PW Consulting: Kitchen Food Garbage Processors Market to Rise from USD 3,110.0 Million in 2025 to USD 4,439.47 Million by 2032 at a 5.21% CAGR

PW Consulting Strategic Brief — Kitchen Food Garbage Processors Market: A 2026 Playbook for Decision-Makers

As businesses, OEMs, investors, and public-sector stakeholders set strategies for 2026, the kitchen food garbage processors sector demands a finely tuned response to evolving demand patterns, supply-chain stressors, regulatory shifts and concentrated competition. Our new market research synthesizes five years of historical performance and a seven-year forecast horizon to deliver the tactical intelligence required to prioritize investment, innovate product lines and redesign supply chains.

Kitchen Food Garbage Processors Market

Headline view: market scale, trajectory and structure

-

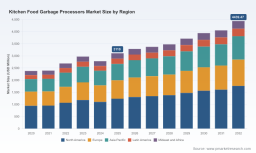

Market scale: The global kitchen food garbage processors market reached approximately USD 3.11 billion in our 2025 base year after rising from roughly USD 2.38 billion in 2020 — a trajectory that underscores both growing adoption and episodic market adjustments.

Kitchen Food Garbage Processors Market -

Growth outlook: PW Consulting projects a compound annual growth rate (CAGR) of 5.21% over the 2026–2032 forecast period, which takes the market to an estimated USD 4.44 billion by 2032 under our central scenario.

Kitchen Food Garbage Processors Market -

Competitive structure: The industry demonstrates moderate concentration — the top three firms account for nearly half of market sales while the leading five capture over 60% — a structure that shapes pricing power, distribution dynamics and M&A calculus.

Why this report matters for 2026 decisions

-

Operationalizing risk and opportunity: 2026 will be a year of trade-offs. Our report translates macro scenarios (tariff regimes, commodity volatility, localized regulatory mandates) into operational decision triggers — when to hedge, when to localize production, when to accelerate product upgrades to capture premium segments.

-

Capital allocation clarity: For product OEMs and component suppliers, the report provides prioritized investment options across R&D, assembly footprint and aftermarket service programs, tied to quantified outcome ranges rather than qualitative conjecture.

-

Commercial playbooks: Retailers, distributors and installers gain go-to-market templates for rolling out retrofit programs, subscription-based maintenance and bundling strategies that improve lifetime customer value and reduce churn.

-

M&A and partnership scoring: We present a framework to evaluate inorganic targets and strategic alliances that strengthen channel access, intellectual property or component sovereignty — particularly relevant in an environment of tariff-driven input cost pressure.

What the report contains (practical, executable modules)

-

Demand modeling and scenario toolkits — reproducible spreadsheets that let users project revenues by alternative recovery, adoption and regulatory scenarios for 2026 planning cycles.

-

Cost and margin decompositions — factory-gate and landed-cost analyses that isolate the impact of raw-material inflation (notably steel and aluminium) and import tariffs on unit economics.

-

Supply-chain stress tests — vulnerability maps for key components, alternative sourcing strategies, and recommendations for nearshoring versus diversified multi-sourcing.

-

Commercial playbooks — segmented go-to-market approaches by channel archetype (mass retail, specialty dealers, installer networks), including pricing architecture and service propositions.

-

Competitive benchmarking — qualitative and quantitative profiles of the leading players across technology, distribution, production footprint and brand positioning, plus an ecosystem map of emerging challengers.

-

Regulatory and policy scenario mapping — analyses of jurisdictional bans, extended producer responsibility trends and trade-policy stressors, with recommended compliance and advocacy responses.

-

Investment case templates — tailored for corporate strategy teams and private capital, including downside sensitivity analyses and modeled exit multiples under different consolidation outcomes.

Market dynamics shaping 2026 strategy

-

Trade policy and input-price shock: The 2025 tariff environment — including a baseline tariff on imports and asymmetric duties on certain supply chains — has translated directly into higher landed costs for disposers manufactured with steel and aluminium components. Our cost models show these inputs are a primary driver of near-term margin compression and a key determinant of sourcing and pricing decisions in 2026.

-

Regulatory tailwinds in commercial segments: Local food-waste diversion mandates are reshaping the commercial market, driving demand for higher-capacity units and service contracts in hospitality, healthcare and institutional settings. These regulations create durable demand pockets, particularly for solutions paired with on-site processing or off-take contracts.

-

Product innovation cycle accelerates: Companies that demonstrate clear differentiation — quieter operation, reduced clogging, integrated water- and energy-saving modes, and modular designs for easy servicing — are best positioned to capture share while commanding premium pricing.

-

Consolidation and channel power: A market concentration where the top-three and top-five firms hold material shares means incumbents will continue to set distribution standards and brand expectations, but mid-tier and challenger players can win by owning niche channels, technology IP or superior installation/service ecosystems.

Competitive landscape: what to watch from key players

-

InSinkErator (Whirlpool ownership): The historical category leader stands on strong manufacturing heritage and technology claims such as advanced grinding and acoustic management. Their scale confers distribution advantage and R&D capacity; watch for continued product line sophistication and enterprise-level channel partnerships.

-

Waste King (Anaheim Manufacturing Company): Recognized for high-performance residential units, Waste King’s playbook emphasizes robust motors, installer-friendly mounting systems and value-oriented positioning — effective strategies in markets where DIY and replacement demand dominate.

-

Moen Incorporated: Integration with kitchen fixtures and proprietary motor technologies give Moen a platform to sell bundled value propositions — a move that increases wallet share per kitchen and reshapes installation economics.

-

Franke & other premium European brands: Firms such as Franke compete on quiet operation, build quality and premium channel presence. Their customers prize long-term reliability and aesthetics, creating an opportunity for higher margins but limited scale expansion without deliberate distribution investment.

-

GE Appliances, Whirlpool and regional OEMs: These firms maintain broad distribution and brand recognition. Their strategic choices — whether to prioritize OEM partnerships, retail exclusives, or bundled appliance promotions — will influence market segmentation and the aftermarket service landscape in 2026.

-

Emerging players and product launches: New entrants are surfacing with differentiated designs for modern kitchens and claims of handling higher ranges of food waste without clogging. These launches accelerate category innovation and place a premium on demonstrated field reliability.

Regulatory and cost headwinds — immediate implications

-

Tariff-driven sourcing shifts: Elevated duties on certain imports make component localization and alternate-material design immediate priorities for 2026 CAPEX planning. Companies should evaluate a hybrid approach: selective localization for high-volume parts and hedging for specialized components.

-

Commercial diversion mandates: Jurisdictional bans and diversion requirements create predictable demand in specific institutional segments; manufacturers and service providers that build compliance-aligned offerings can lock in long-term contracts and premium service revenue.

-

Raw-material inflation: Steel and aluminium cost cycles materially impact unit economics. The recommended mitigation levers include design for material efficiency, supplier commitments, and price-indexed contracts with key distributors.

Actionable recommendations for 2026 planning

-

For OEMs: Prioritize modular designs that reduce dependence on tariff-exposed components and allow for regional bill-of-materials optimization. Accelerate development of quieter, clog-resistant platforms that command higher ASPs in retrofit markets.

-

For suppliers: Lock targeted multi-year contracts for high-risk inputs, and offer co-development agreements that embed suppliers into OEM product roadmaps to secure volume and margin stability.

-

For retailers and installers: Build retrofit and subscription-service bundles that lower upfront price friction and create recurring revenue streams tied to maintenance and consumables.

-

For investors and M&A strategists: Use our scoring matrix to prioritize targets that offer channel access, IP in grinding and noise-control technologies, or service-network density. Smaller firms with superior installation economics can be attractive bolt-ons to incumbent portfolios.

-

For policy teams and procurement officers: Leverage diversion mandates to structure procurement that favors total-cost-of-ownership outcomes — installing disposers paired with maintenance contracts and diversion audits reduces landfill costs and regulatory risk.

What we intentionally hold back — and why

Consistent with the “trailer” approach, this brief emphasizes strategic context and executable guidance while withholding the granular regional and application splits, unit-price matrices and full company revenue breakdowns that live in the licensed report dataset. Those detailed tables, proprietary models and downloadable spreadsheets are included in the full PW Consulting publication and are essential for transaction-level diligence and board-level decisioning.

How to use the full report in your 2026 cycle

-

Integrate the scenario spreadsheets directly into your 2026 operating-plan discussions to stress-test revenue and margin targets across tariff, material-cost and regulatory scenarios.

-

Use our supplier vulnerability map and recommended mitigation playbook to sequence sourcing changes across Q1–Q3 2026, aligning CAPEX approvals with expected payback periods under conservative assumptions.

-

Apply our M&A scoring framework to screen and shortlist targets for mid-market consolidation plays, then layer in sensitivity testing from the report to validate acquisition pricing and integration risk premiums.

PW Consulting’s Kitchen Food Garbage Processors Market report is purpose-built to convert market intelligence into prioritized actions for 2026. For access to the full dataset, segmented analyses, downloadable models and the complete competitive database — including the granular regional and application breakdowns required for transaction-level decisions — please visit the PW Consulting reports portal or contact our industry team to arrange a briefing.

For detailed analysis of this topic, please visit the official page: Kitchen Food Garbage Processors Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.