PW Consulting Forecast: Digital Radiography Leads X‑ray NDT Market as Global Revenue Climbs from USD 9.34 Million in 2025 to USD 14.8 Million by 2032 at a 6.8% CAGR

X-ray Non-destructive Testing Equipment Market — Strategic Outlook for 2026

Executive preview

PW Consulting’s latest market research on X-ray non-destructive testing (NDT) equipment delivers a practitioner-focused strategic compass for 2026. Our analysis shows the global market expanding from USD 5.44 Million in 2020 to USD 9.34 Million in 2025, and we project continued growth to USD 14.8 Million by 2032 driven by a 6.8% compound annual growth rate (CAGR) across the 2026–2032 forecast window. For decision-makers evaluating capital allocation, product roadmaps, M&A targets, or service expansion this year, the report converts macro momentum into a set of actionable choices—while preserving the granular segment-level data in the full report to ensure client engagement and competitive confidentiality.

X-ray Non-destructive Testing Equipment Market

Why 2026 is an inflection year

-

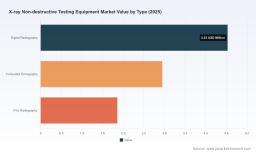

Technology convergence. The industry is moving rapidly from conventional film-based radiography to digital radiography and advanced computed tomography (CT) workflows. This shift is not only about image quality; it changes inspection throughput, data architectures, and lifecycle services (software updates, AI-enhanced reconstruction, cloud storage and analytics).

X-ray Non-destructive Testing Equipment Market -

Regulatory and standards momentum. Recent standard activity—most notably work around computed tomography standards and radiographic testing—has tightened expectations for qualification, traceability, and process validation. ISO 15708-2:2025 and ongoing ISO/TC 135/SC 5 work are forcing equipment purchasers and service providers to reassess compliance plans and certification investments.

X-ray Non-destructive Testing Equipment Market -

Workforce and certification pressures. With ASNT maintaining robust radiographic testing certification pathways (including Level III recertification and scheduled courses in late 2026), firms that fail to invest in certified operators and workflows risk lower utilization and longer ramp times for new installations.

-

Market structure and competitive pressure. The market remains moderately fragmented, creating both margin pressure from low-cost entrants and strategic opportunities for consolidation and differentiated service models.

What the PW Consulting report delivers (practical components)

-

Robust market architecture: historical series (base year 2025; historical window 2020–2025) and forward-looking scenario forecasts for 2026–2032, with clear assumptions on demand drivers, replacement cycles, and adoption curves.

-

Decision-grade financials: TCO and ROI templates tailored by inspection modality, recommended depreciation/CapEx profiles, and sensitivity analyses for key cost inputs (sources, detectors, maintenance).

-

Regulatory and certification matrix: a compact playbook mapping ISO and ASNT activity to procurement requirements, operator training paths, and audit readiness checklists.

-

Vendor benchmarking and go-to-market levers: side-by-side capability assessments (hardware, software, service), aftermarket revenue potential, and channel strategies—presented to facilitate vendor selection without exposing proprietary segment-level sizing in this release.

-

Execution playbooks: short-term (12-month), medium-term (24–36 month), and strategic (3–5 year) roadmaps for OEMs, service companies, and industrial end-users. These include pilot design templates, procurement evaluation criteria, and priority KPIs.

-

Signals-to-watch dashboards: a compact set of leading indicators that buyers, investors, and suppliers can monitor weekly to track demand shifts and competitive moves.

Competitive landscape — what the available intelligence implies

The competitive field spans global platform leaders, specialized portable-system innovators, metrology-focused CT vendors, and a set of high-volume manufacturers primarily serving regional channels. Several firm archetypes dominate strategic thinking for 2026 decisions:

-

Global platform leaders (product breadth, enterprise accounts): Firms such as Comet Yxlon operate at scale, offering integrated X-ray and CT systems for semiconductor, electronics, automotive and aerospace sectors. Their scale supports R&D investments in high-end detectors, reconstruction software, and service networks—making them natural partners for large OEMs and defence contractors seeking end-to-end solutions.

-

Portable and field specialists (mobility and speed): Companies like Vidisco specialize in portable digital X-ray systems tailored for pipeline, weld, and in-situ inspections. For infrastructure operators and field service providers, portability paired with ruggedized workflows is a differentiator that shifts procurement criteria away from pure image metrics to considerations such as battery, data transfer and certification path integration.

-

CT and metrology specialists: Werth Messtechnik exemplifies vendors combining CT capabilities with coordinate metrology for precision industries. Their value proposition centers on measurement traceability and software ecosystems—important where inspection output feeds quality assurance loops or digital twins.

-

Customized system integrators: VisiConsult and certain regional suppliers focus on bespoke configurations, enabling OEMs and electronics manufacturers to adopt inspection systems closely aligned with assembly lines and manufacturing tolerances.

-

High-volume equipment and cost-competitive producers: Several China-based manufacturers supply high-resolution micro-CT, industrial CT, and X-ray imaging at price points attractive for large-scale electronics or casting inspection. These firms pressure pricing in commodity segments while expanding capabilities in higher-margin features (automation and software).

-

Component and source specialists: Companies such as Hamamatsu Photonics and QSA Global play an outsized role in the supply chain as critical component and source suppliers whose pricing and lead-times materially influence OEM margins and project timelines.

Market concentration data indicate that the top-three vendors control a meaningful but not dominant share of global revenue, and the top-five extend that footprint. The implication for 2026 strategic choices is clear: there is room for both consolidation and targeted differentiation. Buyers can exploit this structure to negotiate bundled service agreements, multi-vendor pilots, or managed service contracts that capture productivity upside without overexposing to single-vendor risk.

Recent events and operational signals

-

Trade shows and exhibitions remain key demand accelerants; for instance, vendors like Teledyne ICM are showcasing portable X-ray technologies at major industry forums in 2026, an indicator of continued marketing investment in field solutions.

-

Standards and certification calendars (ASNT training windows, ISO committee activity) act as demand catalysts—organizations planning upgrades risk delays if they miss certification-aligned procurement windows.

How to use this analysis for 2026 decision-making — a short playbook

-

For OEMs and Equipment Suppliers: Prioritize modular, software-friendly architectures. Allocate R&D to detector efficiency and reconstruction algorithms that reduce operator effort and enable subscription-based services. Use the report’s TCO templates to stress-test pricing and service bundles.

-

For Service Providers and Managed-Inspection Operators: Build capabilities around portability and fast-turnaround analytics. Invest in operator certification pathways now to capture service contracts that require certified RT personnel. Consider partnerships with component specialists to secure supply.

-

For Industrial End-Users (Aerospace, Power, Oil & Gas, Automotive): Sequence investments—start with pilot installations tied to measurable yield or safety KPIs, then scale. Negotiate outcome-based service agreements to align vendor incentives with uptime and defect-detection performance.

-

For Investors and M&A Teams: Target high-margin software/service owners or regional integrators with strong channel reach. The market’s fragmentation creates roll-up opportunities, and the report’s vendor scorecard highlights attractive targets by capability set and geographic reach.

Signals to monitor closely in H1–H2 2026

-

Order backlog and lead times for microfocus tubes and detectors—early warning of near-term supply constraints.

-

Participation and product announcements at ECNDT and ASNT events—new product launches or service models will signal where R&D budgets are being deployed.

-

Uptake of ISO 15708-2:2025-aligned processes and ASNT certification enrollments—indicate longer-term demand for higher-spec systems and trained operators.

-

Pricing trends from high-volume Asian manufacturers—watch for margin compression in commoditized product lines and competitive responses from established incumbents.

Closing thought and next step

For executives making 2026 capital and M&A decisions, the X-ray NDT market presents a clear growth runway—quantified in our report by the historical series to 2025 and a forecast to 2032. Yet the opportunity is not uniform: success will flow to organizations that combine technical differentiation, disciplined procurement playbooks, certification readiness, and a clear service strategy. PW Consulting’s full report contains the granular segment-level modeling, vendor scorecards, and downloadable TCO models that equip teams to convert strategic intent into executable programs. Access to that intelligence is the recommended next step for teams preparing budgets, pilots, or acquisition plans this year.

To request the full report or arrange a briefing with PW Consulting’s lead analysts, please visit our report page (link available in the official release). The full dataset and plug-and-play tools are structured to fast-track your 2026 decision cycle without exposing competitive detail in this public summary.

For detailed analysis of this topic, please visit the official page: X-ray Non-destructive Testing Equipment Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.