Unilever (London, UK) — Leverages consumer brands to drive retail demand for spreads and plant-based alternatives; its consumer-facing scale supports innovation investment and rapid route-to-market for reformulated offerings.

- Wilmar International (Singapore) — Large-scale palm-based production capability, positioning it as a cost-competitive supplier globally; strategic exposure to commodity cycles is a double-edged sword for customers and suppliers alike.

- Puratos Group (Groot-Bijgaarden, Belgium) — Focused on bakery-grade margarine and shortening with recent capacity investments to serve industrial bakers seeking localized sourcing and specialized formulations.

- AAK AB (Malmö, Sweden) — Specialty fats and margarine blends with recent sustainability-oriented facility investments; positions the company well for customers prioritizing ESG and energy resilience.

- Vandemoortele (Gent, Belgium) — Expanded European production footprint via acquisition in 2025; consolidation activity highlights strategic repositioning to regulatory and labeling regimes.

- Dairy Farmers of America (Rosemont, IL) — Supplier of dairy-derived margarines and blends, offering differentiated nutritional and sensory profiles for select foodservice and industrial customers.

- Upfield Holdings BV (Wageningen, Netherlands) — Specialist in plant-based spreads, well-placed to capture the premium and health-conscious retail segments.

- Archer Daniels Midland Company (ADM) (Chicago, IL) — Integrated oils and shortening producer with broad global reach and scale advantages in vegetable oil processing.

These firms’ differing strategic priorities—scale, integration, product specialization, or brand-led innovation—define a landscape where partnerships, targeted M&A, or capability investments can rapidly shift relative positioning.

Strategic Implications for 2026 Corporate Decisions

- C-Suite (Strategy & Capital Allocation): Prioritise investments that reduce margin volatility—sustainability retrofits with short payback periods, nearshoring of key capacities, and selective M&A to shore up channel access. Use the report’s scenario outputs to stress-test capex choices under commodity and regulatory shocks.

- Procurement & Supply Chain: Implement multi-sourcing strategies, index-linked contracts, and optionality for bio-based or alternative oils. Our price-sensitivity matrix pinpoints cost thresholds at which formulation or pricing interventions are required.

- R&D & Product Management: Accelerate reformulation roadmaps for clean-label and plant-based spreads; validate sensory parity with controlled pilot runs. The report’s formulation trade-off tables help quantify yield and cost impacts of fat-substitution choices.

- Operations & Manufacturing: Deploy energy and waste reduction projects prioritized by our site-level ROI model. Consider BREEAM/LEED-aligned upgrades where long-term cost and procurement resilience justify initial outlay.

- M&A & Corporate Development: Target bolt-on acquisitions that deliver capacity in regulatory-compliant jurisdictions or add speciality formulations. Given the market concentration dynamics, opportunistic consolidation is a credible route to scale-driven margin improvement.

Why PW Consulting’s Report Matters for 2026

Our methodology blends a granular top-down market model (historical 2020–2025; base year 2025) with bottom-up plant, channel and SKU-level analyses to produce robust, board-ready scenarios for 2026–2032. The study includes an integrated commodity-cost engine, regulatory-impact simulations, and multiple policy and demand scenarios—tools that transform data into operational decisions. To preserve the strategic utility of our intelligence and to protect the proprietary value for subscribing clients, the report intentionally withholds certain segment-level tables and regional/application splits in this public summary; these are available in full to authorised purchasers.

For procurement directors, R&D heads, and corporate strategists preparing 2026 budgets and three-year roadmaps, this report translates macro trends and discrete industry events—facility developments, targeted acquisitions, and compliance incidents—into concrete action steps, prioritized by financial impact and implementation complexity.

Next Steps

Executives seeking the full set of segment tables, regional and application breakdowns, supplier scorecards, and the proprietary input-cost simulator should contact PW Consulting to access the complete Margarine & Shortening Market report. The complete package includes plug-and-play templates (procurement hedging, capex prioritization, and M&A integration) tailored for immediate deployment during 2026 planning cycles.

For detailed analysis of this topic, please visit the official page: Margarine & Shortening Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.