PW Consulting: Through Glass Vias Substrate Market to Surge from USD 130M in 2025 to USD 276.6M by 2032 at 11.5% CAGR — Asia Pacific Leads

Through Glass Vias (TGV) Substrate Market: Strategic Imperatives for 2026

Executive summary

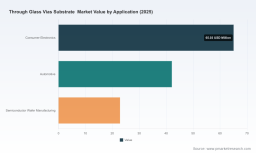

PW Consulting’s Through Glass Vias (TGV) Substrate Market report (base year 2025) frames a pivotal inflection point for semiconductor and advanced-packaging stakeholders preparing decisions in 2026. The global TGV substrate market has expanded rapidly over the past half-decade and—according to our modelling—moves from a 2025 baseline of USD 130.0 Million into a robust growth trajectory across the 2026–2032 forecast horizon at a compound annual growth rate (CAGR) of 11.5%, reaching roughly USD 276.6 Million by 2032. That growth is concentrated around three interlocking themes: scaling high-volume manufacturing, raising inspection and yield engineering capabilities, and integrating glass-based interconnects into heterogeneous packaging roadmaps.

Through Glass Vias Substrate Market

Why this matters for 2026 decision cycles

-

Timing: 2026 is the first full planning year after many pilot and sampling initiatives completed in 2024–2025. Companies that align CapEx, process validation, and supply-chain frameworks this year will capture disproportionate share as throughput-based economics kick in.

Through Glass Vias Substrate Market -

Operational levers: Cost and reliability improvements in laser structuring, metallization, and inspection are the largest controllable drivers of margin improvement. Firms that prioritize process automation and inline metrology can reduce net cost per substrate faster than firms focused solely on material substitution.

Through Glass Vias Substrate Market -

Regulatory overlay: New packaging and waste regulations—most notably the Packaging and Packaging Waste Regulation 2025/40—enter operational effect in 2026–2027 in several jurisdictions. Packaging design choices and supplier selection must account for compliance, recyclability, and documentation early in program timelines to avoid delayed qualifications.

Market trajectory and strategic takeaways

Our historical analysis (2020–2025) shows a clear step-change as TGV moved from laboratory and low-volume applications into targeted high-volume production for consumer, telecom, and compute-related use cases. The forecast period (2026–2032) assumes continued adoption across advanced packaging formats and increased penetration in RF and high-frequency modules. By mid-decade, the implicated growth drivers are: higher-density interconnect needs for chiplet architectures, RF/5G module requirements, and the search for hermetic and thermomechanically compatible substrates for specialized MEMS and sensor packages.

Strategically, this implies three discrete actions for 2026 planning:

-

Prioritize manufacturing readiness over marginal material gains. Capacity build-out, yield ramp plans, and inspection technology integration deliver faster and more predictable ROI than chasing marginal raw-material cost reductions.

-

Integrate reliability engineering into product design gates. Mechanical reliability and via-via proximity effects are non-linear risk factors; early design-of-experiments and accelerated qualification can prevent costly re-designs during production ramps.

-

Use supplier co-development to de-risk inspection and metrology. Partnerships with specialist inspection vendors and laser-equipment suppliers shorten time-to-yield and provide intellectual-property levers for product differentiation.

What the PW Consulting report contains (practical, executable intelligence)

This market study is structured to move executives from awareness to action. Key deliverables include:

-

Market sizing and trend model: A transparent top-down and bottom-up model covering 2020–2025 historical performance and a 2026–2032 forecast, with scenario sensitivity for adoption curves and price erosion.

-

Manufacturing playbook: Stepwise guidance on capacity planning, required capital equipment for laser structuring and metallization, inline inspection checkpoints, and expected yield curves tied to specific throughput milestones.

-

Cost and margin benchmarking: Unit-cost build-ups that translate equipment, cycle time, and yield assumptions into realistic cost-per-substrate ranges; includes sensitivity analyses for volume breaks and equipment amortization.

-

Technology and reliability dossier: Comparative assessment of laser-based structuring techniques, metallization approaches, and reliability stress-test outcomes—plus suggested qualification test plans for early adopters.

-

Commercial playbooks: Go-to-market options for substrate makers, OSATs, and OEMs—covering licensing, co-development, contract-manufacturing structuring, and IP protection strategies.

-

Supplier evaluation toolkit: A practical vendor-assessment framework and heatmap to prioritize whom to engage for equipment, glass substrates, and inspection services (without revealing proprietary scoring details).

Competitive landscape — who to watch and why

The TGV substrate market today is characterized by moderate fragmentation. The top three vendors capture about one quarter of the market share while the top five approach roughly forty percent, leaving meaningful opportunities for specialized suppliers and niche integrators.

-

Corning Incorporated — As a leader in glass-core substrate manufacturing, Corning’s capability to scale high-volume glass production and leverage existing packaging relationships positions it as a primary source of supply for global OEMs pursuing glass interconnect strategies.

-

LPKF Laser & Electronics SE — LPKF’s laser-based structuring and their LIDE technologies are central to many high-throughput TGV programs. Recent equipment integrations focused on inspection and process control accelerate customers’ ability to reach production-grade yields.

-

SCHOTT AG — SCHOTT’s emphasis on hermetic sealing and MEMS-compatible glass (HermeS) differentiates it in niche applications where environmental robustness is non-negotiable. Their recent conference disclosures on via-via spacing and mechanical reliability underscore the company’s technical leadership in reliability science.

-

Plan Optik AG — A specialist in metallized TGVs and volume laser structuring, Plan Optik blends equipment know-how with process integration for MEMS and advanced packages.

-

Tecnisco, NSG Group, Kiso Wave, Allvia, Samtec, E&R Engineering — These regional and technical specialists collectively extend the market’s capacity footprint and provide differentiated offerings—ranging from RF-optimized substrates to AI-focused glass-silicon hybrid solutions. Their presence reduces supplier concentration risk but raises the bar for procurement rigor.

Recent industry moves that shift the 2026 playing field

-

April 2026 — SCHOTT AG presented new empirical findings on how via-to-via distance and density impact mechanical reliability at ICEP-HBS 2026. Implication: product architects must bake in tighter reliability margins when pursuing higher via densities.

-

November 2025 — Onto Innovation published a technical analysis of TGV manufacturing process constraints and inspection challenges. Implication: inspection workflows and defect-classification frameworks are now recognized as gating factors for volume ramps.

-

April 2025 — LPKF integrated Onto Innovation’s Firefly inspection system into its Hannover facility, creating a near-line inspection capability to support panel-level packaging volumes. Implication: combined equipment + inspection offerings materially shorten qualification timelines for COGs and OSATs.

-

May 2025 — Nippon Electric Glass released larger-form-factor TGV samples fabricated via laser modification and CO2 processing. Implication: substrate form-factor flexibility is increasing and creates new packaging architecture options for high-channel-count modules.

Key risks and mitigations for 2026

-

Yield and inspection shortfalls — Risk: inconsistent defect detection leads to yield erosion during ramp. Mitigation: invest in co-validated inspection strategies (optical + X-ray + acoustic) and require supplier proof-of-yield during sourcing.

-

Regulatory and end-of-life constraints — Risk: new packaging regulations introduce compliance cost and documentation burdens. Mitigation: adopt early-design-for-compliance checklists and prefer suppliers with transparent material disclosure processes.

-

Supply-chain concentration — Risk: a small number of glass substrate producers and laser-equipment vendors could create bottlenecks. Mitigation: dual-sourcing strategies, strategic inventory, and co-investment models can smooth supply shocks.

Action roadmap for executives (practical 90–180 day plan)

-

90-day: Commission a readiness assessment that maps current product designs against TGV-specific reliability tests and inspection requirements; shortlist 2–3 partners for pilot co-development.

-

180-day: Execute pilot qualification with a targeted OSAT or substrate supplier that includes agreed yield gates, inspection protocols, and a cost-sharing template for tooling or equipment upgrades.

-

Ongoing: Integrate regulatory compliance checkpoints into product milestones and establish a cross-functional gating process that aligns packaging, procurement, and reliability engineering teams.

Closing — why the full report matters

For teams preparing capital, sourcing, and product roadmaps in 2026, the strategic advantage will accrue to organizations that treat TGV deployment as an integrated manufacturing and reliability challenge—rather than simply a materials substitution project. PW Consulting’s full report supplies the operational blueprints, cost models, and supplier-risk frameworks necessary to migrate from pilot to profitable volume. We deliberately surface the modelling assumptions, scenario levers, and supplier profiles that executives need to make evidence-based decisions, while safeguarding granular segmentation data in order to preserve the integrity of the market intelligence.

To access the complete dataset, interactive models, and supplier heatmaps that underpin these conclusions, please visit the report landing page for licensing and executive briefings.

For detailed analysis of this topic, please visit the official page: Through Glass Vias Substrate Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.