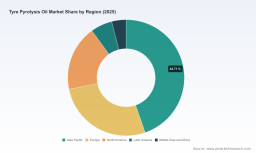

PW Consulting: Tyre Pyrolysis Oil Market to Reach USD 629.45 Million by 2032, Growing at 5.29% CAGR (2026–2032) — Asia Pacific Leads with USD 196.04M in 2025

Tyre Pyrolysis Oil Market 2026: Strategic Imperatives for Investors, Offtakers and Industrial Players

Executive summary

As industrial decarbonization and circularity mandates tighten, tyre pyrolysis oil (TPO) has moved from niche curiosity to commercial-scale feedstock and fuel candidate. Our PW Consulting Tyre Pyrolysis Oil Market report — anchored on a 2025 base year and projecting across 2026–2032 — identifies a structurally growing market driven by technology maturation, regulatory recognition, and the rise of integrated industrial offtakes. The market is forecast to expand at a compound annual growth rate (CAGR) of 5.29% through the forecast window, with the near-term (2026) landscape shaped by key plant ramp-ups, fresh policy signals and the first wave of ISCC/REACH-recognized supply chains.

Tyre Pyrolysis Oil Market

Market snapshot and trajectory

Between 2020 and 2025 the market experienced steady expansion, reflecting improved plant economics and growing acceptance of TPO as a sustainable feedstock. The PW Consulting market model (base year 2025) projects continued growth into the forecast horizon, reflecting a combination of incremental capacity additions, rising industrial integration and policy tailwinds that carve clearer pathways to commercial adoption.

Tyre Pyrolysis Oil Market

Important to strategic planning are two quantitative anchors from our modelling: the mid-decade base and the conservative baseline CAGR of 5.29% used across scenario and sensitivity runs. These anchors enable rigorous comparison of in-house project returns, offtake timing and capex phasing against market-driven demand growth assumptions.

Tyre Pyrolysis Oil Market

Why 2026 is an inflection year for corporate decision‑making

- Policy and standards are coalescing: Under RED III (effective mid‑2025) the biogenic fraction of TPO is recognised as an advanced biofuel pathway (Annex IX Part A alignment) while the fossil fraction can qualify as Recycled Carbon Fuel (RCF) if lifecycle GHG savings meet high thresholds — a dual regulatory recognition that changes commercial valuation for blended streams.

- Regulatory clarity is accelerating market integration: National classifications — notably the decision by France to treat TPO as a raw chemical resource — reduce integration risk for chemical and polymer producers evaluating circular feedstocks.

- Certification and commercial-scale plants are emerging: Recent ISCC and ISCC PLUS certifications, REACH registrations, and large plant inaugurations signal that technology and compliance barriers are being lowered, enabling offtake contracts and long‑term partnerships.

- Feedstock and product metrics are now well-understood: Typical crude yields from end‑of‑life tyres (ELTs) fall in an industrially reproducible band (roughly 40–50% on a steel‑free basis), and routine characterisation of density, calorific value and sulphur content informs engine‑level and refinery integration decisions.

What PW Consulting’s report delivers (practical, execution‑focused)

- Transparent market sizing and a base‑case forecast with upside/downside scenarios calibrated to policy, certification uptake, and capex rollout pace.

- Supply‑chain maps and unit‑economics templates — from ELT collection and pre‑treatment to TPO upgrading, logistics and end‑market blending — that executives can drop into capital planning and cash‑flow models.

- Project feasibility checklists and plant‑level benchmarking (continuous vs batch pyrolysis paradigms, reactor scale profiles, heat‑integration opportunities, and typical operating expenditure buckets).

- Regulatory and certification playbook covering ISCC, REACH, RED II/III and national classification routes, with an impact matrix linking certification status to offtake pricing and market access.

- Commercial models for offtake structures (tolling, fixed‑price supply, indexed supply) and a library of contract clauses and KPIs tailored to TPO quality variability.

- Technology vendor analysis and licensing comparators with key sensitivities for conversion efficiency, maintenance cadence and capital intensity.

- Risk and mitigation matrices (feedstock variability, product spec drift, policy reversal scenarios), plus investor‑grade scenario outputs suitable for board deliberation in 2026.

Competitive landscape — fragmentation and strategic moves

The tyre pyrolysis oil market remains fragmented: concentration metrics point to a low aggregated market share for the largest players, leaving substantial room for new entrants and regional champions. That fragmentation produces both opportunity and risk: first‑mover advantages accrue to companies that secure feedstock access, certification and industrial offtakes, but the market can absorb multiple successful business models across licensing, asset ownership and trading.

- Circtec — With the recent inauguration of a large ELT pyrolysis facility in Delfzijl and announced phase‑2 expansion plans, Circtec is positioning itself as an industrial‑scale supply anchor for petrochemical and refinery markets. Strategic implication: large‑scale players can lower per‑unit costs and negotiate integrated offtake agreements with downstream clusters, but must manage stacking regulatory and merchant risk during early ramp phases.

- Pyrum Innovations AG — Pryum’s thermolysis technology combined with ISCC certification achievements and formal recognition by French authorities creates a clear commercial corridor into EU chemical and fuel value chains. Strategic implication: certification and regulatory engagement accelerate market access and price premia for compliant material.

- Klean Industries — Active global project development and licensing partnerships indicate a playbook focused on technology export and turnkey supply. Strategic implication: licensors can scale quickly through partners, but must ensure quality control and consistent product specifications across geographies.

- New Energy Kft. — Early adopters of continuous process designs and sustainability certification demonstrate a vertically integrated model from feedstock to certified product. Strategic implication: origin‑based certification and point‑of‑origin claims will be a differentiator in premium markets.

- Enespa AG — As a trader and certification/technical services provider, Enespa exemplifies the commercial intermediary role that will connect smaller producers to industrial offtakers. Strategic implication: trading and compliance services reduce market entry friction for smaller plants and create liquidity for standardised TPO streams.

Practical strategic playbook for 2026 executives

For corporate boards and strategy teams setting 2026 priorities, the following actions should be sequentially evaluated and, where appropriate, executed quickly.

- Lock feedstock channels: Secure long‑term ELT supply or partnering arrangements with tyre collectors. Volume commitments are the single most influential lever on project IRR.

- Prioritise certification early: ISCC/ISCC PLUS and REACH pathways materially expand addressable markets. Certification timelines should be integrated into project schedules and capex drawdowns.

- Design for product standardisation: Invest in upstream quality controls and blending protocols to deliver consistent TPO specifications that downstream refineries and chemical customers can adopt without re‑tooling.

- Choose the right process archetype: Continuous systems support scale and throughput predictability; batch systems may suit modular or distributed applications. Use our plant‑level benchmarking to stress‑test technology choices against your balance‑sheet constraints.

- Structure offtake and risk allocation smartly: Use hybrid commercial contracts (partial fixed volumes, partial indexed volumes) and include QA/QC, contingency and certification transfer clauses to manage price and reputation risk.

- Blend policy advocacy with prudence: Engage with regulators on methodology for GHG accounting and feedstock traceability, while maintaining conservative financial models that do not rely on discretionary incentives.

- Explore adjacency value capture: Beyond TPO, recovered carbon black and steel residues have monetisation paths. Integrated product portfolios materially improve overall project economics.

- Plan for staged scale-up: Use an initial proof‑of‑concept or tolling arrangement to shorten learning curves and validate offtake before committing to full‑scale capex.

How PW Consulting’s report supports 2026 decisions

Our dataset and analytics are built to be actionable for 2026 capital planning cycles. The report pairs a robust market forecast (with sensitivity to certification uptake and major plant rollouts), granular unit‑economics templates and a certification/regulatory toolkit that directly maps to commercial terms. Importantly, while this press summary highlights the strategic levers and market drivers, the full report contains the region/application breakdowns, plant‑level case studies, and downloadable financial models that decision makers will need to model specific investments and contractual terms.

Final takeaways

Tyre pyrolysis oil is transitioning from proof‑of‑concept to an investable industrial‑scale commodity for companies that align technology choices, certification pathways and offtake strategies today. 2026 will reward organizations that have already advanced feedstock contracts, obtained or scoped certification routes, and chosen a commercial model that balances scale with quality control. The market remains sufficiently fragmented to allow multiple successful entrants, but early movers with certified, consistent supply chains will secure preferential access to chemical, fuel and circular material offtakes.

For strategy teams preparing board materials, investment committees or M&A scoping documents in 2026, the PW Consulting Tyre Pyrolysis Oil Market report provides the data, scenario tools and regulatory playbook to move from analysis to executable investment decisions. Access the full dossier for the proprietary regional and application splits, plant case studies and downloadable models that underpin our conclusions.

For detailed analysis of this topic, please visit the official page: Tyre Pyrolysis Oil Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.